- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

US Economic Outlook | May 14, 2026

Climbing with Caution

Domestic momentum continues despite uncertainty abroad.

The United States has not felt the greatest costs of the Iran conflict, but challenges are becoming visible. Energy prices have risen, with limited prospects for relief. Inflation measures are poised to spread to other product and service categories. Inventories that helped to blunt the impact are depleting; supply chain distortions are accumulating.

Our forecasts have been premised on a de-escalation and progress toward a durable truce in the Middle East. The U.S.-Iran ceasefire has mostly held, but the slow pace of negotiations is discouraging. The longer the situation lingers, the more downside risks accrue.

The surge in energy prices is reflected in our inflation forecast. Our base case is for the economy to grow through this interval, thanks to continuing tailwinds from AI-related investment and wealth effects. Risks run in both directions; a conflict resolution amid healthy business investment could lead to another strong year.

Following are our thoughts on the outlook for the domestic economy.

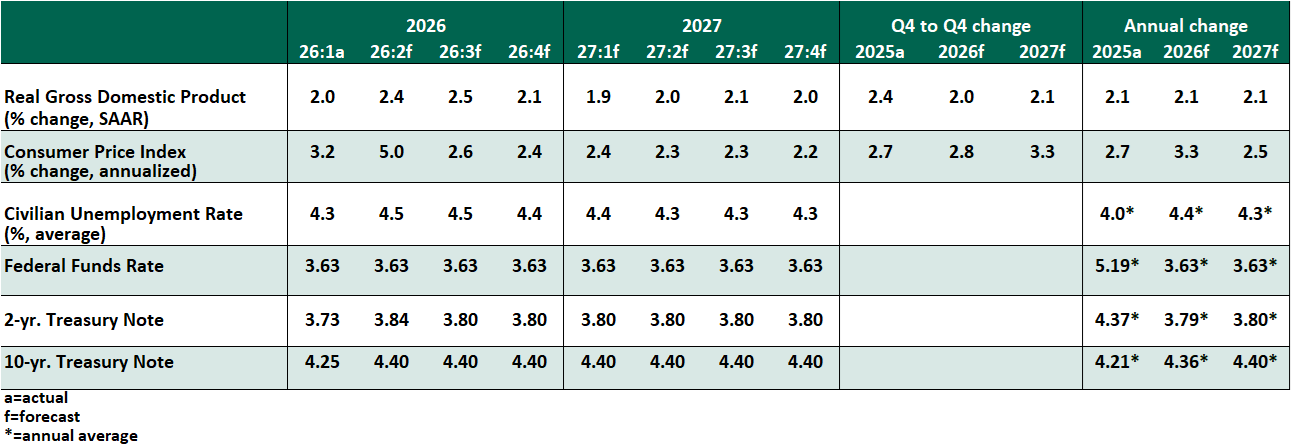

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The U.S. labor market has adjusted to a steadier state. April job growth of 116,000 was well dispersed across the private sector, and the unemployment rate held steady at 4.3%. Private employment data sources like ADP show a similar trend. Weekly initial unemployment claims remain low. Labor turnover data through March showed a slight improvement in the rate of hiring. The Iran conflict has not put employment at immediate risk.

- Real gross domestic product (GDP) grew 2.0% at an annualized rate in the first quarter. The gain was led by business investment in equipment and intellectual property, both consistent with eager spending on artificial intelligence deployments. Consumer spending growth moderated slightly to 1.5% but still continued a five-year streak of growth.

- The consumer price index (CPI) for April climbed to a gain of 3.8% over the past year, or 2.8% on a core basis (excluding food and energy). Energy inflation was predictably high, and food prices are rising, especially for meat. The measure of shelter costs was pushed up as lingering statistical effects of last year’s government shutdown were remediated. But reheating was also evident in unexpected categories like apparel and technology, potentially a delayed outcome of tariff price adjustments.

- The April inflation measure exceeds the gain in average hourly earnings of 3.6%. For the first time in three years, households are not keeping up with inflation in aggregate, depressing sentiment. If sustained, this imbalance may weigh on consumption. For now, consumers have grown their spending in part by reaching into their savings; the rate of personal saving reached a three-year low of 3.6% of disposable income in March.

- The Federal Reserve targets a 2% annual gain on the deflator on personal consumption expenditures (PCE). This measurement is published with a lag to CPI, and differences in weights have recently kept PCE higher than CPI. As of March, PCE gained 3.8% overall and 3.2% core, with little prospect for relief in the near term.

- In their April 29 meeting, the Federal Open Market Committee left interest rates unchanged. The most noteworthy aspect of the decision was three voting members formally dissenting against the language in the committee’s statement that suggested any future easing. Subsequent inflation data supports the dissent: absent a crisis, rate cuts are not justifiable under current inflationary conditions. We have removed the forecasted rate reduction that we had placed in the fourth quarter of this year.

- Incoming Chair Kevin Warsh will inherit a group with strong and dispersed opinions, and a new willingness to show their independence.

- Geopolitical uncertainty has not weighed on equity markets. However, oil prices have entered a new range reflecting limited capacity, and bonds have repriced to reflect a higher inflation outlook. A further breakout in either energy prices or bond yields are central risks to the outlook.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.