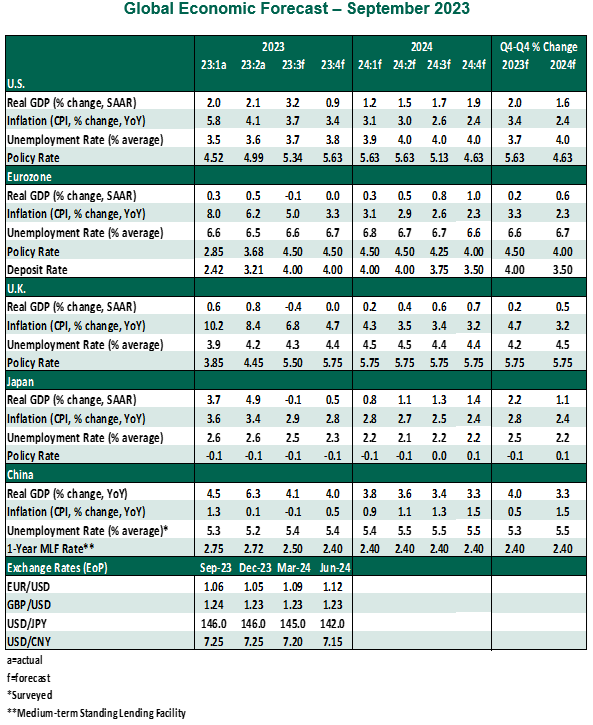

Global Economic Outlook: China Casts A Shadow In The East…And West

The Northern Trust Economics team shares its outlook for major markets in the months ahead.

The post-pandemic economic environment has left most observers humbled. Whether it was the speed of rebound in the reopening phase, the surge in inflation that followed or the economic resiliency of the West in the face of tighter policy, the past couple of years have continually confounded forecasters. That said, a slowdown is upon us. Activity in China and Europe has weakened notably in recent months, and there are signs that the U.S. economy is poised for a deceleration.

The softer outlook is bringing the rate hiking cycle close to an end for Western countries, but the peak is still not entirely clear. Inflation is falling, but not quickly enough to allow a pivot. The recent rise in oil prices and still-tight labor markets may slow the speed of disinflation. American and European central banks will err on the side of keeping policy tighter for longer, while the People’s Bank of China (PBoC) battles to prevent persistent deflation.

Striking a balance between price and economic stability is what the policymakers strive for, but that will be hard to achieve without a compromise on one or the other.

This month’s edition of the global outlook offers a deep dive into the Chinese economy.

China

- After a sharp rebound in activity at the start of the year following the removal of COVID restrictions, China's economy has struggled in recent months. Real gross domestic product (GDP) grew 0.8% in the June quarter, down from 2.2% in the first three months of 2023. The slowdown reflects the end of China's multi-decade real estate boom, an increasingly challenging backdrop for exports, and a guarded stance by the Chinese policymakers.

- Activity data for August, however, brought signs of tentative stabilization. Support measures from the Chinese government provided a boost to consumption and infrastructure investment. The PBoC reduced reserve requirement ratios to boost liquidity. But one month of data does not make a trend. China’s continued economic recovery is still challenged by insufficient domestic demand and narrowing export channels.

- The outlook for the Chinese economy remains challenging, with risks tilted heavily to the downside. China’s massive property sector, the main source of wealth generation for Chinese households, remains a major headwind. Property sales have plunged and are ~30% below the peak. Housing construction continues to fall and home prices slid further last month. Unemployment is rising, and confidence is falling.

- Evergrande and Country Garden are not the only property developers in trouble; many more are at risk. As of end of August 2023, at least 55 Chinese developers that have issued dollar-denominated bonds have either defaulted or extended the maturities of their offshore debt. Direct easing measures to underpin the ailing property sector, such as mortgage rate cuts, lower minimum down-payment ratios for first-time purchasers, easing of mortgage payment rules and buying restrictions will neither solve developers’ problems nor revive the real estate sector.

- A leading Chinese trust company missed payments on investment products, adding to fears that the slowdown may trigger a financial crisis beyond the property sector. The Chinese banking sector is well capitalized and has been steadily reducing its reliance on the real estate sector since the start of the deleveraging campaign in 2016. The implicit or explicit state backing to the large onshore banks will prevent the situation from spiraling out of control. That said, further correction in housing coupled with lower interest rates will dent banks' profitability and increase non-performing loans, wearing away banks’ capacity to cushion the economy.

- Past property slowdowns were met with substantial fiscal and monetary support. However, after more than a decade of credit-fueled expansion, the piecemeal easing approach adopted in the current downturn suggests that the policymakers are no longer willing to rely on large-scale stimulus to boost growth. This incremental approach will only help put a floor on growth, instead of providing a sizeable boost to activity.

- China’s status as the world’s largest exporter is under threat, and not solely from softer external demand. An acceleration in supply chain realignment in the face of rising geopolitical tensions is a major factor behind that risk, as western firms are increasingly reassessing their China exposure. The latest trends in U.S.-China trade demonstrate this clearly.

- The renminbi (RMB) has come under pressure amid weakened growth prospects, with the currency slumping about 6% this year against the dollar. A weaker currency will provide much-needed impetus to Chinese exports, but will likely be accompanied by other unwanted consequences. Sustained pressure on the RMB will add to debt in domestic currency terms, thereby increasing leverage. It could also lead to renewed accusations of currency manipulation by the United States and its allies.

- The property downturn and structural issues such as declining demographics, slower total factor-productivity growth, and high debt will weigh on China’s growth prospects. We expect GDP growth to slow further to 4.0% year over year by the end of 2023. 2024 is likely to be even weaker; we are penciling in 3.5% growth for next year.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.