- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

US Economic Outlook | April 21, 2026

Mission Driven

The domestic economy can grow despite inflationary risks.

We hold out hope that the ceasefire in Iran will lead to a lasting truce. Even in this best-case scenario, supply disruptions in markets including oil, gas, fertilizer, helium, plastics and aluminum will take months to recover from.

For the U.S., the primary economic risk of the war remains inflation: energy prices have jumped, with room to climb further. Other supply chain disruptions may lead to higher prices for food and manufactured goods. And the most recent inflationary cycle taught us that once inflation ascends, it can be slow to settle.

Higher costs can cut into overall spending. Material shortages may also impair consumption and efforts to reshore production. The sooner that hostilities are wound down, the more likely that these outcomes can be avoided.

Despite this new source of uncertainty, we do not anticipate a significant slowdown in activity. The economy has shown considerable resilience during this decade; favorable market outcomes will continue to propel spending, and AI-related investment remains a force. Following are our thoughts on the outlook for the domestic economy.

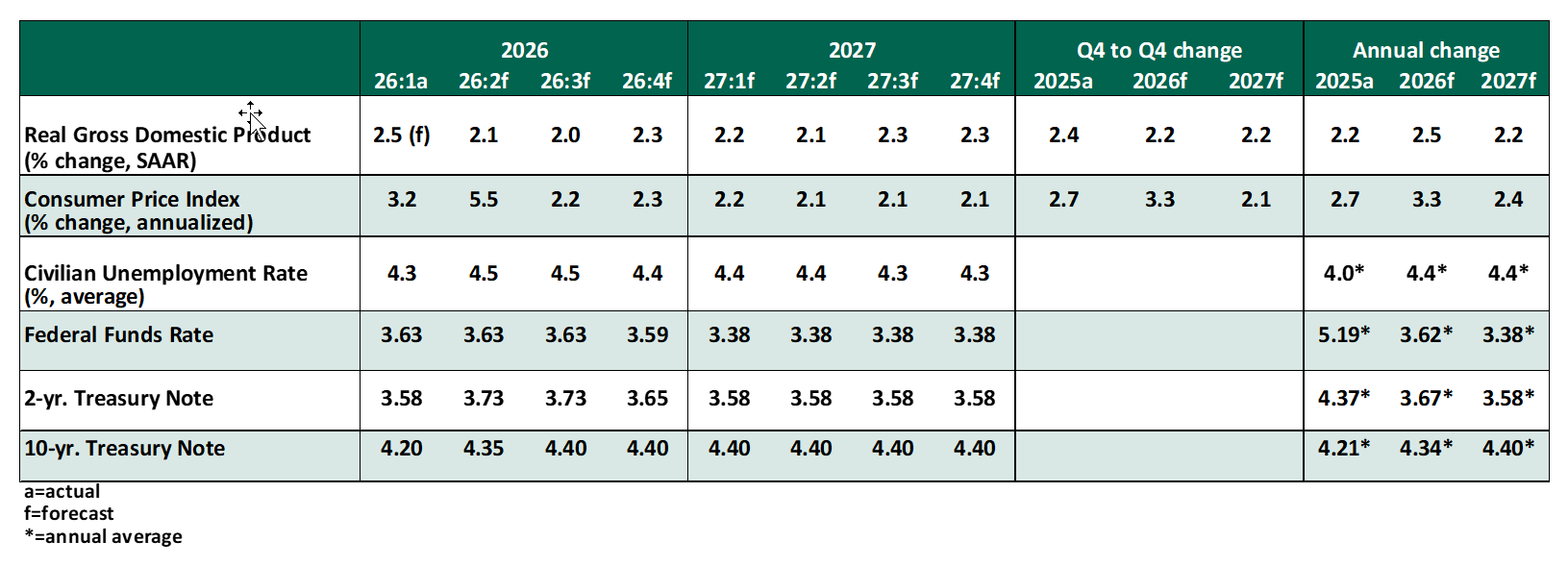

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The March employment report showed surprising strength, with 178,000 new jobs created. The unemployment rate fell one-tenth to 4.3%, driven by a decline in the labor force. The favorable reading offset a negative report in February; the data has become quite volatile. On net, the private sector has gained an average of 79,000 jobs over the past three months, likely a sustainable pace in light of reduced government employment and slower immigration.

Labor market activity remains stagnant. Last summer, job openings settled to a level below the number of unemployed persons; openings have since held flat. However, the rate of hiring touched a low last seen in 2011 (excluding the pandemic), and voluntary quits are also sluggish. Layoffs remain limited, with weekly initial unemployment claims holding at a low level. Those who have jobs are holding on to them, but the unemployed are having difficulty finding work.

- The March reading of the consumer price index (CPI) offered a first glimpse of the impact of the Iran conflict. Inflation stepped up to a two-year high of 3.3% over the past year, pushed up by surges in the costs of gasoline and fuel oil. Other than airfare, most other categories remained well-behaved. Core CPI (excluding food and energy) has gained 2.6% over the past twelve months.

- Monetary policymakers will be challenged to separate temporary distortions from sustained economic changes. Under current circumstances, rising inflation and a falling unemployment rate offer no justification for rate reductions. Our expectation of one further cut late in the year hinges upon the inflationary shock staying limited, without substantial pass-through to other categories. The possibility of a prolonged hold is rising.

- Retail sales remained strong in February and March, sustaining a broad-based annual gain of 4.0% in both months. The February reading on personal consumption illustrated both strengths and limitations of the consumer. Real consumption climbed 2.5% over the past year, but real personal income is tracking only a 1.1% annual gain. Savings closed this gap, with the rate of saving falling by a half a percentage point to 4.0% of personal income.

These divergent aggregates may be driven by diverging fortunes. Wealth effects are fueling consumption by higher-income consumers, while others are falling behind. In the near term, higher income tax refunds may sustain consumer spending in the face of higher energy costs, across all strata. Consumption gains are poised to persist, as well-heeled consumers will be less sensitive to inflation.

- A durable driver of U.S. growth has been investment, especially hardware deployed in the artificial intelligence (AI) boom. Nondefense capital goods orders grew a strong 0.6% from January to February. Conflict has not altered the case for most investment in equipment, and we expect this to provide a tailwind to gross domestic product throughout the year. New tariffs are still taking shape, but they should prove to be less of a shock to business activity this year.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.