- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Great Unwind

U.S. trade strategy is a top worry among economists.

By Carl Tannenbaum

Editor’s Note: I hosted a gathering of Chief Economists from around the world in Ireland last month. Following is an abridged version of the meeting summary that I offered during the closing session.

You don’t have to walk far in Dublin before encountering Celtic knots, the intricate designs that can be found on the Book of Kells, the lawn at Dublin Castle, all manner of Irish jewelry and the upper arms of young Irish. The patterns appeared in Ireland in the seventh century, and eventually became emblematic of the Celtic cultures that spread through that part of the world.

The unbroken cords that form these patterns are symbolic of interconnectedness. It wouldn’t be too much of a stretch to suggest that the knots also describe the path taken by the Irish economy over the past 50 years. Once a somewhat isolated market, Ireland has become a “Celtic Tiger” that has global connections of considerable width and depth.

That symbol, and that history, made Ireland a fitting place to consider what happens when the knots that bind countries together begin to fray. If I had to offer a theme that best captured the content of this year’s conversations, it would be “The Great Unwind.”

I drew the following take-aways from the discussions:

- The United States is the only major market where consumption is growing at a reasonable rate. Nations following an export-led model are therefore highly reliant on U.S. demand, which makes tariffs a particularly potent threat.

- Free trade naturally breeds dependence, as countries focus on their comparative advantages and recognize their resource limitations. Unwinding globalization will be difficult, and it will inevitably reverse gains in standards of living. Middle income countries are most at risk.

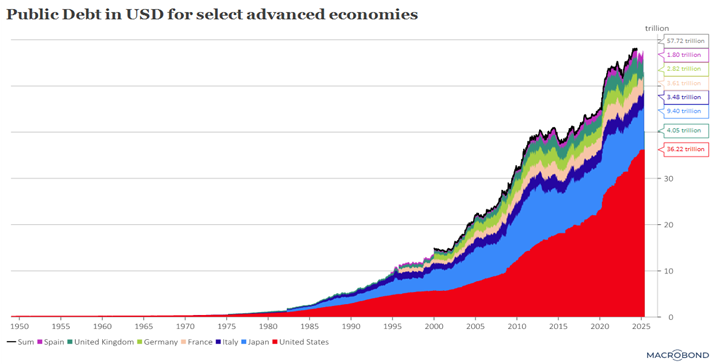

- Anxiety over the level of sovereign debt in developed markets has moderated. The necessity of public spending on security and investor appetite for new safe havens are leading countries to view new bond issuance more favorably.

- The penetration of artificial intelligence (AI) is proceeding more rapidly than expected. This will aid productivity, but accelerate concerns about job displacement that could have economic and political consequences.

Following is background behind each of these conclusions.

Demand Dependence

As several of our presenters noted, backlash against globalization is not new. It has roots in the 2008 financial crisis, and it intensified during the pandemic. But efforts to dissolve the international order have accelerated during the first six months of the second Trump Administration. U.S. policy in the areas of trade, immigration and security has changed, creating an extended cascade of consequences.

The Trump Administration has rooted its tariff strategy in the belief that exporters are deeply reliant on U.S. demand. Americans have often been criticized for spending beyond their means, and not without justification. But global growth would be far more modest if U.S. households tightened their belts.

To leverage this dependence, the U.S. has revealed itself willing to break with existing trade agreements and protocols. Existing pacts with Canada, Mexico, Japan and South Korea have been rendered inoperative. This raises questions about the durability of any accords reached with the current Administration.

The consensus among the group was that the trade agreement covering North America is likely to survive in some form, but a complete decoupling among its signatories cannot be ruled out.

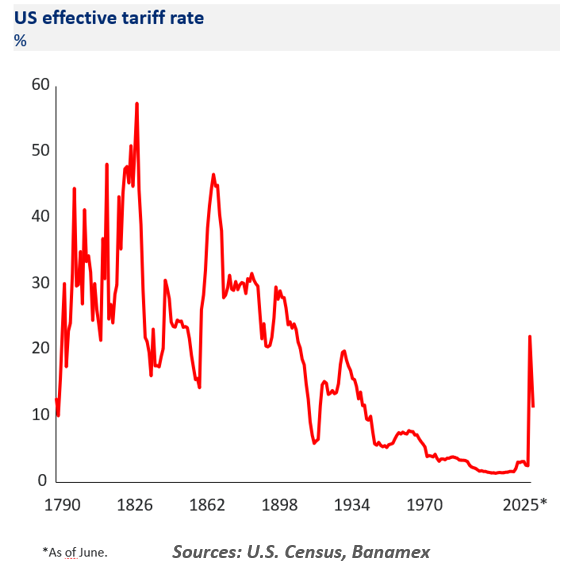

Our delegates expressed surprise that more markets haven’t retaliated against U.S. tariffs. Canada stands virtually alone in this regard, and its countermeasures have not had much impact. Only a coordinated response across markets has the potential to push tariff rates below the U.S. minimum of 10%. For now, U.S. trade partners seem to prefer settling to battling.

China and Southeast Asian economies are a particular target of U.S. trade policy. China’s craft in managing the geography of production and shipping has placed adjacent markets like Vietnam in the cross-hairs. The current focus on transshipment within U.S. tariff policy reflects a wish to diminish “white labeling.”

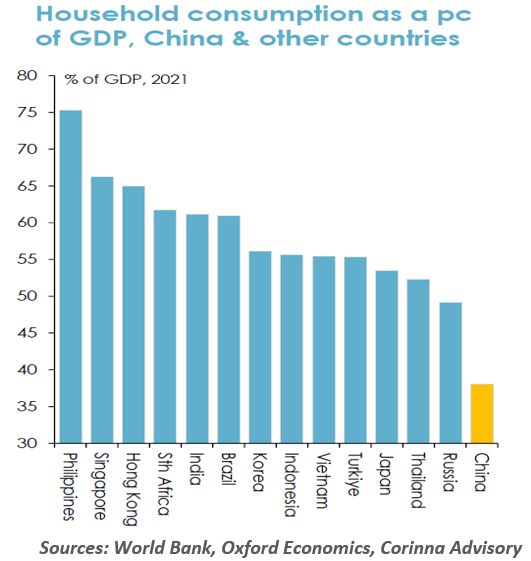

Domestic consumption in China remains sluggish; there are secular and cyclical reasons for that, but neither is likely to ease anytime soon. That leaves China heavily dependent on exports, which it continues to promote with supply-side stimulus measures. This only angers Washington further.

China is less reliant on U.S. demand than other countries are. It may therefore take a long while for the two sides to reach a durable accord.

A reduced level of global commerce will create new challenges for emerging markets. Middle classes have grown in many of these nations, which both reflects and supports economic progress. A substantial middle class is also associated with institutions that promote broad-based welfare, and governments which are less populist.

Many countries that achieve middle-income status never move beyond that stage. With trade in retreat and technology ascending, nations that have reached that point may struggle to maintain it. And in the process, they may become more politically unstable.

Seeking Strategic Autonomy

It is hard to know where tariffs will end up, or what the impacts on economic activity will be. There are likely to be significant discontinuities, and equilibria may prove to be more fleeting than lasting. The uncertainty surrounding all sorts of economic policy is high, and this can inhibit growth by paralyzing decision-making.

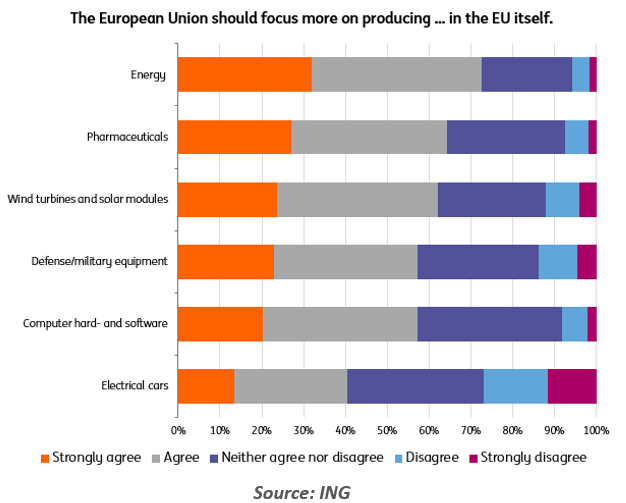

As global relationships become less reliable, countries and regions are seeking a greater degree of strategic autonomy. Europe is attempting to become more self-sufficient in the areas of commerce, security, sourcing and energy. Germany is taking the lead: fiscal expansion there will not only serve European goals, but could potentially rouse Germany from a prolonged economic slump. The commitment among North Atlantic Treaty Organization partners to increase annual security spending to 5% of gross domestic product (GDP) will also be a factor.

The challenges to achieving true self-sufficiency are substantial. An energy transition will deepen dependence on China, and greater responsibility for security will deepen reliance on the United States. Efforts to become more autonomous may be a matter of trading one form of reliance for another. My peers raised a difficult question: what is the cost of autonomy, and is it worth paying?

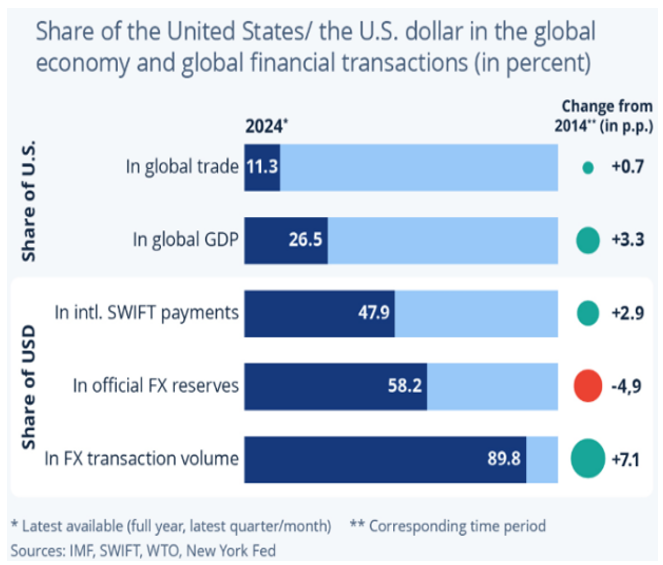

In the financial arena, we had a discussion of whether this was a moment of opportunity for the euro. The breaking of trade ties, deepening U.S. debt and questions about American exceptionalism have raised doubts about the U.S. dollar, which has not been trading like a safe haven currency lately.

Another source of concern surrounding the U.S. currency is the series of attacks on the Federal Reserve, which is under pressure from the White House to lower rates. Full employment and inflation risk in the U.S. will likely lead the Fed to remain cautious…which will likely sustain the ire of the President. Stoic resolve in the face of sharp abuse from the White House earned Fed Chairman Jerome Powell a loud ovation at the June European Central Bank summit in Sintra; he received similar plaudits from our membership.

To truly rival the dollar, the euro would need the following supports:

— Stronger economic growth, today and in the long term

— Unified financial regulation and infrastructure

— Common tax regimes across countries

— A sound banking system

— A bond market better able to receive inbound capital

It will take time for the euro area to check all of these boxes.

Debt Relief

As investors seek alternatives to U.S. Treasury bonds as safe havens, some regions are moving to meet that demand with additional issuance. The proceeds from incremental debt could be used to support the public investment needed to adapt to the changing global environment.

The tacit blessing of fiscal expansion is a departure from the condemnation of borrowing that has been expressed in recent years. In Europe’s case, annual deficit limits will likely remain, but the cap on debt as a percentage of GDP called for in the Growth and Stability Pact may never be formally re-set.

On the private side of finance, the absence of securitization markets and the narrow breadth of private credit in Europe may be hindering capital from reaching its most productive and profitable destinations.

Ideally, policy surrounding finance should facilitate credit flows and innovation, while minimizing the potential for instability. It is hard to strike a balance between these aims, but Ireland offers a model to follow. The rise of the Irish financial sector has been supported by a constructive regulatory environment, investments in human and technological capital and favorable tax terms.

Vehicles that allow investors to meet opportunities without going through intermediaries can serve to widen channels of capital, providing financing to promising sectors that are in their early stages. This will be key to Europe’s goal of becoming more innovative.

Utopia Or Dystopia?

We closed our conference with an update on AI, which may be transitioning rapidly from augmenting labor to substituting for it. Evidence suggests that AI is already affecting hiring rates, as investment in the technology continues unabated. While this will have benefits to productivity, it raises questions about the quantity and nature of work that will be available for humans to do.

One of our guests suggested that college degrees will lose value quickly, and that a 15-hour workweek may be in our future. Those predictions may prove to be extreme, but the pace and direction of travel surrounding AI will raise difficult questions for economies and societies.

Fortunately, the group had the opportunity to unwind in more pleasant ways on a few occasions during the week. The walk home from dinner on Tuesday astride the River Liffey was memorable, and the view down on Lough Tay and the Guinness Estate was epic. We learned what good craic is, and how to say a cúpla focal in Gaelic.

The Great Unwind is a huge frustration for our group, with its international sensibilities and its appreciation of inconvenient economic truths. We will certainly try, wherever and whenever we can, to limit the unraveling that is currently underway.

But it may be a long while before we can think about restoring the ties that have bound us. The group of us resolved to provide intellectual and psychological support to help those around us make the best of a bad situation.

It was wonderful to be together in Dublin. Until we meet next year, I expressed the wish for the group that the wind will always be at our backs, that the sun will shine warm upon our faces and that the road will rise up to meet us.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.