Trade Progress: Small Steps

The signal of announcing trade pacts is an important start.

By Carl Tannenbaum

Earlier this year, I had the misfortune of visiting clients in Canada the day after the country had been targeted with substantial U.S. tariffs. At one event, I was the only American in a room of 400 people. While the mood within the audience was apprehensive, I was able to complete my presentation without incident.

When this publication reaches you, I will be visiting clients in Asia. Trade tension leading up to this year’s trip to the region had been rising: for reference, the weighted average U.S. tariff rate on Canada is 13%, while the comparable rate on China was targeted to exceed 100%. While I have always been received warmly in the Far East, I was preparing for high anxiety.

Fortunately, some relief arrived a week before my departure. Representatives of the U.S. and China reached an agreement to temporarily roll back tariffs that the two had leveled against one another. The change of direction on the trade front has been welcome, but we might still want to manage our enthusiasm.

Officials within the second Trump administration pledged to realign global commerce. They believe that the United States has been taken advantage of by exporters, and has lost control of critical industries. This view prompted a frenzy of tariff announcements.

The scale and scope of trade restrictions caught many off guard. Uncertainty over what might occur next has made it difficult for firms to plan. Markets corrected, and global recession became a real possibility. Even though the reciprocal tariffs were paused, there appeared to be no clear “off-ramp” to avoid a trade war.

But late last month, the tone seemed to change. Treasury Secretary Scott Bessent, a more moderate voice, took on a leading role in negotiating policy. He noted that “America first does not mean America alone. To the contrary, it is a call for deeper collaboration and mutual respect among trade partners.”

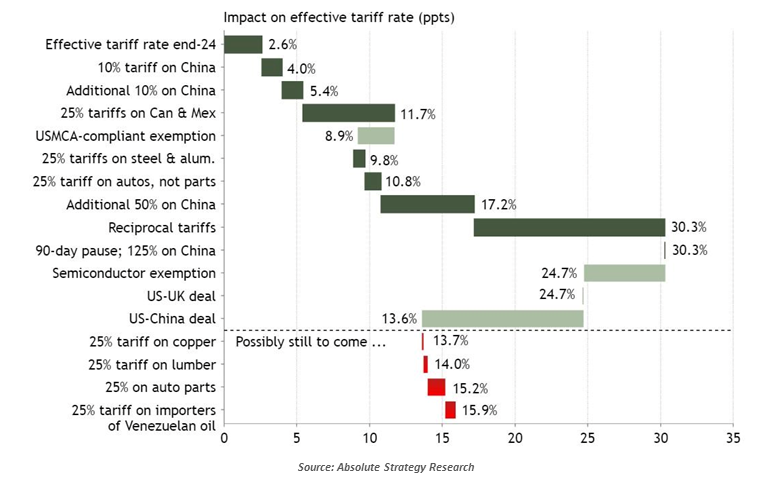

Recent trade pacts, while limited, may represent an important turning point.

Trade talks were initiated with a range of countries. Some early agreements with smaller markets were anticipated, but negotiations with larger countries were expected to last for many months. Surprisingly, though, deals with the U.K. and China came together quickly.

The former was a somewhat lighter lift. The United States has a goods trade surplus with Britain, and Prime Minister Keir Starmer was among the handful of world leaders who had established a good rapport with President Trump. Modest relief was agreed on auto shipments in each direction, and the U.K. was granted a tariff exception on steel and aluminum exports. Both sides trumpeted the success.

But the terms were far from comprehensive. The 10% U.S. baseline tariff on all imports from the U.K. remains in place. And Britain’s digital services tax, which the White House would like to see removed, is still standing. Analyzing the deal, the Brookings Institute termed it “less a done deal than a first installment in ongoing negotiations.”

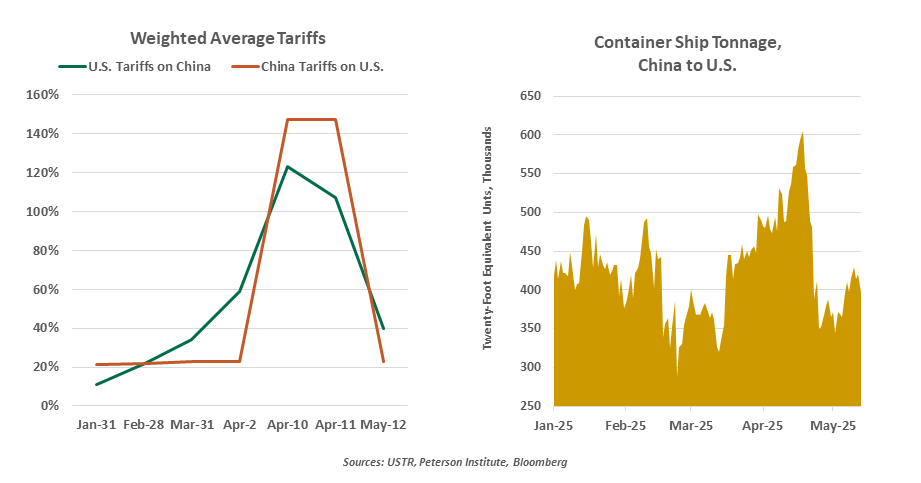

The outcome of recent trade discussions between the United States and China in Geneva was unexpected. Friction between the two that started during Trump’s first term was never resolved, with those tariffs still in force. Then, the two engaged in successive rounds of escalation last month, with aggregate levies climbing to well over 100% in each direction. At these levels, the two countries were essentially declaring a trade embargo with one another across a range of products.

Even though the U.S. granted some relief to technology imports from China in mid-April, most thought that the two countries would dig in for the long haul. Each side believed that it had an upper hand. China did not think American consumers would long tolerate shortages and high prices for essentials sourced from Asia, and felt confident that its own citizens would be patient as its leaders played a long game.

On the other side, Washington senses weakness in the Chinese economy, which is struggling with sluggish domestic consumption and a real estate hangover. Curtailing exports, which are the main avenue of Chinese growth, could tip their economy into recession and place their asset markets under pressure. The thinking within the Administration has been that Beijing would be anxious to make a deal on favorable terms for the U.S.

Defying expectations, the two sides agreed to roll back some tariffs for ninety days. This provides temporary clarity to importers, who are expected to resume normal ordering after a tariff-induced slump. The deferral will limit the hit to Chinese economic growth and to American inflation, outcomes that both sides will appreciate.

Nonetheless, U.S. tariffs against China are still set to reach 40%. That is a significant escalation from the beginning of the year. Challenging discussions covering technology, rare earth minerals and fentanyl lie ahead. And if the Administration sticks to its agenda of re-shoring industrial output, lasting sanctions on Chinese production will almost certainly be a part of the plan.

We’re beginning to see the boundaries surrounding U.S. trade policy.

Recent developments illustrate a couple of boundary conditions for U.S. trade policy. On one side, the Administration has demonstrated a sensitivity to the risks that economic isolationism present to the American economy, consumer sentiment and the financial markets. Uncertainty remains high, but it appears (for now) that we have seen the limits of tariff threats.

On the other side, it does not appear that the United States will let go of baseline tariffs. These are deemed essential to the trade agenda, and they are being relied upon as a revenue source for the U.S. Treasury.

Hoping to avoid repeating the discomfort I encountered in Canada, I recently took the step of sending my international travel schedule to the attention of the U.S. Trade Representative, asking him to conclude negotiations prior to my departures. My reputation needs all the help it can get.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.