- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | March 13, 2026

More On The Middle East

The whole world will feel the consequences of this conflict.

By Carl Tannenbaum

The war in Iran is approaching the two-week mark. What started as a focused set of sorties has broadened into something more durable and dangerous. Iran is not Venezuela.

It has been a volatile interval on the ground in the Middle East, and in the financial markets. Here is some background on how we are thinking about the economic consequences of the hostilities.

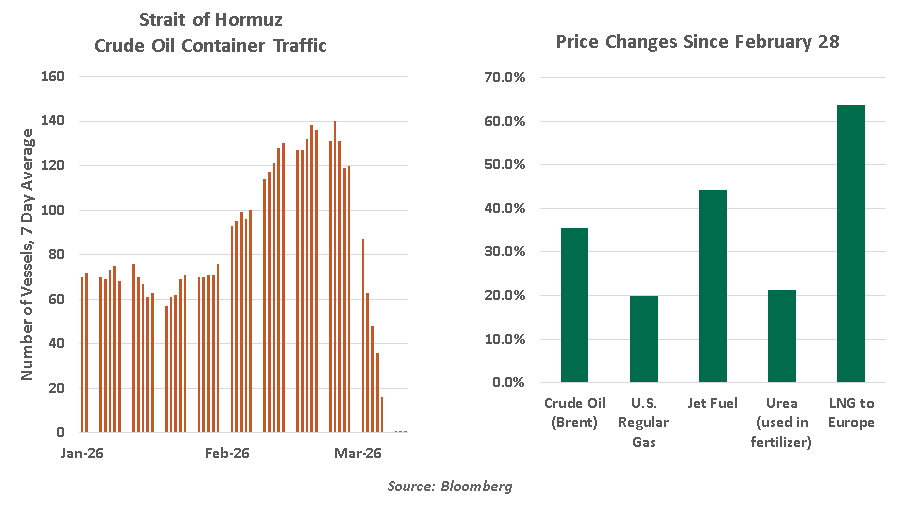

- We are experiencing a significant energy shock. The Strait of Hormuz, a narrow artery through which a substantial fraction of the world’s oil passes, is essentially closed. Iran is able to imperil transit effectively with inexpensive mines and drones, discouraging passage and raising maritime insurance rates. It will be difficult, if not impossible, to neutralize this threat through aerial attacks alone. Using naval escorts to clear a path may not be that effective, and raises the risk of military casualties.

Alternative channels like pipelines cannot handle the same level of output, and cannot move commodities other than oil. With storage capacity stretched, crude production has slowed; oil producing countries in the Middle East are seeing reduced export revenues. Once stopped, restarting production will take time.

- Oil prices have risen significantly, and they have been extremely volatile. The downstream impacts of this on fuel costs for consumers, factories and transportation around the world are already being felt. Derivatives from oil refining are used in a range of products, including fertilizer. Diminished energy and aluminum supplies may impair factories in a number of countries, extending the disruption to a wide range of products. Shipping costs are up sharply. The inflation that will ensue could be broader and deeper than anticipated.

- Damage to critical infrastructure in the region has been limited, but could easily expand. If a key production facility or energy terminal is attacked, energy prices could ascend sharply. This is among the many non-linearities surrounding the situation.

- To compensate for dwindling imports, several nations have announced releases from strategic petroleum reserves, but using stocks to offset flows is a temporary solution at best. Some countries, like India, have very modest reserves, which will not provide much of a buffer.

- Other nations are starting to limit exports, extending distortions in the market. Rationing is also being employed in some places. Government support for energy consumers or temporary reductions in fuel taxes will add to fiscal deficits, and may place pressure on bond or currency markets in the countries that apply them.

- The impairment of the energy supply chain is not as substantial as the broad shock produced by the pandemic. But the 2020 experience illustrates how consequences can radiate from an epicenter.

- While the world is much less petroleum-dependent than it once was, we’re being reminded that no other commodity is as central to economic activity…and daily life.

Hopes for a quick resolution are unrealistic.

- Reaching a true conclusion to the conflict may take months, not weeks. The longer it goes on, the greater the economic costs.

- There are certainly factors which may serve to limit the fighting. Iran has targeted civilian infrastructure in a range of Gulf countries, hoping that they will pressure the United States and Israel to back down. The war is unpopular and will add to inflation in the United States, creating political costs for the administration. Supplies of materiel are limited, and may govern the intensity of attacks. Support from European allies has been tepid, at best; their tacit acceptance of what is going on may have its limits.

- On the other side, the naming of Iran’s new spiritual leader, the son of the man killed in the initial attack on Iran, appears to be an act of defiance. Negotiations aimed at finding an “off ramp” are a long way off. The conflict has multiple fronts, and involves a range of parties; engineering a durable truce amongst them will not be easy. The objectives of the United States and Israel are aggressive; fully suppressing the threat that Iran poses to the region will take time and the investment of ground troops, and success is not assured.

- Iran has been involved in a long series of conflicts in recent decades. A reading of the history suggests that surrender is not in their nature. We’ve yet to see terrorist or cyber attacks on Western targets; the possibility of that kind of escalation is present.

- Declarations of victory have already been offered by both sides. But on the ground, it appears likely that the fighting, and the risks associated with it, will remain severe for some time.

The conflict will depress economic growth and lift inflation.

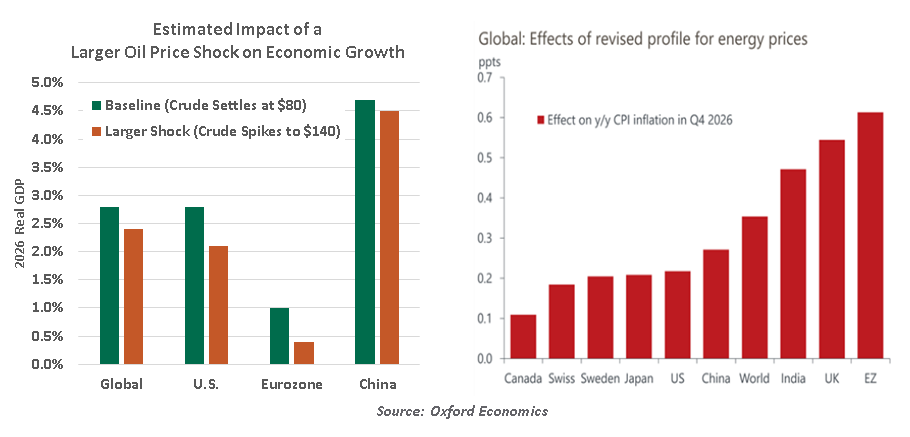

- The economic consequences of the war will be considerably greater for Europe and Asia than they will for the United States. Energy costs take up a much larger share of household budgets in non-US markets, with many nations reliant on imported liquified natural gas. The challenges will be especially complicated for India and emerging economies in Asia.

Oil shocks typically depress economic growth by acting as a tax on consumers and businesses, limiting their purchasing power. This tends to reduce inflation, but the force of higher prices for energy and other products is expected to be more significant.

Higher inflation rates across the world will change the trajectory of central bank policy. Futures markets have pushed out their expectations of rate cuts from the Federal Reserve, and are now expecting rate increases from the Bank of England and the European Central Bank later this year.

China is also in focus. Last year, Iran and Venezuela supplied about 15% of China’s crude oil. About a quarter of China’s imports of liquified natural gas come from the Middle East. For an industrial economy of China’s scale, any interruptions in energy supplies could be very damaging to growth.

The United States and China are scheduled to begin a high-level summit at the end of the month. Some think that this vulnerability will provide the U.S. some additional leverage in those discussions, which are to focus on trade terms. My partner Vaibhav Tandon offers more extensive thoughts on the impacts to China in a separate article.

The situation remains very fluid. We’ll endeavor to keep you apprised as events unfold.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.