- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Back To The Supply Side

Do tax cuts pay for themselves?

By Carl Tannenbaum

The current round of budget discussions in Washington will have a significant impact on America’s fiscal trajectory decades into the future. A key underpinning of this year’s debate has roots that go decades into the past.

Economic performance during the 1970s was dismal. Stagflation took hold, industrial companies nearly failed, and stock markets were stagnant. The Presidential campaign of 1980 centered on what to do about all of that: Ronald Reagan was elected by promising to set a new path.

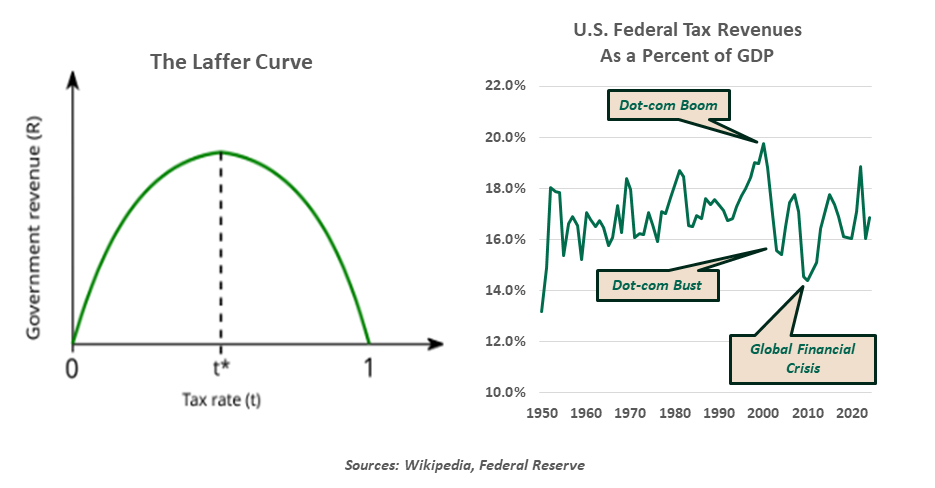

Among Reagan’s advisors was a 40-year-old economist named Arthur Laffer. Laffer’s research contended that high tax rates were simultaneously bad for economic activity and bad for government revenues. Theoretically, this thesis has substantial merit: high tax rates can be a disincentive to invest or even work. This limits potential growth and diminishes tax receipts.

The “Laffer Curve” illustrated the tradeoffs involved, and suggested that there was an optimal level of taxation that was much lower than the regime which was in place at the time. Using this as justification, the Reagan administration pursued a “supply side” approach to fiscal policy. Two major tax bills, in 1981 and 1986, brought the top marginal rate down from 70% to 28%. Levies on capital gains were also reduced.

Beware of overly optimistic budget assumptions.

Debate over whether Reagan-era tax policy worked as intended continues to this day. On the surface, the results appear favorable: U.S. equity markets performed very well in the 1980s, and the economy ended the decade in a much better position. But it is difficult to give tax cuts exclusive credit for these outcomes. The Federal Reserve used tight monetary policy to bring inflation down from 13.5% in 1980 to 4.8% in 1989. As inflation calmed, interest rates were cut, contributing to rising stock prices by reducing the cost of capital. And it spurred productive investment by increasing real rates of return.

Improvements in growth and market performance did not result in a better ratio of tax receipts to the size of the economy. With a handful of notable exceptions, U.S. federal tax collections as a percentage of gross domestic product (GDP) have been in a tight range for the last 60 years. U.S.

Federal debt as a percentage of GDP increased from 31% to 51% in the 1980s.

Arthur Laffer, then in his seventies, was front and center again when the 2017 Tax Cuts and Jobs Act (TCJA) was crafted. He contended that the program would allow the U.S. economy to grow at a rate of 6% without expanding the Federal deficit. The deficit did, however, continue to deepen in the years that followed. A study from Brookings of the TCJA concluded that the tax cuts had not come close to paying for themselves.

As we discussed last year, America’s budget challenges have many root causes. The nation’s demographics have increased the cost of critical government programs. Two major emergencies in 2008 and 2020 brought about extensive and costly public intervention. The return of interest rates to more normal levels has increased the burden of debt service. The country’s fiscal trajectory is unsustainable, and the financial markets have registered their concern by lowering the value of the U.S. dollar and raising the yield premium on Treasury securities.

Evaluating the results of any economic policy is incredibly challenging, as it requires isolating its impacts from other influences on performance. Conclusions are often colored by the priors of the author; this can be seen in the wide range of estimates surrounding the impact of tax cuts on activity. The fuzzy math surrounding fiscal strategies makes it very difficult to say with certainty what works, and what doesn’t.

But the risk introduced by the assumptions underneath the One Big Beautiful Bill Act should be carefully considered. Continued reliance on supply-side theories could make the long-term bill awaiting the nation’s taxpayers even larger than feared. Economists on both sides of the aisle suggest that we could very well be on the wrong side of the Laffer Curve…just not the side that Laffer himself might suggest.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.