- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Criticism Of The Fed: Rule, Not Exception

Central banks work best when left independent.

By Carl Tannenbaum

As we’ve gone increasingly cashless, I will confess to some nostalgia for the artwork that adorns paper currency around the world. Notable local figures often feature, a tribute to national histories.

One of the more ironic examples of this practice is the presence of Andrew Jackson on the U.S. twenty dollar bill, which is a Federal Reserve Note. Jackson, the 7th President, was no great fan of central banks: he was chiefly responsible for closing one of them. That action initiated a 70-year interval in which the United States did not have a central monetary authority which could backstop the financial system.

I was thinking about this historical anecdote as strains between the Fed and the White House recently escalated. While the openness and negative tone of recent statements has surprised many observers, friction between national leaders and their central banks is quite common. While some tension is to be expected, enforced distance between the two is critically important to long-term economic and market performance.

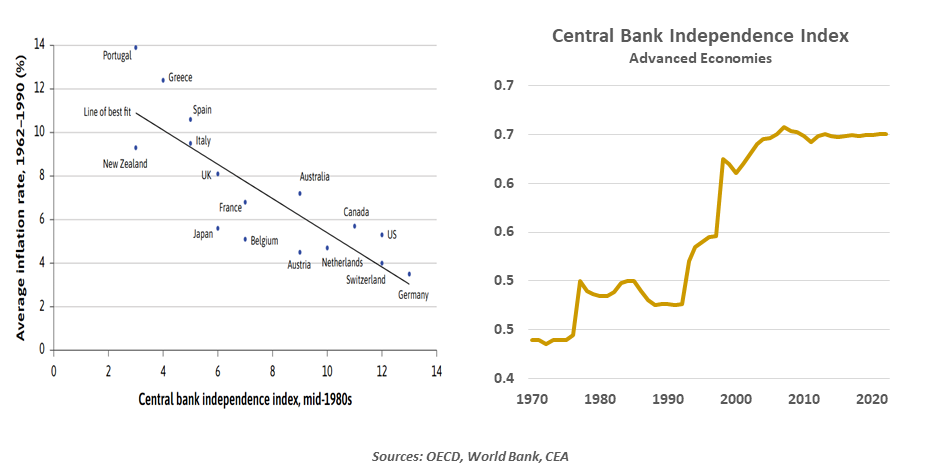

In recent times, central bank independence has been taken as gospel. Political pressure for easy money contributed to extremes of inflation in the 1970s. In the U.S., Paul Volcker took the helm of the Fed in 1979 and started to tame the price level, at great political cost to the president who had appointed him. But Volcker persevered, and the outcomes vindicated his approach.

This experience led many of the world’s other central banks to pursue strict monetary control, without interference from their governments. Studies have consistently shown that countries with the most independent monetary policy have had lower rates of inflation. Low inflation, in turn, is positive for employment, corporate profits, and market performance. Indices of central bank independence rose sharply in the 1990s, and have remained high ever since.

But in the much longer history of humankind, the past few decades are the exception and not the rule. Control of money and credit can influence a range of economic and social outcomes, and so it isn’t unnatural for governments to seek influence. The monetary history of the United States illustrates this well.

Central bank independence is a relatively new concept.

The First Bank of the United States was the creation of Alexander Hamilton, who served as the initial Secretary of the Treasury. He had argued persuasively in The Federalist Papers for centralized management of debt and money. Congress chartered the Bank in 1791 for a twenty year period, but the Bank’s charter was not renewed after the states raised concerns over its operation.

Following the War of 1812, American finances were in disarray. In 1816, Congress authorized the Second National Bank to restore stability. When Andrew Jackson was elected President in 1829, however, he immediately attacked the legitimacy of the Bank. Congress initially resisted, but was ultimately unable to overcome a Presidential veto of an extension to the Bank’s charter. It closed in 1841.

Without a central bank, the United States endured a long series of financial panics. The most major of them came in 1907; only intervention by J.P. Morgan himself prevented a complete meltdown. Soon thereafter, the idea of a central bank gained traction again; the Federal Reserve Act was signed in 1913.

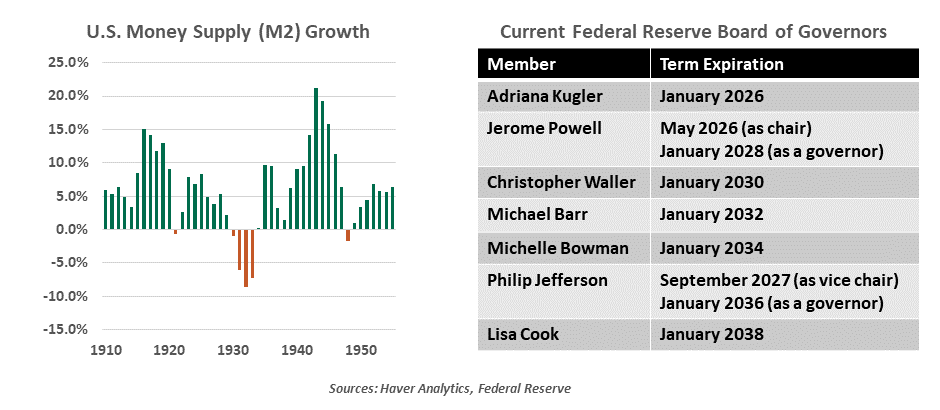

The Act was designed to ensure the Fed’s independence. Governors of the Federal Reserve System were granted long terms, and twelve regional Federal Reserve Banks were created across the country. The Presidents of five of those banks, along with the seven governors, vote on monetary policy. As powerful as chairmen are, they do not individually control the financial system.

During the Second World War, the Treasury asked the Fed to assist in financing the effort. The money supply was allowed to grow at an elevated rate, with the proceeds invested in government bonds. When inflation raged after the war ended, the Fed sought to re-establish its independence. An accord was signed in 1951 that created a clearer separation between the central bank and the government.

Against this longer sweep of history, the President’s recent criticism of the Fed is not that unusual. Nonetheless, the financial markets viewed it with great apprehension. Markets struggled for several days after the initial volley, but settled after the president reassured that he had no intention of trying to dismiss the chair.

To date, there has been no hint of reopening the Federal Reserve Act; Congress would be unlikely to support such an initiative. And the markets have registered their concerns over any suggestion that monetary policy could become more politicized.

The Federal Reserve is structured in a way that limits the influence of politics.

The White House will get an opportunity to shape the direction of monetary policy through its appointments to the Board of Governors. Two seats, including the chair, will open next year; other vacancies could arise if sitting governors leave the Fed for other pursuits. But it will be difficult for the administration to engineer a majority on the Federal Open Market Committee anytime soon.

I attended a large-scale luncheon at a hotel recently, where I was required to check my outerwear. When I went to retrieve my coat, I realized that my wallet (as usual) was devoid of currency. Not a problem: a placard with a QR code was posted on the table, linking to a site which facilitated cashless gratuities. It was another reminder of the incredible transformation in the payments space that has occurred during my lifetime.

The speaker at the lunch was none other than Jay Powell, the current Fed Chair. He made an articulate case for independence, and vowed to resist efforts to compromise it. He earned a huge round of applause for his remarks. Perhaps his face should one day be featured on the twenty dollar bill…or on the landing page opposite a QR code.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.