- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Options Quarterly Commentary Q3 2025

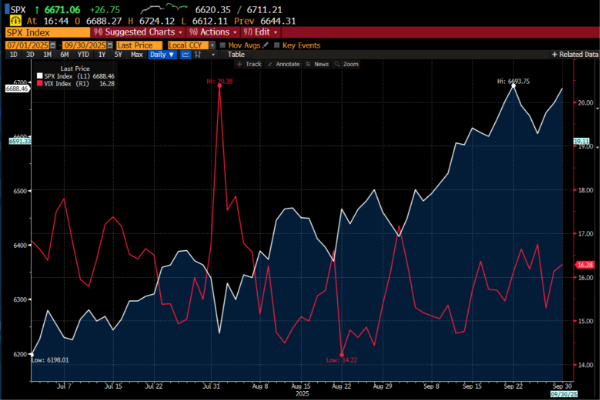

US equities posted strong gains in Q3 2025, setting multiple record highs. The rally was fueled by easing trade tensions, resilient economic data, robust corporate earnings, and continued optimism around artificial intelligence growth. This was further supported by the Federal Reserve initiating a new rate cutting cycle with a 25bp cut at its September meeting, whilst signaling further easing ahead. ‘’Magnificent Seven’’ stocks continued to lead the market, with the information technology sector advancing 13.2%. Corporate earnings growth for the S&P 500 reached 12%, well above expectations of 7%. In addition, markets saw record-setting rallies in both gold and silver. The S&P 500 Index: SPX ultimately closed at 6688.46 (+8.1% vs Q2 2025). Volatility was moderately choppy, with the VIX moving within a 7.78 point range for the quarter. The biggest move was driven by the sharp downward revision to U.S payroll data (for May and June) on August 1, causing the VIX to spike to 20.38. The CBOE Volatility Index: VIX closed at 16.28 (down -2.7% vs Q2 2025).

Source: Bloomberg

Volatility compression occurred throughout the quarter alongside the steady climb in equities. SpotGamma attributed this low-vol regime to heavy positive dealer gamma positioning as a result of 0DTE flows, dampening market movement. 0DTE options-selling forces dealers to hedge by buying into declines and selling into rallies, explaining the drop in realized volatility as the market achieved all-time highs.

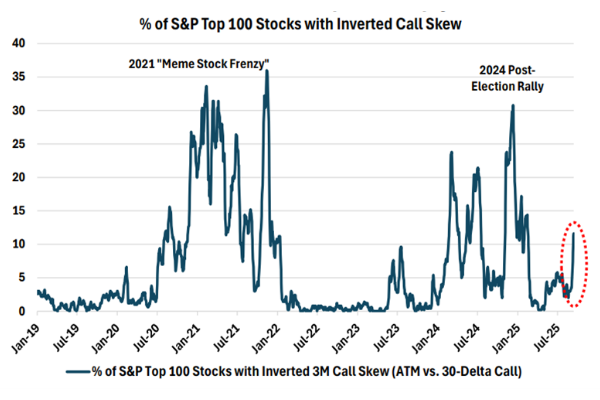

The options market showed little concern ahead of the September FOMC meeting, implying only a 0.7% swing in either direction, the second lowest projection in 18 months (Susquehanna). Post meeting, options activity surged led by single stocks, reaching a record high of 54 million contracts traded on September 19. A large portion of this was call buying which pushed the put-call ratio down to a three- month low of 0.45 (CBOE), highlighting a strong bullish sentiment. This was further reflected in the proportion of stocks trading with inverted call skew which is typically a sign of elevated optimism (see below).

Source: CBOE

US listed options volumes reached new all-time highs in Q3, averaging over 53 million contracts per day. It was noted by NYSE that the customer segment (as opposed to market makers) now accounts for nearly 46% activity, the highest share since late 2021. FLEX options also saw robust growth, with 1.2 million contracts traded daily (NYSE).

Towards quarter-end, volatility compression began to reverse with markets entering a ‘’spot up, vol up’’ dynamic, where the S&P reached all-time highs and volatility simultaneously rose. Investor sentiment wavered amid concerns around a government shutdown causing the SPX 1m implied-realized vol spread to double to 5.0% (76% percentile), indicating a growing gap between implied and realized volatility (CBOE).

The five-year average correlation between the SPX and the VIX is -0.88 (Bloomberg), reinforcing that rising equity markets typically coincide with lower volatility. When this relationship breaks down, as it did on 10% of trading days in 2025 so far, it often signals markets are overheated (Nomura). Nomura highlighted that this breakdown tends to occur when investors are heavily positioned in equities and a further rally increases downside hedging demand, which steepens put-call skew and drives the VIX index higher. Conversely, if investors are underexposed, a rally can spark a rush to buy. They note that in this instance the latter occurred, and an elevated call skew increased demand for call spreads, most notably in technology stocks.

As we head into Q4 and year-end, there has been a noticeable uptick in demand for protection, indicating that investors are looking to lock in gains and hedge against potential drawdowns. Tail hedging has picked up significantly, evidenced by the S&P 500 3-month 25-delta skew steepening from the 40th percentile to 70th percentile (CBOE). There was a sizeable VIX options trade on September 29 where one market participant bought 113,000 contracts of VIX November $32 calls, spending a total of $9.7 million in premium (Bloomberg).

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.