- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Simmering Down

Growth is expected to decelerate, but not come crashing down.

The temperature around global trade has generally eased since early April, when the U.S. administration rolled back some of its sweeping tariffs. Negotiations are ongoing, with progress achieved on a couple of fronts. Economic activity has emerged unscathed in most places, and some cautious optimism surrounds the outlook.

But international commerce is unlikely to see a return to old norms. Trade pacts are unlikely to result in significant tariff reduction. Sectoral and universal levies, along with non-tariff barriers, remain key impediments. U.S. duties on steel and aluminum imports have been doubled to 50% for some nations. Further, geopolitical tensions could complicate an already intricate economic backdrop.

Growth is expected to decelerate across major markets during the balance of the year, but it is unlikely to come crashing down. As long as the worst of trade tensions are behind us, the global economy can continue to grow through uncertainty.

Following are our thoughts on how top markets are faring.

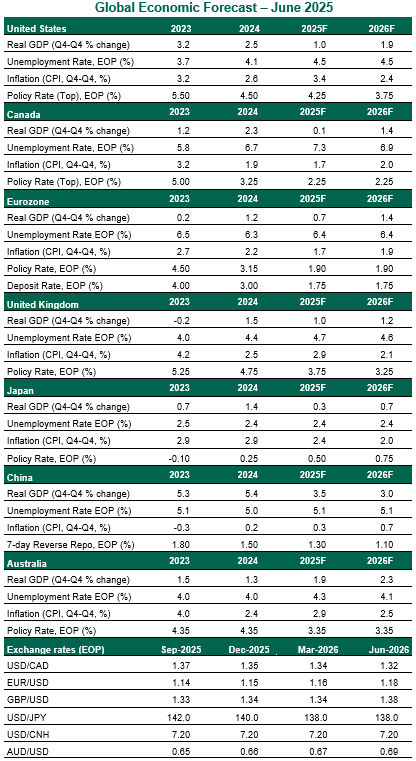

United States

- Gross domestic product (GDP) in the first quarter was heavily influenced by front-loaded imports ahead of tariff announcements. These flows have stopped, and trade will be less of a damper on second quarter growth. Consumer and business spending has remained solid, and we expect it to continue rising at a moderate pace. There is a growing belief that the U.S. administration will not push the trade war to recessionary extremes. However, the costs and uncertainties of new tariffs will make for slower growth and higher prices in the second half of the year.

- With inflation above target and the labor market still performing reasonably well, the Federal Reserve is staying on the sidelines. Tariffs have added to inflation risk, even as some policymakers have characterized them as a one-time shock. We anticipate one rate cut this year, followed by two in 2026.

Canada

- Canada’s economy has maintained a steady pace of growth, expanding 0.5% during the first quarter of this year. But the picture wasn’t as rosy as the headline reading suggested. Consumer spending growth slowed sharply, despite temporary fiscal stimulus measures like the Goods & Services Tax holiday. Residential investment contracted. Front-loaded exports to the U.S. were the key drivers of growth. We continue to expect a short and shallow technical recession this year.

- Uncertainty around U.S. trade policy and the potential upside risks to inflation from retaliation have forced the Bank of Canada (BoC) to adopt a wait-and-see stance. The BoC held its policy rate steady for the second meeting in a row; rates are at the middle of their 2.25%-3.25% neutral range. The Bank’s preferred inflation measures have remained firm, contributing to caution. The Governing Council, however, suggested that rate cuts may be needed if cost pressures remain contained and the economy weakens. We continue to see two more cuts later this year.

Eurozone

- The eurozone economy expanded at a robust 0.6% quarter over quarter rate in the first three months of the year. Though strong on the surface, the headline print was heavily influenced by volatile Irish GDP figures, which accounted for a little over half of the aggregate growth. Prospects are expected to weaken and stay soft in the coming quarters. Higher tariffs coupled with elevated trade policy uncertainty will weigh on consumption and investment decisions. Euro area labor markets continue to hold up, with the unemployment rate stable at a record-low of 6.2% in April. A durable trade deal with the U.S. remains elusive, with persistent disagreements over tariffs and non-tariff barriers.

- The news on prices has been getting better. Headline inflation dropped below the target to 1.9% year over year in May. Services inflation eased notably, after a shift in Easter timing had pushed it up in April. Some wage indicators are pointing toward a slowdown in the coming months to levels compatible with the 2% inflation target. Continued progress on disinflation allowed the European Central Bank to make policy less restrictive at the last meeting. But the messaging suggested that the central bank was nearing its terminal rate. We expect one more cut in the third quarter.

United Kingdom

- The U.K. economy appeared to turn a corner in the first quarter, with growth exceeding expectations. However, signs of a payback have started to emerge. GDP growth declined 0.3% in the month of April, and retail sales slumped in May. The composite Purchasing Managers’ Index was broadly flat for the three months ending in June. Britain has moved aggressively to strike trade deals with three major markets, but none are likely to be game changers for the domestic economy. Fiscal room has tightened; unfavorable revisions to the outlook by the Office for Budget Responsibility will likely force the government to hike taxes in the Autumn Budget.

- Inflation moderated in May. While headline inflation is likely to rise gradually over the coming months on account of positive energy contributions, we expect continued progress on underlying price pressures. Slack in the labor market will exert further downward pressure on wages, giving the Bank of England confidence to stick to its quarterly pace of rate cuts.

Japan

- Growth was revised up from an initially reported -0.7% annualized quarter over quarter contraction to a smaller -0.2% decline in the first quarter. The upgrade was primarily driven by a sharp revision to inventory investment alongside a better private consumption reading. Household demand should continue to grow, backed by improving real incomes. But higher U.S. tariffs and elevated uncertainty will prove to be a lasting drag on exports and business investments. Hopes of a trade deal with the United States have risen ahead of the July 9 deadline but may fall short of providing a reprieve to the country’s vital auto sector. The U.S. has been reluctant to offer concessions on this front.

- Inflationary pressures have strengthened, but not owing to demand-side pressures. The core-core consumer price index (excluding fresh food and energy) remained above 3% year over year in May, led by surging rice prices. By contrast, services inflation was tame at 1.4%. The Bank of Japan (BoJ) remains on the sidelines, given the high level of uncertainty. However, the central bank announced its exit plan from quantitative easing, starting in FY2026.

China

- Economic activity in China has remained resilient in the first half of the year, benefiting from front-loaded exports and consumer goods trade-in programs. Neither of these two supports are likely to sustain growth for very long. The country’s important real estate sector remains in an extended slump. Elevated trade tensions coupled with relatively higher tariffs on Chinese goods will hinder external demand. The de-escalation in trade tensions from a point of a virtual trade embargo was a welcome development, but a more durable accord that further reduces frictions is nowhere in sight. Even under a best-case scenario, levies on Chinese imports into the U.S. will be much higher than they were at the start of the year.

- The urgency to double down on macro easing waned after the tariff truce, but fiscal and monetary policies are likely stay loose. Further rate reductions and liquidity-boosting measures will be needed to keep deflationary pressures at bay. Incremental easing, rather than more sweeping stimulus measures, remains our base case.

Australia

- Australian real GDP growth slowed to a crawl in the first three months of the year, rising just 0.2% quarter over quarter. Consumers and businesses remained cautious amid sluggish real wages and high global uncertainty. Lower borrowing costs alongside improving purchasing power should aid in a revival of economic activity. Australia has managed to fly under the Trump administration’s radar on trade. But as an open economy with deep links to China, Australia is vulnerable to a slowdown in external demand.

- In line with expectations, the Reserve Bank of Australia resumed its easing cycle as it lowered the cash rate by 25 basis points to 3.85%. The minutes of the meeting revealed that the Board considered a larger 50 basis points reduction, owing to downside risks to both the global and domestic outlook. While the statement did not provide explicit guidance for further easing, the central bank’s tone appears to have become more accommodative. We continue to see two more sequential cuts.

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.