- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Weekly perspectives from Gary Paulin, Head of Global Strategic Solutions, on global market developments and their potential broader implications

March 23, 2024

PEAK PLUMBER, GOLD BEANS AND ASKING YOURSELF: WHAT'S MISSING?

Riding several horses with only one bottom

I found it hard to take everything in this week, so much that it felt a bit like trying to ride several horses at once. Harder still to identify the signals, with news flow filled with confusion and contrast. Central Bankers were full of contrast. Take the Turks, where headlines read: “Turkish annual consumer price inflation soared to 67%, fuelling concerns the central bank might have to return to tightening”. Ya reckon? And so they did, lifting rates 5% to 50%. Luckily, for the Turks, they have been hoovering up gold and now have the 11th largest reserve on the planet. Just think what a digital version of gold could do to their balance sheet (more on this later). But Turkey wasn’t the real story this week. Nor was digital gold.

The real story?

So, where was the real story? Was it in Japan, where Shunto wage inflation unshackled the JCB to lift nominal rates into positive territory, for the first time in 17 years. Nope, that didn’t do much other than remind folks that real rates remain decidedly negative, great news for supply constrained assets like Japanese real estate which had its best week in years and stocks, especially exporters given continued weakness in the Yen. The FED and BOE cooed as if it was an election year. The Swiss cut. All this dovishness the same week commodities rallied, suggesting 2025 could get very interesting (and why the chart below remains a relevant framework). Redditt captured the exit hopes and dreams of private equity (PE) barons and their LP investors, when it opened +50%, signaling perhaps the real return for IPO exits, after a few false starts last year. Yet, in contrast the press were quite damming on PE, with articles that may have had more import had they been written a year earlier. That said, expecting PE to return this decade what it did last is, I believe, a stretch for reasons we’ve discussed.

All assets are cyclical

It's fairly mechanical, but markets have a tendency to mean revert. The weight of money sees to that, and there’s no shortage (of money) in PE. But it still has a role, albeit a changing one as the ability to ‘smooth returns’ conflicts with regulator demands for greater NAV transparency and independence. Removing the mystery will remove (some of) the margin. However, I’m not here to beat up on PE – the FT and The Economist have done a good job of that this week. PE still provides access to themes not in public markets and there are still potential opportunities in distressed and secondaries, especially. But instead let me offer an alternative asset. One where compound dividend growth could surpass the current level of average cash returns (or DPI, more also on this shortly) by the end of the decade, if not sooner. Done using no leverage, with lower correlation and without any asset appreciation. No, not magic, but something far more mundane (read on). But even that’s not the big story this week, nor was it the World Petrochemical Conference in Texas, President Xi’s party invitation (I’ve said previously that team-spirit is found at the bottom of a pint-glass), the Justice Department’s lawsuit against Apple, Nvidia's ‘Woodstock of AI’ or that Elon Musk believes we will run out of electricity next year. No, the biggest news of the week is: get used to blocked toilets for we are running out of plumbers.

Peak plumber

Part of my hesitation of going all in on the disinflation narrative, lest as it relates to the productivity miracle from AI, is that AI’s benefits will be unevenly distributed. Yes, AI will, perhaps ironically, help replace knowledge workers or coders, but what of blue-collar jobs like construction, which faces a generational cliff on the eve of the world’s largest ever construction project? Like any supply-constrained commodity, pricing power will grow with demand – a relevant observation given that labour as a share of profit is near generational lows. We’ve already discussed this in light of builders, miners, munition makers and manufacturers but not in terms of the world’s previous productivity miracle – plumbing (yes, the Victorians in the UK still trump Silicon Valley in terms of impact to GDP). Where, despite the allure (okay, it’s a hard sell), we simply can’t find enough plumbers to replace those retiring, leaving us 550,000 short – in the US alone. And correct me if I’m wrong, but I’m yet to see AI swing a hammer, spotweld, or fix a leaking pipe. The greater scarcity – and therefore value – may not lie in the code. But in the commodity.

Copper, the new cocoa?

It seems to me that fundamentals matter less than they once did with commodities. You can probably thank MIFID II (with its impact on research) and the rise of machines (and indexation) for that. But when they matter, they really matter. Take cocoa. Or even Bitcoin. For months prior to the recent spikes there were warnings of looming supply scarcity. Things had to get to an extreme level before a price reaction occurred – and what a reaction it was (2x – 3x in 12 months). And this is the point about commodities. Supply is the determinant factor in price formation. But thanks to a lack of fundamental commentary or focus thereon, the market has ignored the supply crunch that’s looming due to years of underinvesting or resource nationalisation. What’s happened to cocoa will happen in other commodities, like copper – which showed glimmers of form this week. Should we awake to a ‘break-out’ you know the story that will accompany it. A story already scripted but not properly sold. Inventories have been depleted, stocks-to-use ratios are near lows and the market is in deficit thanks to more than a decade of under-investment. This as China reflates and the world commits to its largest ever construction project – the climate transition. And if contango puts you off buying futures, buy stocks with claims thereon, for many even provide you with a positive carry. A curious thing, to PE investors, known as a dividend.

“Dividend is the new IRR”

According to the Economist, it’s now possible to buy t-shirts emblazoned with the slogan “DPI is the new IRR” on Amazon. DPI (Distribution to Paid-In Capital) is a measure of cash returns as % of paid-in capital. It has fallen to record lows recently of 11.2%. While I do believe current vintages will improve on that, and PE still has a role to play in asset allocation, I would, nevertheless, like to offer you a new alternative, one that requires no leverage, provides uncorrelated returns, and that should cash compound in real terms to levels well above DPIs within about 5 years, if not sooner. And that’s without any asset-price appreciation, activism or excessive risk taking. The alternative asset is called a “dividend”, particularly those of UK stocks. Why, because UK corporates are busy ‘eating themselves’ to starve off being eaten (probably by PE). In other words, if you assume corporates commit to buying back about 5% of their float each year (many are well north of this) with say 5% dividend growth on starting yields of 4% (the FTSE average) then returns could triple within a decade. Add 30% or so leverage, which alternative investors seen happy with, and you could be getting high teens returns, with bond like volatility. And that’s with stocks going sideways. Who knows, you may even get lucky if there is a value transfer from ethereal to material world assets, or more commodity supply chain pressure. Or both.

What’s missing?

During WW2 extra armoury was applied to RAF bombers in areas considered most likely to be hit. This area was identified where planes received the most bullet holes – the wings, tail and fuselage. The problem, this only focused on returning planes whose holes were not fatal and ignored those still missing (whose holes presumably were). This led to an inaccurate picture of risk and therefore, effective prevention. Luckily, a famous statistician, Abraham Wald, discovered the flaw and saved many lives. What he did for pilots, CIOs must do for portfolios. They must consider what’s missing. For risks lie as much in what they own, as what they don’t. And many don’t own much small/midcap or international equities, commodities or gold. Things I would consider now. Before the campaign begins.

Golden beans and physical bitcoin

“Big Gold Rally Surprises Wall Street”, screamed the front page of the WSJ when I was in Chicago last week. Other articles pointed to the ninth consecutive week of ETF outflows and a well-known multi-asset fund ‘turning bearish’. So despite investor/retail disdain, why the gold strength? Well, as we’ve discussed, it’s mostly due to central banks, certainly those outside the US sphere of influence who are busy accumulating. This is not uncommon during periods of geopolitical tension (it happened prior to both world wars and as a reserve asset, gold has displayed lower downside volatility than USTs recently. Beyond that, gold helps protect against a policy-mistake akin to ’68 where rates were cut despite a low output gap (sound familiar?). And I think the market may be warming up to the idea that while ETFs are currently unpopular, gold beans are not, especially not for Gen Z’ers in China looking for a safe place to park their cash.

But the reason I’m excited by gold is: I just watched bitcoin triple. And if you listen to the Bitcoiners, they will entice you with compelling logic like; ‘supply growth is set to half, so if every US millionaire – about 24m or so – tried to buy just one bitcoin, there would be a 6-7m shortage). Oh and it’s 'digital gold' and likely going to ‘eat’ physical gold, for it can’t be easily transported, is not divisible, nor readily available (on your iPhone).'

But what if it was? What if gold created a digital coin that was backed by physical, and therefore portable, divisible and available. What then? This could fix the sovereign debt problem and give boomers a legitimate entry point into digital assets. And provide the young with a way into gold Well, as I’ve mentioned in recent weeks, this is exactly what the World Gold Council is trying to do.

Finally, some common sense!

I was delighted to read in The Times the UK Chancellor is considering allocating some of the NatWest share giveaway to public schools in order to improve their financial literacy, and possibly even tap into their gaming tendencies via stock clubs and competitions. Literacy is one thing, fear of missing out is another! As I wrote last year: “…change needs a champion. It also needs the youth”. Another point made was that if the government wanted to use NatWest as a way to excite the youth, then, those shares had better go up. A lot. Few things are as powerful as price. Well, this week I was equally encouraged to see NatWest seek permission to increase their buyback allowance from 5% to 15%. And that’s with a starting dividend yield of 6%. Perhaps that’s even bigger news than our impending plumbing shortage.

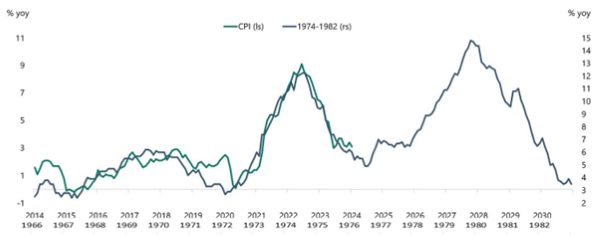

The most annoying chart in the world

Source: Bloomberg, BLS, Apollo Chief Economist

With apologies – but on the question of whether we may soon see 1970s-style reflation, the above chart (seen before), may provide food for thought…

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.