- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Weekender

Fortnightly perspectives from Gary Paulin, Head of International Enterprise Client Solutions, on global market developments and their potential broader implications

April 26, 2025

WHAT COULD GO RIGHT?

Flip the script

Back in January, riding a wave of euphoria, we ran a pre-mortem: what could go wrong? That exercise led us to consider the merits of buying cheap insurance via puts – a prudent hedge. Fast-forward to today, sentiment is deeply negative.

So, let’s flip the script: what could go right? This isn’t a forecast through a crystal ball , but a mental stress test to challenge the prevailing gloom. Some of you will push back – and that’s exactly why we do this.

As Munger said, know the counterargument better than the arguer...

So, what could go right?

- As the storm of bad headlines fades, markets take stock and see a surprisingly resilient picture: US stocks are up 8% year-over-year. Foreign markets have done even better –UK +15%, Germany +23%, Hong Kong +27%, Argentina +90%. The dollar index (BBDXY) has weakened, but only modestly (-3% YoY), and oil prices are down 24%, easing inflation pressures. US Treasuries have rallied. Meanwhile, China’s Shanghai Property Index – our best proxy for Chinese consumption and a key factor in US-China trade talks – is up 11% and breaking higher. Its Economic Surprise Index (CESICNY) is climbing too.

- People are wealthier than a year ago. Inflation is fading, recession fears are ebbing, and stimulus is on the horizon – from direct payments (DOGE checks), tax cuts, deregulation, to rate cuts by ECB and BOE, German military Keynesianism, Indian fiscal stimulus, and improving Chinese consumption. The market “looks through” the inevitable earnings hiccup caused by trade tensions. US Treasuries regain safe haven status as data shows recent selling was just SWAP unwinds. A weaker dollar and lower oil are now viewed as stimulative – flipping the narrative from capital flight to liquidity-driven risk appetite. This is exactly what Scott Bessent, former macro-trader, now Treasury Secretary, predicted.

- Elon Musk returns with his latest trillion-dollar vision: humanoid robots. He claims they’ll solve the demographic cliff and create the largest addressable market of his lifetime, potentially adding trillions to Tesla’s valuation. Bold? Absolutely. Plausible? We’ll see. But it’s the kind of moonshot thinking that can shift market psychology.

- Investors are waking up to liquid alternatives as a real option versus illiquid private equity, with unlevered dividends becoming the new IRR—especially in dividend-rich markets like the UK and Hong Kong.

- Larry Fink and others turn bullish on UK assets. FT journalists turn giddy because the FTSE 250 index can be bought for about 1x book, on 10 times earnings which are expected to grow double digits, leaving room for higher dividends starting at 3.9%.

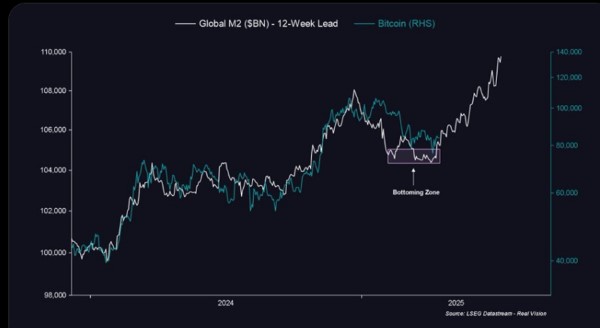

Global money supply hits a new record high. Adjusted for USD weakness, it’s already at a record (see white line below). A weaker dollar helps the rest of the world deleverage and reflate.

Source: RealVision

- Central banks slash rates. The Fed follows suit now inflation is cooperating (Trueflation at 1.4%, lowest since Nov 2020).

- Bessent’s push to exempt bank treasury holdings from SLR could free up lending capacity, restoring bond market depth, allowing foreign investors time to repatriate and prop-up their domestic economies. More rebalancing. And USTs rally.

- Bitcoin, which tracks global liquidity 83% of the time, rallies signalling a tech rebound (having led tech down). Binance advises sovereigns on crypto policy and strategic reserves. Remember, when liquidity flows, risk assets often follow.

- Contrarian signals abound: brokers calling a market top, first time gold bulls emerging, The Economist warning of a dollar crisis. Yet, as the WSJ concludes, Trump is a disaster everywhere, ‘just not in the data’.

- Trade tensions ease as punitive tariffs push partners to negotiate. Trump demands “burden-sharing” for market and security access, settling for higher NATO defence spending, domestic consumption boosts, and lower trade barriers for US goods. Deal frameworks for South Korea, India, UK, and Japan emerge, setting templates for Europe and even China. Markets cheer as trade friction gives way to something resembling free trade.

- At 8pm on June 14th, Trump calls Xi to exchange birthday wishes. They exchange symbolic gifts – a private viewing to A Minecraft Movie and a Nintendo Switch (made in China, sold by Japan) both symbols of globalisation – and are filmed eating McDonalds and teaming-up in Fortnite against Putin and Kim Jong Un. The optics? Priceless. The message? Cooperation over conflict.

- Ninety days after Liberation Day (April 2 2025), Trump unveils a “beautiful” trade deal just in time for Independence Day celebrations. He reminds us: a strong president equals a strong stock market. The Trump Put is back, alongside the Fed’s. Markets rally.

Are these scenarios likely? Probably not. Impossible? Never say never.

New regime: the next 40 years

Whether or not this optimistic scenario unfolds, the longer-term market regime is shifting. As we discussed two years ago now, for asset allocation, the future is not in the past. The tools that worked over the last forty years won’t necessarily serve the next forty. Equities remain the weapon of choice, but factor and regional selection will matter more. If multiples compress – as they often do in range-bound markets – earnings growth and dividends will drive returns, not P/E ratios.

Value and quality will be prized. The rare skill of selling will gain a premium. Investors will relearn mean-reversion, the P/E cycle, and that every asset has a life cycle – even private equity.

Every asset has a life cycle

We’ve long cautioned about increasing private equity allocations. All assets mean-revert, even “exceptional” ones like PE. The flood of capital inevitably suppresses returns, especially in volatile markets with few exits. Signs are clear: rising leverage to fund distributions, retail inflows, indexation – classic late-cycle markers.

Increased regulatory scrutiny and transparency erode the “mystery”, where margins often hide. Headlines about the “death of PE” and the “end of the Yale Model” are just part of the clearing process. Yale’s decision to rebalance has been months in the making. More secondaries are coming as IPOs remain shuttered. Expect single-digit DPI returns for a while, making dividend compounders more attractive. But, if under-allocated, now is a good time to add – pricing is rationalizing, and distressed assets may emerge.

Expect a regional shift away from the US toward Europe, the UK, and Asia. Your dollars will be warmly welcomed, reserve status or not!

Whoever has the gold makes the rules

You know my long-standing views on gold: it remains the ultimate neutral reserve asset, alongside bitcoin. Its role will only grow, but the recent headline frenzy and new bulls emerging could mean a pause – and better entry points ahead. Trump’s recent Truth Social post: “He who has the gold makes the rules” – is a reminder that gold reserves still underpin geopolitical power.

But the US appears comfortable with its stash for now.

Pope Francis: RIP

Pope Francis took his name from St. Francis of Assisi, founder of the Franciscan order. Though not a Franciscan himself, he honored their legacy. So too should capitalists. The Franciscans played a critical role in banking, mortgages, and capitalism, through pawnshops that allowed collateralized lending without violating usury laws. This evolved into the mortgage market (mort = death, gage = pledge), a reason why Catholics are to this day among the world’s largest non-government landowners. They also invented double-entry bookkeeping, fueling company formation and capitalism itself.

The current papal frontrunner, Cardinal Parolin, is Italian – perhaps a sign of continuity.

Receive The Weekender

Register your interest in receiving Gary's commentary direct to your inbox.

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.