- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Surplus Assets and Shortfall Risk

The primary goal of most private investors is to have sufficient assets to fund their lifetime consumption. There are many definitions of risk, but running out of money too soon – the risk of failing to fund anticipated lifetime consumption – is perhaps the most tangible one. This is the notion of shortfall risk.

By Peter Mladina, Executive Director of Portfolio Research, Wealth Management

Charles Grant, CFA, Senior Analyst, Wealth Management Portfolio Research

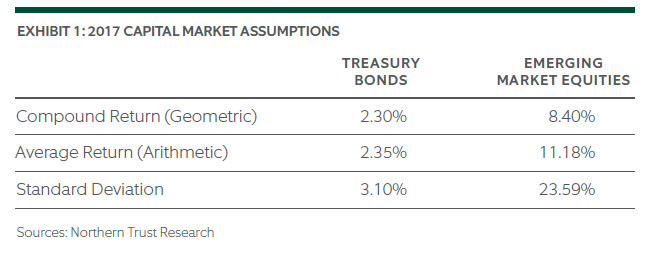

Shortfall risk is commonly defined as the probability of a shortfall. To mitigate shortfall risk, some investors want a buffer of assets in excess of what is needed to fund their anticipated lifetime consumption (and other high-priority goals). This surplus increases their confidence that they will be able to fund their lifetime consumption. But this view of shortfall risk is incomplete because it fails to consider the magnitude of potential shortfall. A higher magnitude of potential shortfall can offset a lower shortfall probability. A better option for many risk-averse investors may be to use some or all of a surplus to settle a larger proportion of their high-priority consumption goal with safe assets. To illustrate the point, consider a high-net-worth investor with the consumption goal of funding $500,000 per year over her remaining 30-year lifetime planning horizon. She has a current investment portfolio of $11 million. Assume consumption can be funded using either a safe asset with a small surplus (scenario 1) or a risky asset with a large surplus (scenario 2). For this illustration, we use intermediateterm Treasury bonds as the safe asset and emerging market equities – at the other end of the return and risk spectrum – as the risky asset. Exhibit 1 shows Northern Trust’s 2017 capital market assumptions for these two asset classes.

The compound return is the expected multi-year (annualized) return. The average return is the expected single-period (one-year) return in the presence of volatility risk (standard deviation). The average return and standard deviation are parameters in Monte Carlo simulation. We employ this set of assumptions in a Monte Carlo simulation with 3,000 trials.1 From the simulation we capture the probability of shortfall and the magnitude of potential shortfall. The magnitude of potential shortfall can be quantified in different ways when relating it to lifetime consumption. We use the average number of years of unfunded consumption and the average unfunded percentage of the consumption goal (shortfall ratio) when there is shortfall.

SCENARIO 1: LOW RISK, SMALL SURPLUS PORTFOLIO

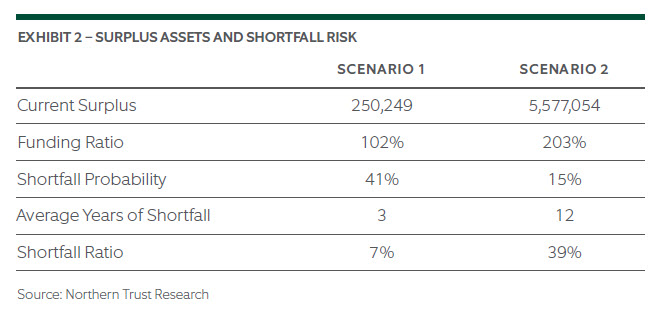

For scenario 1, the investor’s lifetime consumption is fully funded with a portfolio of intermediate-term Treasury bonds. Using the 2.3% expected compound return as the discount rate, the present value of $500,000 per year for 30 years is $10.75 million. The entire $11 million portfolio is invested in intermediate-term Treasury bonds. The funding ratio is calculated by dividing the current value of portfolio assets by the present value of the consumption goal. A 100% funding ratio indicates that lifetime consumption is fully funded by portfolio assets, on average. Scenario 1 results in a funding ratio of 102%, indicating a small current surplus (about $250,000). The compound return represents the mean or expected multi-period return outcome. We should expect that half of the outcomes will be worse and half better than the expected outcome. Monte Carlo simulation allows us to evaluate the spread of potential outcomes, both in terms of probability and magnitude of potential shortfall. The scenario 1 simulation indicates that lifetime consumption is successfully funded 59% of the time, which is higher than 50% due to the small initial surplus. In the other 41% of potential outcomes, the investor has a shortfall. But the magnitude of potential shortfall in these outcomes is relatively inconsequential: the average shortfall represents only three years of unfunded consumption and the shortfall ratio is 7%. The investor could easily adapt consumption to deal with this level of shortfall risk, if it were to manifest. The 41% shortfall probability does not fully capture the shortfall risk of this safe asset; the combined view of shortfall probability along with the magnitude of potential shortfall is more complete. In theory, the safe asset could be transformed into a risk-free asset by replacing the portfolio of intermediate-term Treasury bonds with a series of Treasury inflationprotected securities (TIPs), where the timing and magnitude of maturities are aligned with the pattern of consumption. Although this asset would have a similar expected return and standard deviation as intermediate-term Treasury bonds, it would be effectively risk-free in relation to funding the lifetime consumption goal because it is maturity-matched, inflation-protected and has no material default risk. Shortfall probability would be reduced from 41% to 0% (and there would be no magnitude of potential shortfall). But in practice, TIPS are issued in limited maturities (5-, 10- and 30-year) and interest income is heavily taxed, making implementation challenging as a risk-free consumption hedge for many high-net-worth investors.2

Scenario 2: High Risk, Larger Surplus Portfolio

For scenario 2, lifetime consumption is fully funded with a high-return, high-risk portfolio of emerging market equities. Using the 8.4% expected compound return as the discount rate, the present value of $500,000 per year for 30 years is just $5.42 million. The entire $11 million portfolio is invested in emerging market equities, resulting in a funding ratio of 203%. The high expected return results in a huge current surplus (about $5.58 million), which could fund twice the desired level of consumption! Consistent with a large buffer of surplus assets, the scenario 2 simulation indicates that lifetime consumption is successfully funded 85% of the time. It appears as though shortfall risk was reduced by simply owning a higher-return, higher-risk asset (i.e., as if risk were mitigated with high return). But in the other 15% of potential outcomes (a reasonable likelihood), the magnitude of potential shortfall is dramatic – averaging 12 years of unfunded consumption. And the shortfall ratio is 39%. This magnitude of potential shortfall could materially undermine the ability to fund a 30-year consumption goal. If this shortfall risk were to manifest, the investor would need to significantly reduce consumption. The 15% shortfall probability does not fully capture the shortfall risk of this risky asset; the combined view of shortfall probability plus the magnitude of potential shortfall is more complete.

CONSIDER TRADING SURPLUS FOR SAFE ASSETS

When evaluating surplus assets and shortfall risk, many investors rely on a buffer of surplus assets, or they consider the probability of a shortfall. We showed how the magnitude of potential shortfall is a key element of shortfall risk and an important consideration. Ultimately, there is some mix of safe assets and risky assets that suits the risk preference of a particular individual. But this risk preference should consider the benefit of trading some or all of a surplus for a higher allocation to safe (or risk-free) assets when funding lifetime consumption or other high-priority goals.

- For simplicity, we ignore taxes and inflation.

- Many high-net-worth investors prefer to use high-quality municipal bonds as safe assets.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.