- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Has Geopolitical Risk Lost Its Bite?

Understanding Market Reaction to the Iran and Israel Conflict

Despite significant worry about recent conflict with Iran in the Middle East, financial markets have had a muted response. Even as events drew in the United States, investors remained sanguine in their outlook. There’s been no widespread selling of equities. Gold, a perceived safe haven, did not rally and remained below highs attained earlier this year. Even oil only rose modestly in price, failing to achieve price levels of one year prior. Why?

Investors are worried about two primary risks from the recent flare up in hostilities with Iran:

The risk of higher oil and energy prices – one high probability risk is that oil infrastructure is destroyed or that oil tanker travel through the Straight of Hormuz is restricted. Higher oil prices, of course, will drive transportation and energy costs higher, dampening economic growth as a result.

AND/OR

The risk of the conflict expanding into other countries or regions – with the US joining attacks on Iranian nuclear infrastructure, a very real chance exists that the conflict could swell, embroiling additional participants. Here again, investors expect growth headwinds if hostilities expand or other countries join the attacks.

Yet despite real concern over these risks, financial markets barely moved. Price action in global equity, bond, and commodity markets did not reflect a high probability of the above risks manifesting. To understand the market’s reaction, or lack thereof, let’s break down these risks to understand why the market has generally shrugged them off.

Oil price stability

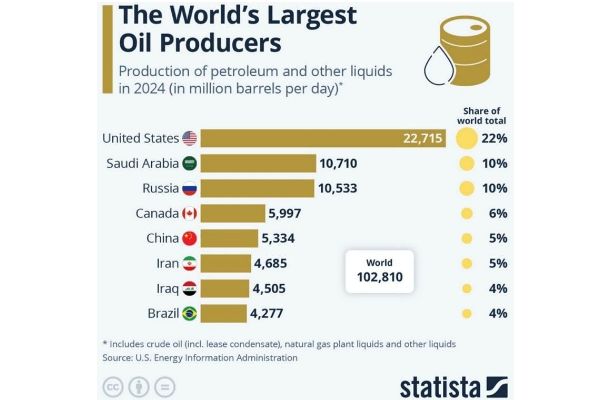

This risk of higher oil prices in the long run is low. Oil is oversupplied at present. The impact of the US shale revolution is profound. According to the Energy Information Administration (EIA), onshore crude oil production in the US has more than tripled since 2010, led in large part by the development of fracking technology to access oil trapped in shale formations. Today the United States accounts for 22% of total oil production, more than the combined total of what Saudi Arabia, Iran, Iraq and Kuwait produce. The US is now the dominant hydrocarbon superpower, a role that the country assumed in just the past 15 years. The importance of the Middle East within energy markets has therefore been diminished in recent years.

If oil prices did rise marginally, many investors believe that the effect would be temporary. More wells would be drilled/tapped to take advantage of rising prices. There are many different regions that could turn up oil production, beginning with the US. Continuing oil field development in countries such as Guyana and Kazakhstan will also expand global oil production.

And yet, many investors did not fret over even temporarily higher oil prices. Israel and Iran possess a number of vulnerabilities that render widescale targeting of oil and energy assets a less viable military strategy than what’s been observed in the Ukraine/Russia conflict for example. Both countries have very precarious infrastructure that could be targeted easily with devastating effects. Attacking one another’s infrastructure is therefore fraught with risk, with the real potential for a tit-for-tat response that would impact civilian populations and undermine political support. For this reason, civilian and energy infrastructure has typically not been targeted by either combatant.

Israel’s vulnerabilities come from its small size and lack of natural resources. It is a tiny country geographically with population centers clustered in the north/center area with deserts covering the southern 2/3rds. There are simply less areas to spread out sensitive infrastructure. And Israel’s energy sector is especially exposed. Since its founding, Israel has been a major importer of energy, making it very susceptible to any disruption . And even more worrisome, Israel attains over half of its water supply through energy-intensive desalinization plants. Therefore any attacks on power and electricity infrastructure has the double whammy of potentially cutting water supplies on top of disruptions to energy supply.

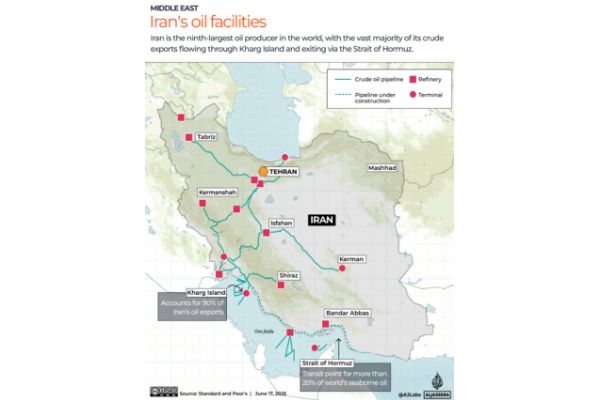

Iran is similarly exposed to attacks on their infrastructure. With decades of sanctions, Iran’s infrastructure is already in various states of disrepair, but particularly worrisome is that their oil export infrastructure sits on Kharg Island in the Persian Gulf. Approximately 90% of Iran’s oil exports flow through terminals on Kharg Island, rendering it an invaluable asset.[1] Defending the island is nearly impossible for Iran, as it is sits over 15 miles off the coast of Iran and only possess 8 square miles of land. The oil export facilities represent an easy target if either Israel or the US are so inclined. An attack on Kharg’s assets would indeed drive oil prices markedly higher (until additional supply comes available) but it would likely incite a similar reaction by Iran to counterstrike similar sensitive infrastructure.

Therefore the market consensus is that Iran will not focus on infrastructure in their missile attacks as Israel would easily and quickly return the favor. And likewise the consensus view is that Israel will also demonstrate calculated restraint to limit the likelihood of counterstrikes on their vulnerable and critical infrastructure.

Limited Scale Conflict

The second risk that would trigger big swings in financial markets would be an expansion of fighting. Any number of scenarios could unfold that could ensnare additional combatants. Here again, the probability of this risk manifesting has been heavily discounted by investors. The consensus view is that the conflict between Israel and Iran will not grow to include other participants other than the US bombing intervention on June 21.

The main reasoning is that Iran has limited ability to expand the battle. The Iranian military is designed to maintain cohesion at home and is not structured or resourced for direct foreign entanglements. Author and Middle East expert Amin Saikal describes Iran as a “pluralist society with a complex history of rival groups trying to assert their authority”. Add in the challenging mountainous terrain and it’s clear to see why the Iranian military is more inward focused. Iran has instead relied upon a number of proxies for engagement outside of their borders, including Hamas, Hezbollah, and the Houthis. The allied proxies which Iran has relied upon have all been largely defanged by the Israelis over the past 18 months.

There also seems to be little interest or strategic imperative among other observers to get involved or see the conflict expand. Under the Trump Administration, the US has been signaling its intention to be less involved in global conflicts. While the US felt it strategically necessary to intervene albeit briefly, the decision was contentious even within President Trump’s cabinet and has been heavily criticized. The US has little to gain from continued involvement and worries about the impact of higher oil prices on consumer sentiment. European powers have been notably uninvolved.

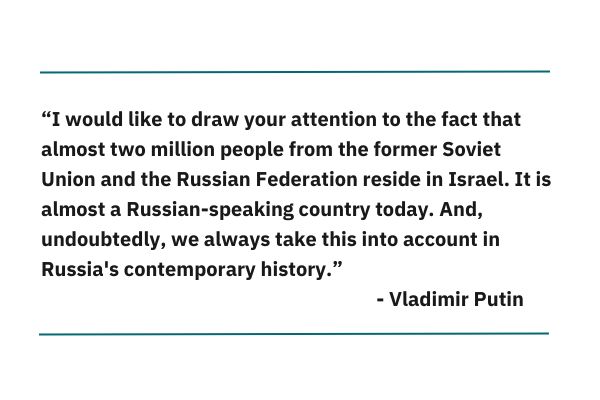

Moreover Iran’s two largest allies outside of the region—China and Russia—have no interest in a larger conflict. Russia is already overextended in the Ukraine conflict, and a large ethnic Russian population resides in Israel. According to Israel’s Central Bureau of Statistics, today there are around 1.3 million Russian speakers living in Israel, representing around 16% of total population, who Moscow cannot afford to alienate. Putin was recently quoted as saying “I would like to draw your attention to the fact that almost two million people from the former Soviet Union and the Russian Federation reside in Israel. It is almost a Russian-speaking country today. And, undoubtedly, we always take this into account in Russia's contemporary history”. China also wishes to avoid an expanded war as they remain a large energy importer, especially of hydrocarbons. They are dealing with their own problems at home and abroad, and Xi Jinping is disinterested in any conflict that will drive oil prices higher, even if the impact is temporary.

Meet Your Expert

Grant Johnsey

Grant is responsible for delivering capital market solutions to institutional clients across agency brokerage, transition management, security finance, and foreign exchange.

Northern Trust Securities, Inc.(NTSI), Member FINRA, SIPC and a subsidiary of Northern Trust Corporation. Products and services offered through NTSI are not FDIC insured, not guaranteed by any bank, and are subject to investment risk including loss of principal amount invested. Additional disclosures are included in the link, see http://www.northerntrust.com/ntsidisclosure

Business Continuity Notice- Northern Trust Securities, Inc.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.