- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

My weekly perspective on global market developments and their potential broader implications

JULY 22, 2023

Truth

All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident. Schopenhauer1.

I’ve often found this a good framework for assessing market trends. It echoes Templeton, bull markets are born in pessimism, grow on scepticism and die on euphoria. Plenty of what we’ve discussed recently could fit into one of these buckets; abatement vs exclusion, commodities, UK equities and selling long-bonds - all ridiculed. Brazil and Japan – rejected (even by Blackrock until recently). Mega-cap tech faced rejection in Jan but transitioned closer to become self-evident. And AI is, well, “the biggest platform shift, ever, duh, just ask Goldman’s”, who argue it’s a $7T opportunity, which combined with $8T they penned for Metaverse, could add 15% to global GDP by the end of the decade…..!! Whether likely (helpful) or not, these expectations exist, suggesting the opportunity to positively surprise, may not. Outside the mega-cap tech names where the majority of AI value will likely concentrate (see below), I remain biased towards the earlier stages of this framework. And as it relates to the US, it’s the better value sectors exposed to higher capex and state largesse, than those reliant on monetary factors, like a lower discount rate. Fading the Fed in favour of Fiscal.

Round trip

I think US markets could be range-bound for years. Major indices may go nowhere over time, despite wild rotations underneath and with only a handful of transcendent stocks. In a market like this, a good selling discipline is critical; the ability to take profits when you can, not when you have to. It’s also one of the hardest things to find in a manager. Why? I read recently the neural networks controlling prediction are the same that control memory, suggesting biological and not just behavioural factors are at play with recency bias, extrapolation and endowment effects. It explains why we fall in love with stocks. Such leads to a common investment error Clare Flynn Levy at Essentia Analytics calls, round-tripping, where managers hold onto their winners until they become losers. She believes such value destructive habits can be solved for, least minimised, and the alpha capture from such can be significant. Her own studies suggest +120bs. While some large managers have sophisticated risk management functions that coach as well as caution, many smaller ones do not. To level that field, I’m suggesting my managers take some of my research budget (once Rachel Kent’s recommendations are implemented) and apply it to coaching or behavioural analytics. That way I cover not just their IQ, but their EQ too. That which Buffett believes provides real edge.

All it takes to win

Carlos Alcaraz won an epic men’s Wimbledon title by winning only 50.3% of the points (168 to 166). That’s a pretty slim hit rate. It’s a bit like investing. You will not win all your points. But make sure the points you do win are ones that count. The ones that really ‘pay-off’. Your risk managers can help here through things like position-sizing or implementing a process of review to reveal areas for small, yet incremental improvement. It’s often small margins – 0.3% in the case of Alcaraz, that defines wining vs losing.

Creativity is a contact sport

Watching Alcaraz emotionally embrace his team at the end of the final, was a reminder that success in anything, even singles tennis, is a team endeavor. It involves different expertise and perspectives, with the same purpose to produce good results; greatness is in the agency of others. The same can be said of innovation. Of creativity. Years ago, I asked a then-CEO of GSK what were the environments that created their biggest drug breakthroughs, innovations or ‘aha’ moments? I was surprised by his answer. It wasn’t the lab. It was the café at lunchtime, where ideas from other disciplines would ‘bump into each other’. Innovation, he said, occurred at the margin of disciplines. Creativity is a contact sport.

So, can AI be creative?

This idea of creativity from human interactions got me thinking about Generative AI. Can it replicate the café, as above? I hear a lot about large language models (LLMs) in future being able to talk to other LLMs, which could, I guess, lead to new and creative insights. But one thing’s unclear. If LLMs are going to ‘bump into’ other datasets and ‘generate’ new outcomes, new decisions, new data, that must assume these (unique) data sets are freely open and available. But why would the owners of that data, give it away? For free? It’s their one scarce resource, their value proposition. And what might this say for cyber risks, for data privacy, for energy use, for ESG? Might we instead end up with more firewalls, more paywalls, more private server capacity, more security, less freely-available data, higher prices and an even warmer planet? I, of course, don’t know, but we, as an industry must find out before we spend the billions that Goldmans are expecting us too.

I’d rather have a beer with Einstein

According to Mo Gawdat, the former Chief Business Officer at Google X, ChatGPT already has an estimated IQ of 155, not far off Albert Einstein at 160. But in the move from ChatGPT 3 to 4, its intelligence has increased 10x. Okay, so the value of human intelligence and knowledge-based activities might commoditise over time (thank God my children can spot-weld). But as Einstein said, the true sign of intelligence is not knowledge but imagination. Creativity is intelligence having fun. And who would you rather have a beer with. Einstein or an AI?

Where did all the painters go?

I was fascinated reading about the plight of painters at the dawn of photography. As a photo could do in seconds what a painter would take hours, if not days, photography represented one of the most disruptive technologies in history (to painters, at least). But not all painters. Yes, those trying to replicate objective reality, died. A photo was so much better. But those who saw their art as a way to be more expressive, more creative and more human, flourished. That’s a hopeful metaphor for the world we live in. For the alternate view, a world where we let the AI decide – it becomes the tool, not a tool in decision making – doesn’t sound much fun. For clue of how things might transpire, I suggest watching the movie Idiocracy, produced in 2006. It’s oddly prescient in terms of the current discussion. It’s also hilarious (with the same lead as from Old School).

Breaking down the silos

Back to business. When I talk to CIOs it’s apparent they’re preparing for a world where the range of potential outcomes increases. A world that might require new assets, new geographies and expertise. And as change seems to happen at ever-increasing rates, they appreciate they also need to become more open, more flexible and agile (see above: endowment effects). But what worries me is that these challenges are often viewed solely from the perspective of the investment office. Too little thought is given to operations, to technology and to new the data sets and relationships that will be required if change is forced on them. In other words: a successful strategy is dependent on structure more than ever before. And so, it’s critical that operations, data and investment teams work more closely together – as one team, not separate silos. While creativity is a contact sport, so too, it seems, is implementing change.

Benefits to many, value to a few

Some of you might remember that before the IPO of Facebook (now Meta), Aviate Global (the brokerage firm I co-founded) produced a video featuring Neil Campling, suggesting Facebook could become the biggest company in the world. It was a bold call, with a market value at the time of only about $10B. Our rationale, simplistically, was if they win the landgrab via selling addiction, for free, then once everyone was hooked, they could create enormous value selling high-margin products (like advertising) through that network. I wonder if that playbook is now being used with AI. Meta has released an open-source version of their AI model, Llama 2, for public use. This LLM, which can be used to create a ChatGPT-like chatbot, is available to start-ups, established businesses and lone operators. For free. The plan, I guess, is build an eco-system (Big Pharmas café, but on steroids). One where they gain a front row seat on every new creation, idea and application that’s generated, in real time. But this ability to leverage their technology, distribution and scale in order to dilute competition and control content, is not isolated to Meta. It extends to all large platforms. And while we buy into the idea that AI will benefit us all, its value may concentrate in the hands of just a few. Those with the compute, the data and the networks.

Rotation – cont.

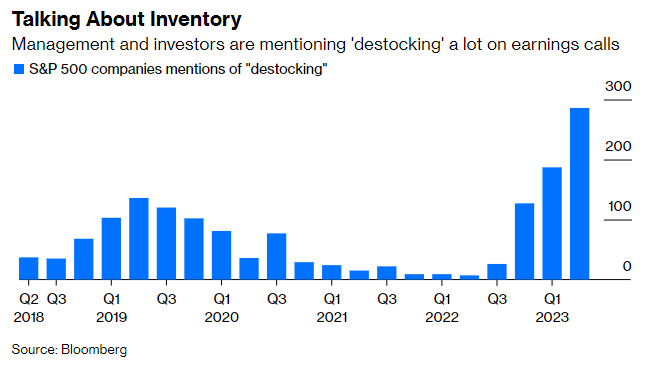

The stories we tell – the narratives – matter. How we act today is often a function of what we expect in future – a maxim implanted into every central banker. Procurement managers, too, are required to look ahead and figure out how much inventory they will need relative to expectations of sales growth. And what story have they been told all this year? Recession. So, what’s been their reaction function? To de-stock. See below.

Source: Bloomberg: It Feels Like 'Lehman II’ in This Crucial Industry, 29 June, 2023 (note: free trial registration available)

But what if, as the market’s been signalling (with bank stocks joining in this week), an emergent narrative is developing, one that moves from recession to resilience, maybe even growth? Could de-stocking turn to re-stocking at a time of resurgent capex in manufacturing? We discussed last week about the idea a fiscal put might now be in play, one favouring assets exposed to state largesse, more than those hoping yields head lower (and terminal values higher). If we’re right, it’s occurring at a time many are underweight such things as commodities (per the Bank of America Global Fund Manager Survey2) and I’m still being ridiculed for being bullish the UK.

Ridicule

Being a bull on UK assets is hard and my ego has hit new lows. Readers last week were angry I inferred Kingspan was British. It is, in fact, Irish. In my defence I was referring to its UK listing, although 98% of shareholders even decided to de-list it this week! Next came the ignominy of learning that if the UK was a US state it would be poorer than Mississippi. And then, the fatal blow, news the Orkney Islands want to secede from Scotland and become a self-governing territory of Norway. Brexit, Megxit and now, Orkxit. To be fair, they might have a point. Scotland has GDP/capita of £33,000; falling life expectancy and its former leader has been arrested. Norway, by contrast, has a gdp/capita of c£80,000;, has rising life expectancy and its “handsome, wholesome…population are regularly found to be among the most satisfied in the world” 3. That aside, I remain bullish long term, and was reminded why after seeing another US PE firm bid for a UK asset – this one a £8B fund manager called Gresham House with exposure to scarce albeit future fit assets like energy storage and energy. They paid a 68% premium on the AIM market. The message here – if we don’t buy these assets someone else, probably in America, will.

FYI I am about to begin a summer holiday and therefore The Weekender will be on hiatus until Saturday 12 August. I look forward to connecting with you when I return.

1 Quote generally attributed to Arthur Schopenhauer, German philosopher (1788 – 1860)

2 CityWire: Global funds drop commodities but bet on soft landing, 19 July, 2023

3 The Economist: Why the Orkney Islands are considering joining Norway, 12 July, 2023

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.