France, Britain, And The Fight For Fiscal Credibility

Bond markets are growing skeptical of tight public finances.

By Vaibhav Tandon

Empires have not always fallen to invading armies. Some have withered under the quiet weight of debts they could no longer bear. History is littered with powers that were undone not by conquest, but by ledgers.

The Spanish Empire is a case in point: despite immense colonial wealth, the Kingdom declared multiple bankruptcies during the 16th and 17th centuries, drained by relentless wars and imperial ambitions. Its reliance on external lenders eroded its financial credibility and eventually, global influence. Today, echoes of that unraveling are seen in parts of Europe as fiscal pressures mount.

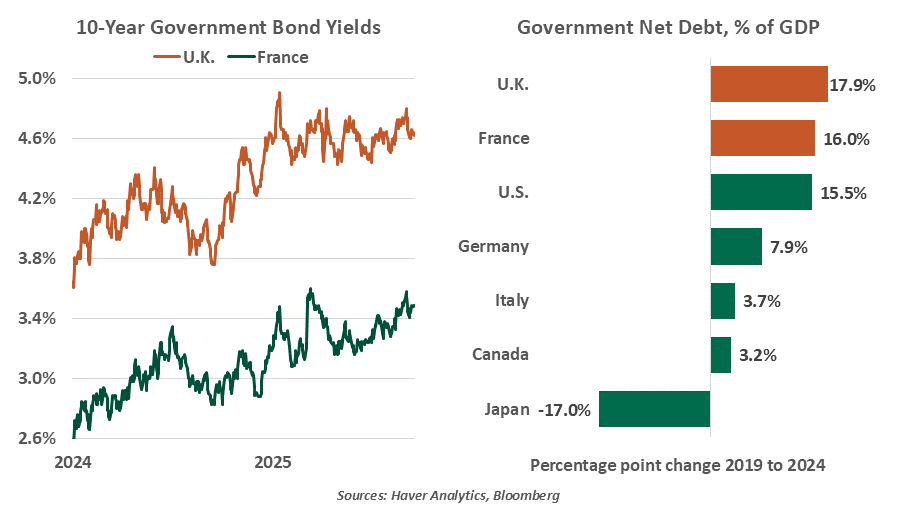

Long-dated yields have climbed to multi-decade highs across several advanced economies. Although some idiosyncratic factors are at play, elevated and rising public deficits are a common thread. France and the U.K. have drawn particular attention. In both cases, fiscal rules are either being breached or met by the tightest of margins on the basis of improbable assumptions. Political and fiscal uncertainties have made investors wary of committing to their long-term sovereign debt.

Yields on 10-year French government bonds surged to their highest levels since March, almost converging with those on Italian debt. In the U.K., 10-year rates surged to around 4.75%, up about a full percentage point from a year ago. The move has been even sharper for the longest maturities, with yields on 30-year French and British bonds climbing to their highest levels since 2009 and 1998, respectively. Investors are starting to reevaluate the safety of these sovereign debts, repricing risks to a level akin to corporate debt.

France, once a cornerstone of European stability, is now contending with one of the most difficult macroeconomic landscapes. The country is grappling with a rising public debt ratio and a fiscal deficit that remains stubbornly high at 5.5% of gross domestic product (GDP). Political fragmentation in the parliament, evidenced by four prime ministers in the past two years, has paralyzed reforms. The fractious legislature cannot agree on proposed austerity measures to rein in debt.

The new prime minister has signaled willingness to make concessions, including rolling back plans to abolish two public holidays and targeting a much more modest deficit reduction. But he is likely to struggle in balancing the competing expectations of financial markets and the public.

Demand is growing for a rollback of the 2023 French pension reforms, which gradually raise the retirement age from 62 to 65 by 2031. Reversing one of the few deficit-reducing measures passed in recent years would undermine market confidence in the French government’s ability to tackle its debt problem. These concerns appear to have contributed to Fitch’s decision last week to downgrade France’s credit rating by one notch to A+, the lowest among peers. Bringing public debt under control will require turning the primary deficit into a small surplus, a turnaround seldom accomplished in recent history.

The fiscal challenges facing France and the U.K. are testing the limits of market confidence.

With memories of the 2022 U.K. bond crash still fresh, Britain’s fiscal position is once again showing signs of strain. Alongside a fragile currency, it faces the highest borrowing costs and inflation among its peers. The U.K. government has struggled to contain a debt burden which has risen more than in any other Group of Seven economy over the past five years.

The British government is already spending around 8% of its budget on debt interest, double the pre-pandemic level of 4% and more than its outlay on education. Higher borrowing costs, feeble growth and policy U-turns have swiftly eroded the narrow £9.9 billion fiscal headroom unveiled in March, piling pressure on Chancellor Reeves to find £25 billion to avoid breaching borrowing targets. With little scope for more spending cuts and the tax burden approaching its highest level in over seven decades, public and political resistance to further tax hikes is formidable. These constraints have raised doubts about the government’s ability to adhere to its own fiscal rules.

That said, the U.K.’s public debt to GDP ratio is lower than France’s. Britain has also reduced its reliance on 30-year bonds for borrowing, reflecting diminished demand led by structural changes in the pensions industry. This suggests that, while Britain’s fiscal position is still challenged, it may be more manageable than France’s in the near term.

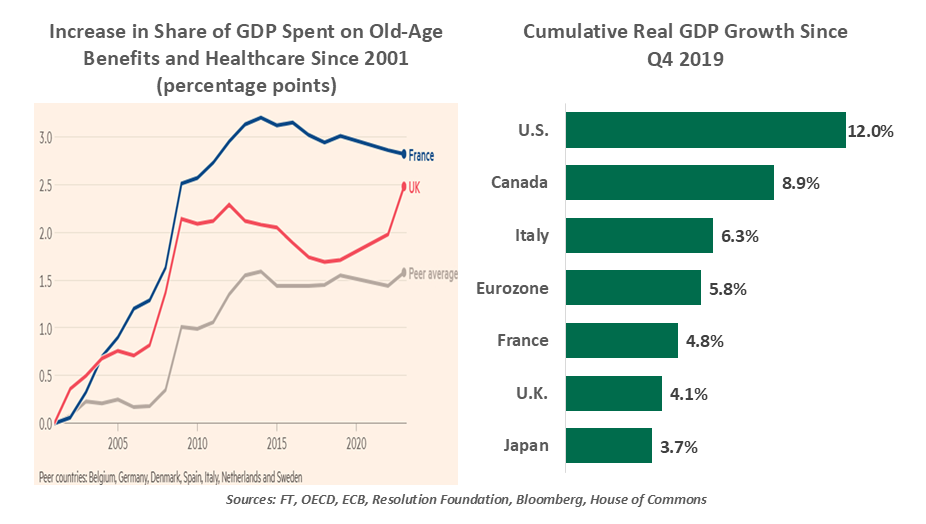

Demographics are also adding strain to both nations’ public finances. Though France and Britain’s demographic profiles are somewhat more favorable than those of other European member states, generous retirement systems are placing a significant burden on government budgets.

Generous retirement systems are placing growing pressure on public finances.

In France, spending on public annuities now accounts for a quarter of the national budget, with French pensioners receiving larger government payments than their counterparts anywhere else in the Western world. In the U.K., public disbursements to older citizens have climbed higher and faster than in peer countries. In both places, retirees’ incomes have grown far more rapidly than those of working-age cohorts, further complicating efforts to restore fiscal balance.

France and the U.K. need stronger economic growth to help shore up tight fiscal situations and meet demands for higher spending on public services. Unfortunately, neither of them has a recent history of investment and innovation; productivity growth in both countries has lagged.

In the coming few weeks, investors will be watching closely to see whether the French and British governments can restore fiscal discipline without undermining the trust of financial markets or the public. In an era where confidence is capital, the strength of a nation’s balance sheet may once again determine its standing.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.