T+1 UK and Europe: The work starts now

Following the move to T+1 securities settlement in North America in May 2024, the United Kingdom (UK), the European Union (EU), Switzerland and Liechtenstein have now formally endorsed and are actively planning to transition their respective securities settlement cycle to T+1 on 11 October 2027.

Collectively this is a major task given there are over 31 Central Securities Depositories (CSDs), 18 Central Counterparty Clearing houses (CCPs) and 90 trading venues across the multiple currencies and countries involved. You could argue North America’s move to T+1 in May 2024 may prove to have been simple in comparison.

By Natalie Berkecz, Global Head of Regulatory Product, Northern Trust and Gillian Turato, Chief Operating Officer, Northern Trust.

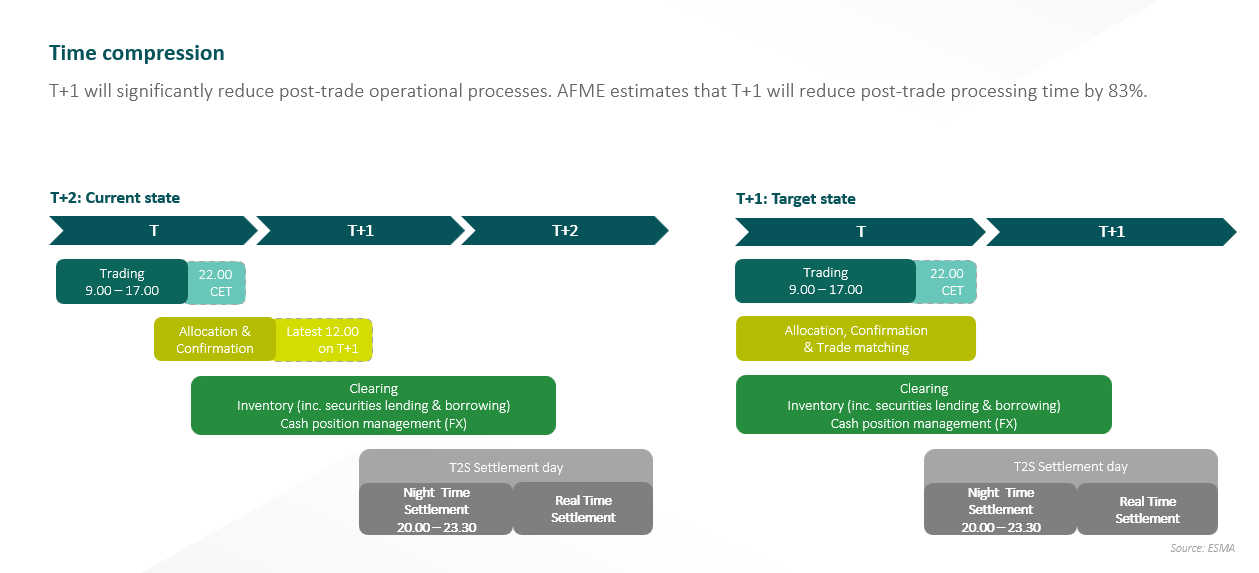

There are many reasons for late or failed settlements but analysing and understanding those causes is going to be key to your successful T+1 programme. In 2024, €70.43 million a month was paid on average in financial penalties for settlement failures on the European Central Bank (ECB) Target2-Securities (T2S) platform. According to a recent survey, 71% of respondees’ settlement failures in 2024 were caused by counterparty shorts and 21% were caused by data issues including those relating to incorrect or stale standing settlement instructions (SSIs).[1]

Cross-border alignment amongst European capital markets is welcome at this early stage of the process, with jurisdictions setting up governance structures to oversee this complex transition (e.g., "The EU governance structure" in the EU and "The UK Accelerated Settlement Taskforce" in the UK).

As seen during the North American migration, public and private sector collaboration will be crucial to effectively coordinate the various enhancements across the securities settlement post trade process chain. Due to the significantly larger number of stakeholders involved, compared to North America this will be a point of particular importance for the European migration.

While many firms will look to leverage the capabilities developed for the North America transition, the size, complexity and specificities of European capital markets will mean many firms will have to look beyond a “copy/paste” solution. This, in the context of legacy infrastructure and fragmented market practices, presents a monumental shift. In this article we explore the nuances of the European T+1 migration and outline areas firms should be focusing on at this stage of the planning.

Why are European capital markets transitioning to T+1?

European regulators have concluded that transitioning the securities settlement cycle to T+1 presents significant benefits to European capital markets.

- Risk reduction: reducing the number of days between trade execution and settlement reduces counterparty, market and credit risk.

- Cost reduction: reducing exposure over the settlement period leads to a reduction in margin requirements thus enabling market participants to better manage capital and liquidity risks. The Depository Trust and Clearing Corporation (DTCC) estimates that T+1 settlement could translate in a reduction of 41% of the volatility component of CCP margin requirements[2].

- Maintaining global competitiveness and alignment of European capital markets: reducing the settlement cycle to T+1 can help maintain the competitiveness and relevance of European capital market in a global context and attract investors via a more efficient use of capital supported by a more modern settlement chain (risk and cost reduction improves liquidity).

Lessons learned from the North American migration to T+1

Lessons learnt from the North American T+1 migration can be leveraged in the European context, namely due to similar challenges. Capabilities such as setting up appropriate governance structures, upgrading technology to increase automation and straight-through processing, reviewing processes to eliminate manual interventions can all be in theory re-applied to the European migration.

For instance, the North American migration highlighted the importance of:

- Public and private sector collaboration: can support the identification of common challenges, with a view to develop effective joint solutions that advance the strategic goal of a compressed settlement cycle.

- Clear regulatory and industry guidance: enable market participants and regulators to pinpoint the instruments in scope versus those out of scope, establish an overarching timeline and support the development of guidelines to smooth out any bumps (e.g., such as cut off times).

- Enhancing post trade capabilities: supports the adoption of automated post-trade solutions (e.g., real-time trade matching) and the drive for efficiencies in the allocation and affirmation process which enhance trade matching on or before T+1.

- Operating model adjustments: such as changes to trade matching and settlement processes, measures to address time zone and foreign exchange (FX) challenges and funding model adjustments have all played a key role in accounting for the increased funding requirements resulting fromT+1.

- Cross-border considerations: firms have had to incorporate a global perspective, such as FX settlement risk, international banking and market coordination, and collateral risk management to enable the successful implementation of T+1.

Leveraging partners who offer scale and efficient trade settlement capabilities, such as automated and round the clock FX or middle office outsourcing, has been a useful tool in successfully implementing T+1 settlement in North America since May 2024.

The European transition will present a unique set of challenges

The European securities settlement ecosystem differs from the US due to its complexity: multiple legal, fiscal and regulatory frameworks, languages and a larger number of stakeholders involved in the securities settlement chain (e.g., such as market infrastructure providers).

Due to this increased complexity, the European migration to T+1 presents a set of challenges:

- Fragmentation: European financial markets are characterized by multiple jurisdictions, regulatory bodies, CSDs and clearinghouses. For instance, not all 31 European CSDs have the same operating hours, some allow partial settlements while others do not, some CSDs are part of T2S and others not.

- Multi-currency: there is a diverse set of currencies within Europe as well as Central Banks adding a further layer of complexity to the European migration.

- Operational and regulatory hurdles: compressing post-trade activities into a single day can lead to increased operational complexities, especially for firms with systems not yet adapted to T+1, potentially exacerbating settlement failures. The increase in fails, during the adaptation period, could lead to a significant amount of financial penalties under the EU’s CSDR regime if no relief is provided.

- Cut-offs: early publication and notice of cut off time changes will be essential in ensuring that firms can work towards them. In the North America T+1 context, the publication of cut off times and changes were left until relatively close to the implementation deadline, allowing little time for the industry to work these into their systems developments and process implementation. Northern Trust will continue to utilise its voice in the industry to lobby and deliver cut off time changes as efficiently as possible on behalf of our clients, especially given so many more platforms will be changing cut offs than under the North American move. It is worth highlighting that in the EU T+1 Industry Committee in its “High Level roadmap”, published 30 June 2025, there are recommended placeholders for specific settlement cutoffs. Firms will need to monitor subsequent industry publications and recommendations to ensure they are able to align with industry cutoff standards under development.

- Funding: a shorter settlement cycle can give rise to funding and liquidity issues. Clients will need think about their whole trade lifecycle and any connected / dependant movements to understand if they are likely to encounter funding gaps. Thinking ahead of time how to solve those challenges will be key as well as assessing the impact of any penalties that may occur due to failed trades.

- Securities with Multiple Listings: some securities, such as Eurobonds and exchange traded funds (ETF), trade on numerous European trading exchanges, including the UK, Switzerland and some Nordic venues. These might also settle at an International Central Securities Depositary (ICSD) highlighting the importance of the alignment and coordination of European jurisdictions to achieve T+1.

- Funds: within the UK and EU already have a T+3 or shorter fund subscription and redemption settlement cycle. ESMA estimates that a large portion of UCITS transactions settle on T+2 and a non-negligible amount settle more than two business days after trade date. This means that the creation and redemption processes of shares of funds invested in jurisdictions not yet operating on T+1 represents a significant challenge. If a fund manager has to deliver on T+1 the share of a fund invested in securities which settle on T+2, the transaction on the fund share is likely to fail to settle. As such both the IA, PIMFA and AIMA issued a recommendation on 29 May 2025 to encourage firms to alter their fund settlement timings to T+2 on or before 11 October 2027.[3]

To support the transition to T+1, the “EU T+1 Industry Committee” published it’s High-Level Road Map on 30 June 2025[4]. The roadmap contains a series of recommendations designed to assist market participants in identifying and addressing critical operational considerations in readiness for firm’s planning, budgeting and implementation of securities settlement target operating model changes. The 60-page report contains over 59 recommendations split across key aspects of the securities settlement process. The EU T+1 Industry Committee recommends that several actions take place as soon as possible or latest by Q3 2025. This underscores how firms’ need to prioritise planning for EU T+1 as soon as practically possible.

Partnering with Northern Trust

Following the successful implementation of T+1 in North America, we look forward to leveraging our global presence and capabilities to support clients as they begin preparation for the European migration to T+1 on 11 October 2027.

It is important firms begin to prepare for this transition by:

- Establishing an internal enterprise-wide T+1 program and participating in relevant industry stakeholder groups, to increase education and information gathering, supporting the analysis and operating model design of the European T+1 migration (e.g., timelines, regulatory and industry guidelines, testing schedules etc).

- Engaging with counterparties and intermediaries to understand their preparedness, operating model analysis and how their systems, processes and needs may evolve due to enhancements (e.g., reviewing counterparties’ and intermediaries’ specific needs).

- Preparing an impact assessment of internal and external security settlement processes to identify and plan for enhancements across the trade lifecycle where required (e.g., settlement root cause analysis, removal of manual intervention, automation, efficient use of UTI etc) such as reviewing trading systems, trade support and confirmations.

- Identifying ancillary services such as funding, financing and securities lending to ensure there is an accurate understanding of the impact of T+1 on liquidity and costs such as reviewing trade funding and payment systems, ETFs and fund redemptions and any alterations to the recall process for securities lending.

Although we are not starting from scratch this time round, expect team sizes and funding to be more significant than it was for the North American change due to the increased complexity. From a scheduling perspective, this also means that planning and analysis needs to start sooner in order to meet the deadlines. In order to support you, we will have a series of T+1 communications in the lead up to go live and encourage you to begin your preparations. Northern Trust looks forward to partnering with our clients on this change and welcomes your feedback and early discourse.

[1] Firebrand Research - Tackling Post-Trade Friction Supporting a Global Shortened Settlement Cycle (June 2025)

[2] DTCC - Leading the Industry to Accelerated Settlement (April 2021)

[3] https://www.theia.org/news/press-releases/ia-pimfa-and-aima-issue-recommendation-t2-fund-settlement

[4] https://www.esma.europa.eu/sites/default/files/2025-06/High-level_Roadmap_to_T_1_Securities_Settlement_in_the_EU.pdf

Meet The Experts

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Natalie Berkecz

Global Head of Regulatory Product

IMPORTANT INFORMATION AND DISCLOSURES

Northern Trust Banking & Markets is comprised of a number of Northern Trust entities that provide trading and execution services on behalf of institutional clients, including foreign exchange, institutional brokerage, securities finance and transition management services. Foreign exchange, securities finance and transition management services are provided by The Northern Trust Company (TNTC) globally, and Northern Trust Global Services SE (NTGS SE) in the European Economic Area (EEA). Institutional Brokerage services including ITS are provided by NTGS SE in the EEA, Northern Trust Securities LLP (NTS LLP) in the rest of EMEA, Northern Trust Securities Australia Pty Ltd (NTSA) in APAC and Northern Trust Securities, Inc. (NTSI) in the United States. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures.

This marketing communication is issued and approved for distribution in the United Kingdom by The Northern Trust Company, London Branch (TNTC). TNTC is authorised and regulated by the Federal Reserve Board; authorised by the Prudential Regulation Authority; subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. This communication is provided for the sole benefit of clients and prospective clients of TNTC and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of TNTC. Any unauthorised use is strictly prohibited. This communication is directed to clients and prospective clients that are categorised as eligible counterparties or professional clients within the meaning of Directive 2014/65/EU on markets in financial instruments (‘MiFID II’). TNTC does not provide investment services to retail clients. This communication is a marketing communication prepared by a member of the TNTC sales & trading departments and is not investment research. The content of this communication has not been prepared by a financial analyst or similar; it has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. This communication is not an offer to engage in transactions in specific financial instruments; does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of individual investors.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.