- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Student Debt Default Deluge

Student loans are rapidly rising to their pre-pandemic delinquency rates.

By Ryan Boyle

Debt collectors have been unpopular since ancient times, but they play a necessary role in the lending lifecycle. Their jobs are not easy: I recall one collector noting that there are few ways to communicate with defaulted borrowers. Mail is easy to discard; phone calls are regulated and often ignored; in-person tracking is expensive. But a derogatory entry on a consumer credit file can send an effective message.

Student loan borrowers are once again learning lessons about the consequences of debt delinquency. After a prolonged and controversial delay, student loan payments are coming due again, and collection efforts are underway.

The hiatus from student loan repayments was borne of good intentions. Amid vast uncertainty in the COVID-19 pandemic, the federal government made rapid, bipartisan efforts to ease the burden on households wherever possible. Most student debt is held by the Department of Education, and payments were suspended starting in March 2020.

After five years, student debt is once again due.

After legal wrangling and failed ideas to provide broader relief, payments were once again required starting in October 2023. Borrowers whose bills had stopped were facing what felt like a new obligation, which was disconcerting. To ease the transition, the government did not enforce collections for a year. But the grace period has expired, and the scope of defaults is significant. Many household budgets did not have the slack to resume payments.

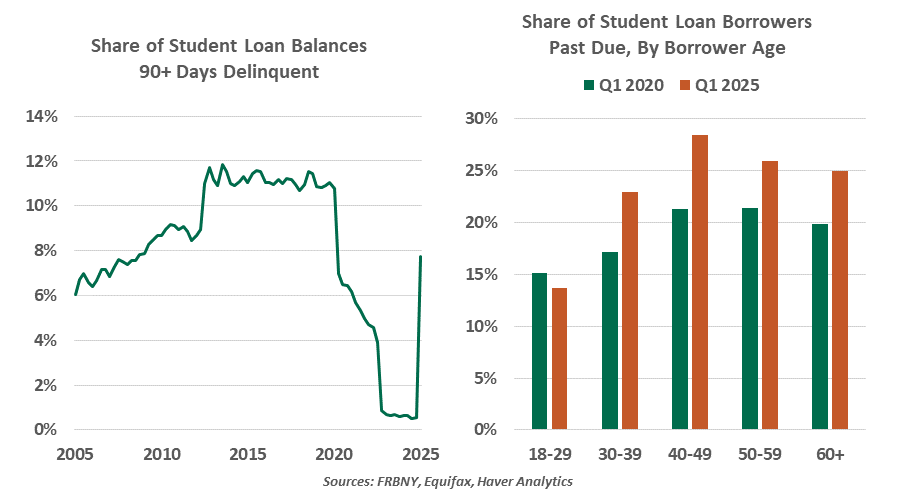

Credit bureau data summarized by the Federal Reserve Bank of New York show that roughly one out of every four of the 19 million borrowers with payments due fell behind on their student loans in the first quarter. Defaults are rapidly rising to their pre-pandemic rates. Researchers observed that credit scores declined by over 100 points for more than two million borrowers. A below-prime credit score will raise borrowing costs and likely preclude homeownership for these consumers; landlords may hesitate to sign leases based on their history of delinquency.

Unlike other forms of credit that may be written off or expunged in bankruptcy, student debt will stay with a borrower until it is repaid. The New York Fed found that borrowers of all ages were impacted by past-due marks on their student debt, with a greater delinquency rate observed in borrowers over 40.

During times of financial distress, skipping a student loan payment is tempting. Essential spending like rent, utilities, communications and transportation will take priority. But defaulting on a government-held obligation carries stringent consequences. This summer, the administration will resume wage garnishment to collect on student loans, the same punitive mechanism used to enforce legal judgments, tax underpayments and past-due child support. Up to 15% of after-tax income can be redirected to enforce student loan repayment.

As loans came due in late 2023, we wondered whether the renewed payments would impair the unstoppable consumer spending that fueled U.S. economic outperformance. Continued consumption gains in 2024 showed these fears were overstated or premature. An actual loss of disposable income will prevent some consumers from spending as they have done to date.

For most students, borrowing for education will pay for itself through higher lifetime earnings. But the structure of student lending is in need of reform. The tax legislation working its way through Congress may include some simplifying provisions, but appetite for broader reform is limited.

A successful debt collector cannot be shy. Timid efforts to obtain payment will rarely be rewarded. The federal government has changed to a more aggressive posture for student loan collections. Borrowers in default will hear the message loud and clear.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.