- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

U.S. Jobs Report: Unfavorable But Unbiased

A cooler labor market was long in the making.

By Ryan Boyle

Revelrous college students joke that Thursday night is the start of the weekend. We do not have that luxury, especially with the first Friday of each month offering the U.S. jobs report, bright and early. For a run of several years, this has been a cause for its own sort of celebration, with job gains continually exceeding expectations. Last week’s report abruptly ended the party, with disappointing payroll gains and significant negative revisions to prior estimates. The cooler data sparked a backlash. How did the music die so rapidly?

The monthly Employment Situation Summary combines the results of two concurrent surveys: The Current Establishment Survey (CES) collects staffing data from businesses, and the Current Population Survey (CPS) asks households about their employment status. Robust statistical methods are used to extrapolate national trends from a representative sample.

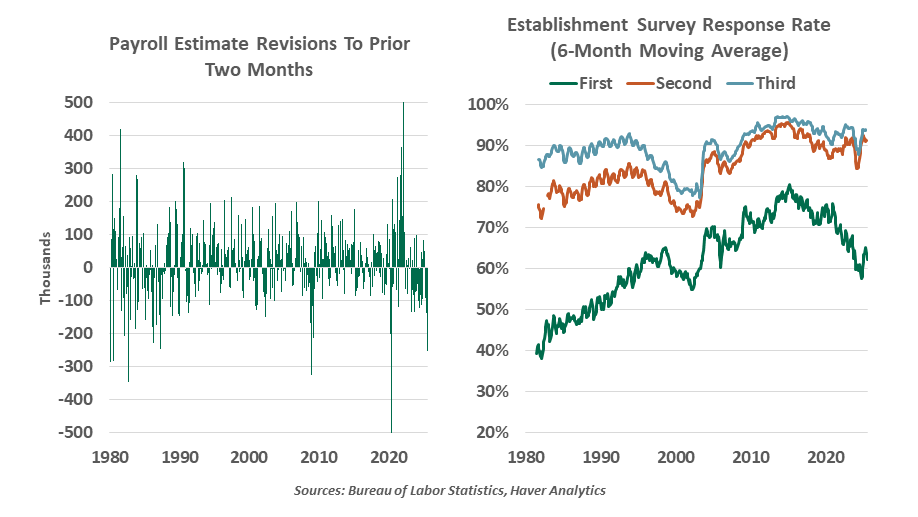

Every CES report includes revisions to the prior two months. Not all employers submit their responses by the initial deadline. Since the COVID-19 disruption, a declining proportion of businesses have replied on time. Smaller businesses in particular struggle to spare the resources to complete the surveys, and they are an important source of new jobs. This widening gap requires more use of estimation. The smaller the sample, the greater the margin of error.

Estimating activity across the U.S. economy is a tremendous task.

Estimating employment at small firms is further complicated by their lifecycle: every day, new businesses are formed while others cease operations. Sound data on business births and deaths is naturally lagged. Annually, the estimate of employment is revised to incorporate a complete census of employers, which has revealed an overestimate of the level of employment in recent years. While these revisions have not changed the direction of the trend (showing growth both before and after revision), the restatements have revealed that initial CES numbers were too rosy.

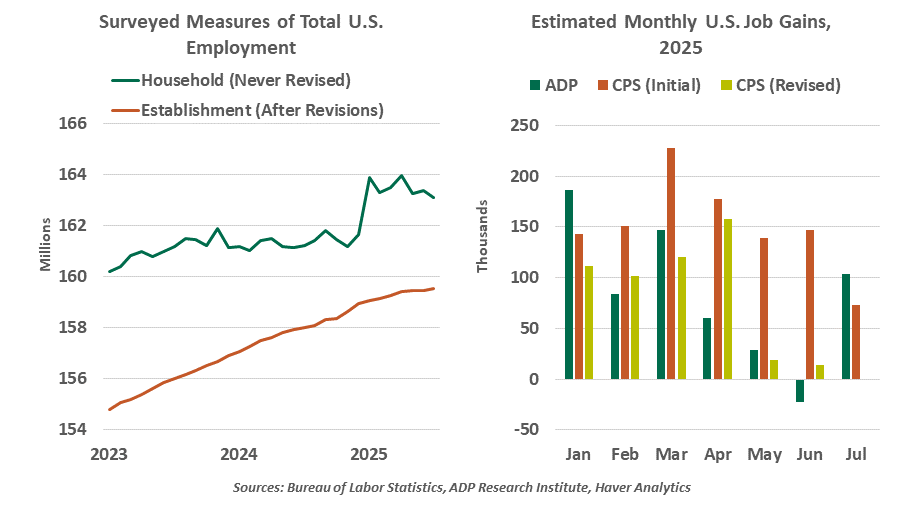

Revisions reflect the tradeoff between timeliness and accuracy. An optimal report would be correct and complete on its first publication However, a real-time enumeration of all employers would be unworkable and would still miss new business formations. When more survey responses arrive after the first publication, they should be used; a reliable revised figure is preferable to a noisy first estimate. Unlike CES, the CPS is not routinely revised, and is accordingly more volatile.

The stress around the July jobs report shows the importance of keeping all data in perspective. Any data point, favorable or otherwise, is not necessarily the start of a trend. All reports should be considered in context: are contemporary readings showing similar trends? Private sector surveys provide a helpful gut check. Trends published by job search sites Indeed and LinkedIn had showed slower hiring that would be consistent with lower job creation. The report from payroll processor ADP also reflected a slower pace of gains in the year to date. These findings set our expectations that the payroll report was poised to slow.

Though helpful, private data sources are not a substitute for foundational government data; indeed, these sources often use official data as a benchmark. The Bureau of Labor Statistics (BLS) and similar agencies produce figures used by innumerable businesses, investors and researchers to gain greater understanding of the economic environment.

Accusations of bias were used to justify the dismissal of the BLS Commissioner, but they are unfounded. Revisions have moved in both directions under all presidencies. Most months of 2024 showed negative revisions. And part of the slowdown in July was the ongoing loss of federal government jobs, evidence that Trump administration priorities are meeting their goals.

We defend and support the BLS. Its employees are well-trained, impartial and driven by the agency’s mission. But they have a large mandate and limited resources to meet it. The BLS’ sources and methods are reliable but cumbersome, still using paper mail and telephone interviews for some data collection. Amid a hiring freeze, the agency already needed to halt its price data collection for inflation reports in three geographies this year. The recent fiscal bill has reduced the BLS budget by 8% in fiscal year 2026.

A cooler job market will help to justify rate cuts.

To improve the reliability of the data, some investment is needed, at a time that the appetite for new government spending is severely curtailed. The new budget proposes to reorganize the BLS, Bureau of Economic Analysis and Census Bureau into a single statistical agency within the Department of Commerce. Efficiencies are possible, but so are oversights.

The subpar reading this past Friday was consequential to our outlook. The Fed has kept a cautious posture, holding rates steady since December in anticipation of higher inflation. They had the luxury of waiting as the job market appeared to be holding up. The July report showed a crack that makes a clearer case for easing to support the full employment mandate. We believe the Fed will cut in September, likely with more to follow. But rapid and large rate reductions are unlikely; the unemployment rate remains low, and inflation is holding above the 2% target.

Our outlook of an imminent cut discounts any political influence. Though the slow employment report was poorly received by the White House, it is exactly what’s needed to ease monetary conditions. A replacement for Governor Adriana Kugler (who resigned before her term had been completed) has been nominated, but may not be confirmed in time for the next Federal Open Market Committee meeting on September 16-17. One more dovish governor is unlikely to alter the committee’s decision.

We must also contemplate how many jobs must be created for “breakeven” growth. Job creation must keep pace with population growth to hold the unemployment rate steady; prior to this year, economists had estimated this required about 120,000 monthly gains. Today, amid heavy retirements and slow immigration, the labor force is not growing as rapidly as its old norm. While July’s gain of 73,000 jobs felt slow, these lower readings may prove sufficient to keep the unemployment rate contained.

The first Friday of each month may no longer be celebratory. We only hope that we won’t wake up to headaches that are too severe.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.