Options Quarterly Commentary Q4 2025

US equities ended the fourth quarter of 2025 higher despite a challenging macro backdrop, closing at 6845.50, up +2.35 % vs Q3 2025. Performance was supported by resilient earnings growth, easing inflationary pressures, and 50 basis points worth of interest rate cuts from the Federal Reserve. Even after the sharp sell-off in April following the Trump administration’s tariff announcements, the S&P 500 closed the year up nearly 18%, delivering a third consecutive year of double-digit gains.

Volatility defined much of the quarter with markets facing a series of headwinds, including the longest government shut down on record, weak labor data, policy uncertainty, and renewed concerns around lofty AI valuations. Average VIX levels in Q4 were 15% higher than Q3, ranging from a peak of 26.42 on November 20 to a low of 13.47 on December 24.

Volatility followed a clear progression through the quarter with October’s tariff-related disruption, November’s spike driven by valuation concerns and policy uncertainty, and December’s sharp compression to multi-year lows. SPX skew flattened meaningfully in the final two weeks of 2025, reflecting a combination of reduced hedging activity and increased demand for upside exposure (Nomura). According to CBOE, one-month skew (25- delta) fell from the 90th percentile in mid-December to around the 40th percentile by year-end (CBOE). The CBOE Volatility Index (VIX) closed the quarter at 14.95, down -43% from its November peak and -8.2% lower vs Q3 2025.

The S&P 500 finished 2025 with an 80th percentile 18.6% realized volatility. It was noted by Rocky Fishman from Asym 500 how unusually concentrated volatility was in 2025, with just five trading days accounting for nearly 15% of total absolute returns, the highest since 1987.

SPX and VIX performance Q4 2025 (Source: Bloomberg)

Key Themes in 2025

1. Record Options Trading Volumes

Options trading activity reached record levels in 2025 amid a year of heightened volatility. According to OCC data, total options volumes hit 15.21 billion contracts, up 24.4% vs 2024. By product type, volumes were split approximately 54% equity options, 37% ETF options and 8.3% index options. In 2025, retail traders accounted for approximately 30% of total options volume, underscoring the impact retail investors now have on market outcomes.

December also saw a record options expiration, with an estimated $7.1 trillion in notional options exposure expiring, reinforcing the growing influence of options positioning on short-term market dynamics. Structurally, the US options market remains highly competitive and fragmented, with 18 active exchanges and two more expected to launch in 2026.

2. Continued Rise of Zero-Day-to-Expiry (0DTE) Options

0DTE options have become a dominant feature of options trading, representing ~23% of total US options flow in 2025 (as shown below). Most notably 0DTE SPX options average daily volume reached approximately 2.3 million contracts, representing 60% of total SPX option volume (CBOE), underscoring how dominant same day expiries have become in the index space.

This growth has largely been driven by retail investor participation, accounting for roughly half of all 0DTE trading (Bloomberg), and points to more speculative retail behavior. The surge in 0DTE activity has impacted market volatility and liquidity dynamics, with heavy trading around key macro events often amplifying price swings, as 0DTE trades are hedged by dealers who buy or sell stock to remain delta neutral.

Source: Goldman Sachs

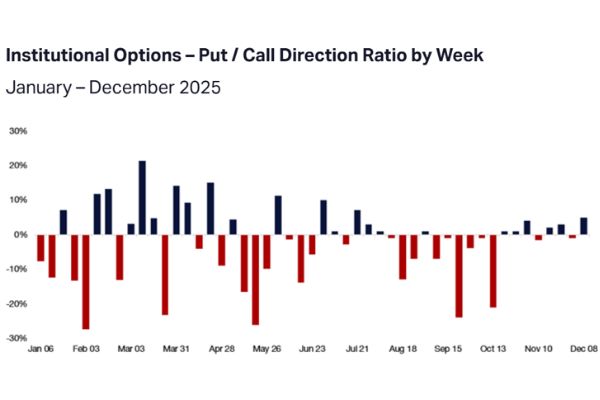

3. Bullish Retail Investors vs Cautious Institutional Investors

Citadel data shows that retail investors maintained a persistently bullish stance throughout 2025. As you can see below, in all but five weeks of the year, retail investors were net buyers of calls, signaling their strong risk appetite despite periods of elevated market volatility. Citadel highlights that retail investors stayed calm during bouts of volatility and historically, retail positioning remains relatively balanced as average VIX levels rise, up until 35. Beyond this threshold sentiment appears to shift, with extreme net sell days occurring at roughly twice the frequency of extreme net buy days.

In contrast, institutional investors adopted a more cautious approach to positioning, reflecting a greater focus on hedging, evidenced by the put-call ratio being far less consistent week to week. This suggests more tactical positioning and risk control during volatile periods rather than persistent bullish conviction.

Source: Citadel Securities

Looking ahead to 2026

Conflicting AI narratives and US political uncertainty are creating a supportive backdrop for continued market volatility in 2026. Strategists expect equity volatility to remain elevated, with many warning that the tech bubble could become increasingly unstable. Against this backdrop, UBS strategists argue that whether the AI boom ultimately continues or reverses, exposure to options that profit from higher volatility on the Nasdaq offer a way to position for both sides of the trade.

Historically, midterm election years represent the most volatile phase of the four-year presidential cycle. According to Aptus Capital Advisors, the S&P 500 experiences an average intra-year decline of 19% during midterm years, compared with 12% in the other years, alongside a 16% average drawdown across the full cycle. This historical pattern reinforces expectations for elevated volatility throughout 2026.

Geopolitical risks have also surfaced early in the year, with developments in Venezuela driving a sharp increase in gold volatility and positioning turning notably more defensive. One-month GLD skew steepened to the 80th percentile in early January, reflecting increased demand for downside protection (CBOE). CBOE highlighted that during this time GLD puts traded at parity with calls, suggesting markets priced downside risk equal to upside potential for gold in the short term (the first time since May 2025).

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.