- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Transatlantic Tussle

U.S.-Europe negotiations involve more than just tariffs.

By Vaibhav Tandon

“Keep calm and carry on” was the mantra adopted by the British government in 1939 as the country prepared for World War II. The message helped to keep the population level-headed as the nation endured mass attacks on its major cities.

Britons remained calm with the new U.S. administration and went on to strike a trade deal. But their European counterparts may struggle to maintain the same poise in the face of the latest tariff bombshell from the U.S.

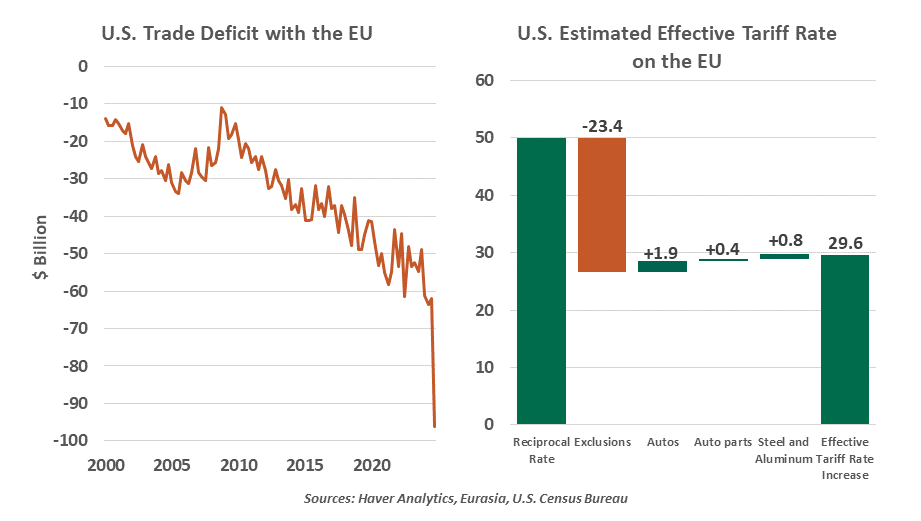

Late last week, President Trump threatened to inflict 50% duties on all goods coming into the U.S. from the European Union (EU). The U.S. currently applies 25% duties on European steel, aluminum and cars, and a blanket 10% on all other EU products. The latest punitive move would have pushed the effective rate to 30% on European imports.

The president walked back this threat within a matter of days, delaying implementation until July 9. But the sudden flurry served as a reminder that there is a lot at stake for the two transatlantic partners.

A trade war with Europe will be far more consequential for the United States than deterioration in commercial ties with China. Total trade with the EU accounted for almost 5% of America’s gross domestic product (GDP) in 2024, compared to 2.2% of GDP with China. Europe is a major buyer of U.S. energy, autos and airplanes. European firms account for close to two-thirds of global foreign direct investment in the U.S.

America is the top destination for European goods, contributing to a $236 billion EU surplus in 2024. The EU has reportedly offered a €50 billion deal to address this large imbalance. The proposal includes increased purchases of American liquified natural gas (LNG) and agricultural products like soybeans. According to some observers, the bloc has also offered strategic cooperation in areas like energy, artificial intelligence and digital infrastructure. The Europeans are willing to reciprocally slash transatlantic tariffs to zero in areas like autos and industrial goods. They are also open to reducing dependence on China and initiating tariffs against subsidized Chinese exports, furthering another key objective of the U.S. administration.

A durable trade agreement between the U.S. and the EU seems a long way off.

The EU’s offer to import more from the U.S. will help reduce the bloc’s goods surplus. A long-term deal focusing on U.S. LNG imports would not only give America’s hydrocarbon industry greater access to a large market but would also go a long way to help address Europe’s energy security. Eliminating levies on sectors like autos where differences are stark (EU tariffs cars at 10% vs. 2.5% in the U.S.) is a compromise that should be welcomed by U.S. policymakers and exporters.

But these proposals did not satisfy the White House, leading to last week’s escalation. America’s insistence on addressing non-tariff barriers like high value-added taxes and regulatory burdens in member states is perhaps the biggest roadblock in the ongoing negotiations. Given the European Commission’s inability to offer concessions on domestic tax and regulatory frameworks, deemed as internal policies of member states, this could emerge as the deal-breaker. The EU is also reportedly opposed to a U.S.-U.K. style trade agreement that leaves a blanket 10% U.S. tariff in place on its exports.

With key differences unresolved, the threat of transatlantic escalation in trade tensions remains in place. The two markets have the world’s largest trade association, with goods and services worth over $1.5 trillion changing hands each year; strained commercial relations are not in either side’s interest. According to the American Chamber of Commerce to the European Union, affiliate sales of EU firms in the U.S. have surpassed $3.5 trillion while that of the U.S. affiliates in Europe crossed $4 trillion in 2024. Transatlantic investments could become collateral damage if trade issues cannot be resolved as the U.S. and Europe are each other’s primary source and destination for foreign direct investment.

Europe cannot afford a trade war with its largest export market, which accounts for a little over one-fifth of all EU goods exports. Economies like Germany and Ireland, which have a high ratio of U.S. exports to GDP, would suffer the most. At a sectoral level, machinery, pharmaceuticals and autos will be the most severely affected, as they account for well over half of the bloc’s shipments to the United States.

The current tariff levels are already seen as unacceptable in Brussels, so an escalation will likely prompt retaliation from the EU. Member states have already approved a €21 billion package of up to 50% tariffs on American goods like corn, wheat, motorcycles and clothing. Though the implementation of these levies has been temporarily suspended, EU capitals are already discussing further countermeasures covering €95 billion of U.S. goods covering aircrafts, cars and bourbon if negotiations fail.

America’s trade exposure to the EU exceeds its exposure to China.

Europe also has a strong leverage with the United States in services trade and has indicated its openness to raise the stakes by going after America’s tech corporations. These moves would risk an escalatory cycle like the one that we witnessed with China earlier this year.

Though far-fetched, Europe could further widen the scope of the trade war by threatening to curb buying of American assets. European investors hold about $2.9 trillion in U.S. Treasuries, close to $9 trillion in U.S. equities, and over $2.6 trillion in U.S. corporate and other bonds. Even a small unloading of these holdings could drive a strong sell-off in Treasuries and the dollar.

With significant mutual economic risks, we think an escalatory spiral will be avoided. In the event of a transatlantic trade war, neither side will be able to keep calm or carry on.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.