- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Gold Has Many Buyers

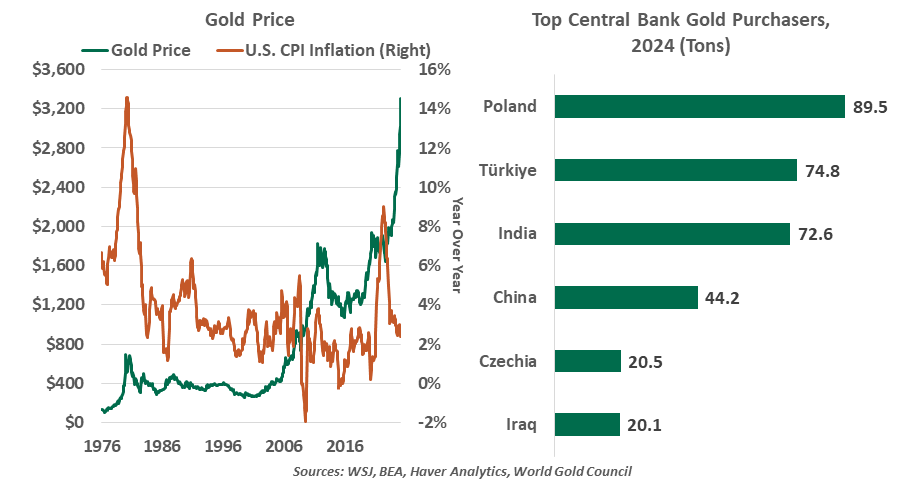

Major buying by central banks has fueled gold's rally.

By Ryan Boyle

Most economists and portfolio managers are cautious when discussing gold. Its handling and transaction costs are high, and it pays no interest or dividends. Outside of a few industrial uses, gold is not a productive investment. In an average year, its price will hold steady. However, in the year to date, gold has rallied while most other assets have been challenged.

Gold has an uneven reputation as a store of value that can hedge against inflation. This was the story of the of the early 1980s, when gold ascended while costs of living surged. But for long intervals thereafter, the metal held a rangebound price while most other investments thrived. Most recently, gold failed to hedge inflation; it lost nominal value as prices rose in 2022.

Rising gold prices align with rising uncertainty.

Instead, the recent escalation in gold prices appears to reflect lower confidence in the U.S. dollar. The metal ran up in the wake of the 2008 Global Financial Crisis—both during the recession and for years thereafter, as the economy struggled and quantitative easing raised fears of a devaluation of the dollar. As a recovery took shape, gold prices cooled, holding steady again until recession fears started to bubble up in 2019.

As the American economy appeared poised for a slowdown last year following the COVID reopening, investor interest in gold returned. U.S. consumers found gold for sale in warehouse clubs, and Chinese consumers stocked up on gold beans. Institutional investor interest is also returning to precious metals, with a survey by investment platform Ortec Finance finding 38% of pension managers planned to allocate to gold to guard against inflation risks.

Central banks have long been major holders of gold. Demand from smaller countries for bullion has been strong since Russia’s invasion of Ukraine in 2022. Western nations responded to the attack with financial sanctions, locking up Russia’s foreign reserves. Other central banks may be less inclined to keep stock in dollars if they fear these holdings could be a vector of geopolitical risk.

While smaller nations are buying, larger nations are not selling. The U.S. Federal Reserve holds over 8,000 tons of the metal, followed by Germany, Italy, France, Russia and China holding over 2,000 tons each.

Gold has also gained the attention of presidential advisers. Plans have been floated to tap America’s gold holdings as an offset to upcoming tax and spending plans, or even to seed a sovereign wealth fund. Combining Treasury and Federal Reserve holdings, the U.S. sits on over 261 million troy ounces of gold. Marked to market, the value exceeds $800 billion and is still rising.

We have not heard the last about gold in this cycle. Avoiding the hype will be a test of our mettle.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.