- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Options Quarterly Commentary Q2 2025

The second quarter of 2025 was marked by pronounced market volatility as investors contended with tariff policy uncertainty and an escalating war in the Middle East. On April 2, President Trump’s ‘’Liberation Day’’ announcement of harsher than expected tariffs triggered a sharp sell-off, with the S&P 500 falling nearly 12% in a single week. The VIX soared in response to the tariff announcement, closing at VIX 52.5 on April 8, marking its highest closing level since April 2020, during the peak of the COVID-19 pandemic. President Trump’s subsequent 90-day tariff pause on April 9 triggered a 44% intra-day swing in the VIX, from being up 10% (reaching an intra-day high of 57.96), to down 34% at the close. SPX intra-day volatility doubled, surpassing the highs seen during 2020, and approached levels last seen during the 2008 Financial Crisis where the VIX traded 80+ both in 2008 and 2020 (CBOE). Markets staged a powerful rebound with stocks hitting all-time highs heading into quarter-end, supported by progress in a US- China trade deal, renewed investor confidence, a robust Q1 earnings season and growing optimism around potential rate cuts. The S&P 500 Index: SPX ultimately closed the quarter at 6204.95 (+10.6% vs Q1 2025). As noted by JPM equity derivatives research, equity volatility saw a rapid normalization following tariff de-escalation, with the VIX halving its peak in just 12 trading days, marking the second fastest normalization ever, with the VIX dropping around 35 points in the two months following the announcement. The CBOE Volatility Index: VIX closed at 16.73 (-27.2% vs Q1 2025).

Source: Bloomberg

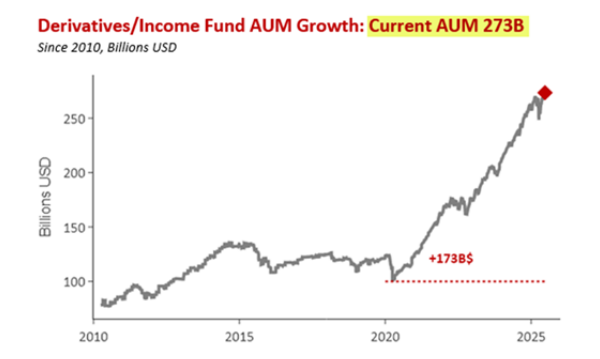

June options expiration marked the largest in history, with $6.5 trillion of equity options expiring. The event was particularly notable due to high levels of positive dealer gamma positioning which significantly suppressed volatility. These dynamics arise when market participants consistently sell more volatility than they buy. As a result, dealers are long gamma (long calls or puts) and to remain delta hedged, buy in dips, and sell in rallies. These hedging flows dampen volatility and create a pinning effect in equities. Following the June options expiration, the S&P was able to break out into a broader trading range due to the reduction positive gamma positioning. Volatility selling has been a trend that has significantly increased over recent years. A key driver of this are ETFs utilizing embedded options strategies that systematically sell volatility for income. These strategies have expanded rapidly over the last five years amassing to a total $237bn AUM (see below).

Source: Nomura

Another trend to note was the surge in volume in zero-date-to-expiry (0DTE) options in Q2 and according to the CBOE, May was the second highest month in 0DTE trading on record, averaging 2.11M contracts, or over $1.2T notional, a day (record is Mar2025 with 2.17M contracts ADV). The growth in 0DTE trading in May came on the back of a rebound in retail trading, which had dipped during the April spike in volatility. SpotGamma note a trend of reduced 0DTE flows during periods of high volatility, such as the April tariff turmoil as a result of 0DTE traders taking a back seat during these times, in addition to an increase in longer dated options activity for hedging purposes.

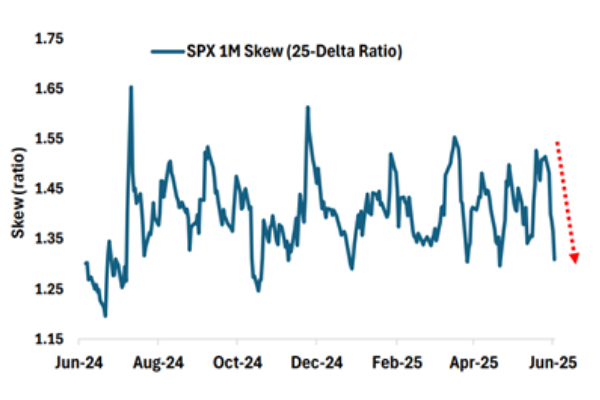

By the end of the quarter, equity implied volatility broadly declined as geopolitical risks in the Middle East subsided and tariff fears eased. According to CBOE, the majority of the VIX decline was driven by the S&P rally; however, a shift lower in the volatility surface and SPX skew flattening accounted for roughly a quarter of the decline. They note the decline in skew was primarily concentrated in the front month (as shown below), indicating the move was largely driven by ‘’FOMO’’ type call buying as a response to the market rally.

Source: CBOE

Typically, during the summer months, market volatility tends to be elevated largely because of thinner liquidity, which can lead to sharp and unpredictable price swings. Looking ahead to Q3, equity volatility is expected to climb ahead of the upcoming tariff deadlines, particularly with the S&P trading at a record high. CBOE has highlighted the emergence of the ‘’spot up / vol up’’ dynamic as we enter Q3 reflecting a scenario where both equity markets and implied volatility are rising in tandem. This pattern suggests that investors are becoming increasingly concerned over key trade policy developments over the coming months and therefore increasing hedging activity.

Options involve risk and are not suitable for all investors. Call for a copy of the Options Clearing Corporation (“OCC”) Disclosure Document entitled "Characteristics and Risks of Standardized Options." Please read it carefully before investing.

Confidentiality Notice: This communication is confidential, may be privileged, and is meant only for the intended recipient. If you are not the intended recipient, please notify the sender as soon as possible. All materials contained in this presentation, including the description of Northern Trust, its systems, processes and pricing methodology, are proprietary information of Northern Trust. In consideration of acceptance of these materials, the recipient agrees that it will keep all such materials strictly confidential and that it will not, without the prior written consent of Northern Trust, distribute such materials or any part thereof to any person outside the recipient’s organization or to any individual within the recipient’s organization who is not directly involved in reviewing this presentation, unless required to do so by applicable law. If the recipient is a consultant acting on behalf of a third party client, the recipient may share such materials with its client if it includes a copy of these restrictions with such materials. In such event, the client agrees to comply with these restrictions in consideration of its accepting such materials.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.