- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Global Economic Commentary | March 25, 2026

A New Chapter

The Iran conflict has changed the paths for inflation and central bank actions.

The conflict in Iran has brought rapid consequences for the global outlook. All nations will be challenged by a curtailed supply of commodities and the higher prices that ensue. The impacts will be greatest for nations that are more reliant on imports of energy and other critical materials. War-related inflation will complicate decisions for central banks; rate reductions are off the table. Some will contemplate rate hikes, though they are an imperfect solution to inflation caused by supply shocks.

This outlook assumes the Iran situation carries on at its current intensity, without substantial escalation, before the involved parties move toward a ceasefire. The longer that hostilities continue and the Strait of Hormuz remains impassable, the greater the downside risks. Even if a ceasefire takes shape and trade flows resume, a complete return to prior levels of activity will take months, and potentially years in the case of destroyed energy infrastructure. We have adjusted our growth expectations accordingly.

Despite the fog of war, developed markets have demonstrated their ability to grow in the face of uncertainty. Consumption carries on; most countries’ labor markets are firm; trade tensions have lost some urgency; past rate reductions are now stimulating with a lag. For now, our outlook for major markets remains one of modest growth.

United States

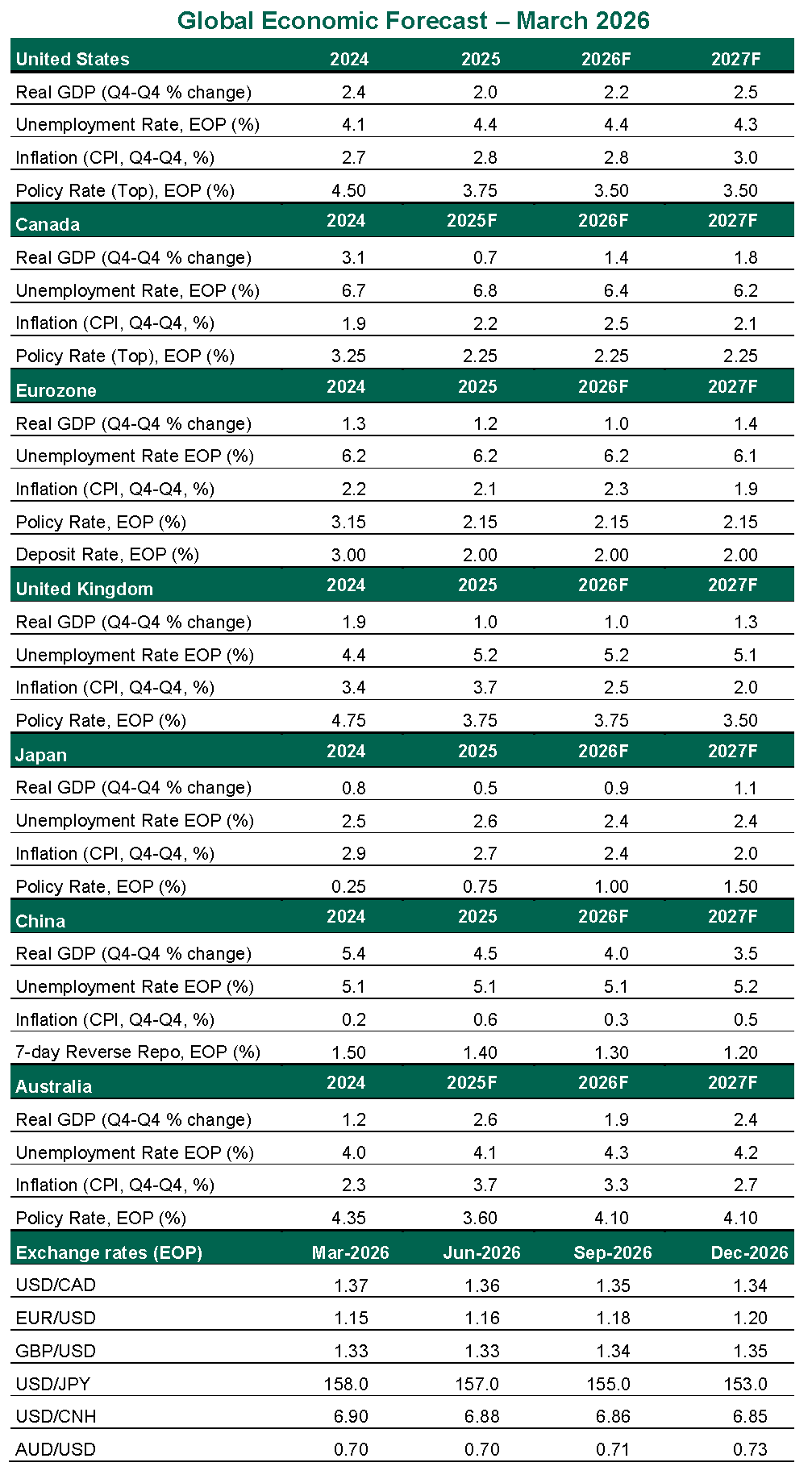

- The U.S. is relatively insulated from the consequences of the conflict, with ample domestic supplies of energy and fertilizer. However, commodity prices are set globally, and higher costs are already evident. Energy expenditures will offset some of the near-term gains from a more favorable year of income tax returns. Inflation had already been stuck above target, with services prices showing modest acceleration. The February employment report revealed a surprising decline of 92,000 payrolls and a rise in the unemployment rate; the labor market is sluggish at best.

- Expectations of a Federal Reserve rate cut hung on a stable inflation outlook, which is now in jeopardy. We now expect no further rate cuts until late in 2026, with risk of a further deferral or even a hike should inflation prove persistent.

Canada

- While no nation is better off from global circumstances, Canada is well-positioned to weather the energy market surge. The nation’s fuel supply is secure, and as an energy exporter, it stands to gain from higher prices. Prior to this uncertainty, the Canadian economy had been slowing; the February unemployment rate rose two tenths to 6.7%, undoing the progress shown in January. Overall growth showed declines in the second and fourth quarters of 2025, though gains in the first and third quarters delivered an adequate real gain of 1.7% for the full year. Economic slack should help to buffer inflationary shocks from energy prices.

- The Bank of Canada held rates steady at its March meeting, and we expect no further policy changes. Inflation worries will be offset by limited growth and signs of a deteriorating labor market. Policy uncertainty looms with the U.S.-Mexico-Canada Agreement due for renegotiation this summer. U.S. leadership has a preference for bilateral engagement, which may leave Canada exposed to sudden changes in its terms of trade.

Eurozone

- Europe was still recovering from the Russia-Ukraine energy shock when the Iran war commenced. Liquified natural gas (LNG) shipments from the Middle East had helped to restore some of the missing energy supply. Imports from Norway and the U.S. will help to ensure a steady flow of LNG in many nations, but higher global prices will be felt across the bloc. Industrial economies like Germany will remain challenged, and a more tense trade environment will not support export prospects. However, Europe’s labor markets remain tight by historical standards, with the unemployment rate reaching a record low of 6.1% in January.

- The European Central Bank had entered the year judging that monetary policy was in a “good place.” Now, its confidence in stable rates has been shaken. We expect a slow and challenged growth outlook to balance any contemplation of an inflation-fighting rate hike, leaving the rate outlook flat for the year ahead. Middling growth, higher rates and higher inflation are pushing the regional economy to the verge of a cycle of stagflation.

United Kingdom

- The U.K. entered the year with lackluster activity and a slowing labor market. The three-month moving average surveyed unemployment rate rose eight tenths to 5.2% in the course of 2025, with momentum toward further increases. The Office of Budget Responsibility forecast only 1.1% gross domestic product (GDP) growth in 2026, following 1.4% growth in the prior year, even before complications arose in the Middle East. Core inflation has run at 3.4% over the past year, modestly reaccelerating in recent months. Policy options for a slow but inflating economy are limited.

- The March meeting of the Bank of England’s Monetary Policy Committee (MPC) ended a four-year run of split decisions and varied opinions among Committee members. The MPC unanimously held rates steady and expressed that tighter monetary policy could be needed if the surge in energy prices proves “larger or more protracted.” The U.K. entered the year with more elevated inflation than most developed markets, and a further inflationary shock makes the risk of higher rates more credible. We have set aside our prior expectation of two rate cuts this year, but we don’t yet foresee rate hikes. Current rates are already restrictive, warranting patience. Easing may resume next year, once the effects of the crisis subside.

Japan

- Japan’s fourth quarter gross domestic product was revised up to show a 0.3% quarterly gain, reflecting better momentum as the economy entered a more complex year. Unemployment remains stable. Four years into a run of positive inflation after years of falling prices, core inflation touched a cycle low of 1.6% year-over-year in February. Much of the nation sets its wage gains in a public, national Shunto renegotiation each spring; inflation could raise the risk of wage demands that spark a modest wage-price spiral. Fiscal concerns may re-emerge as the government makes plans to reduce taxes on food and offer subsidies to keep fuel prices affordable.

- Japan is especially exposed to imported petroleum prices, with over 90% of its oil and 20% of its LNG flowing through the Strait of Hormuz. Large reserves offer a cushion, but higher prices will still weigh on the nation’s prospects. While other central banks may be circumspect about reacting too quickly to higher energy prices, the inflationary shock will cement the Bank of Japan’s course of rate hikes. Sustained wage gains will also allow the central bank to continue gradual normalization.

China

- Relative to other markets, China is in a favorable position entering a challenging interval. The nation has the world’s largest strategic petroleum reserves, and it maintained oil trade with Russia while other nations levied sanctions. Export controls on fertilizer will hedge against crop deficiencies. These ounces of preparation help to insulate it against the current shocks. And if some global inflation gets past these defenses, China’s nearly three-year run of flat prices should make the inflation more tolerable. But all these buffers do not offset the challenging position the country was in to start the year.

- The National People’s Congress set a real growth target of a 4.5%-5% for this year, its lowest since 1991. Leadership recognizes the combined challenges of a declining population, slower export markets and significant debt service obligations. Prospects for further policy support are limited; the nation is settling into a slower but more sustainable rate of growth.

Australia

- The Australian economy reaccelerated to end 2025, gaining 0.8% in the fourth quarter and 2.0% across the full year. The unemployment rate has been rangebound at 4.1%-4.3% over the past five months. Inflation remains elevated above the central bank’s target range, standing at 3.7% year over year in February. The economy was on a firm footing ahead of the global disruption, with lingering inflation its greatest challenge. Australia is highly exposed to global fuel prices, and will be sensitive to the global energy shock.

- The Reserve Bank of Australia is taking inflation risks seriously, raising its policy rate to 4.10% at its March meeting. We had expected that firm inflation would bring about a hike regardless of geopolitical circumstances. The current rate is sufficiently restrictive in the face of inflationary risks, and we expect no further changes for the foreseeable future.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.