The View from the Bond Desk – An Occasional Series

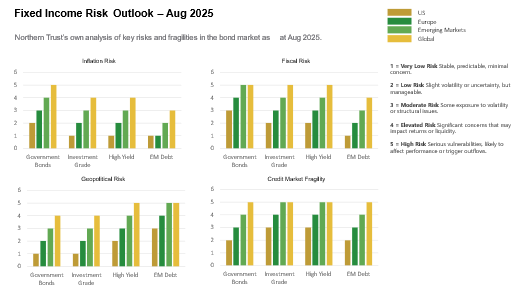

Investors in global fixed income markets should remain alert to several key risks that could disrupt flows and valuations in the coming months. Tariff-related inflation remains a top concern, particularly in the U.S., where recent policy shifts have introduced effective tariff rates of 13–17%[1].

While businesses have absorbed some of the cost increases, the risk of a broader price reset looms, potentially complicating the Federal Reserve’s rate path. If inflation proves stickier than expected, the Fed may delay or reduce rate cuts, impacting duration-sensitive assets. Additionally, fiscal uncertainty tied to the One Big Beautiful Bill Act (OBBBA) and elevated U.S. deficits could undermine investor confidence, especially if debt servicing costs rise or fiscal discipline erodes.

Geopolitical volatility also poses a significant threat. Although recent de-escalations—such as the Israel-Iran ceasefire—have calmed markets somewhat, tensions remain high, and any reversal could trigger risk-off sentiment. In Europe, the ongoing effects of the Russia-Ukraine war and energy price instability, add layers of uncertainty. Emerging markets face their own challenges, including local currencies strengthening as the US$ weakens (so from the perspective of a consumer sitting in Bangkok, imported things are more affordable but exported things are less attractive vs substitutes), bloated debt levels (up by double figure percentages YTD in many EM economies)[2], and vulnerability to U.S. trade policy shifts.

Moreover, credit market fragility is emerging, especially in sectors like U.S. office-backed CMBS, where refinancing risks are rising due to uncertain rate trajectories.

While corporate fundamentals remain broadly healthy, margin pressures and tighter spreads suggest limited upside, making security selection critical.

What is our outlook?

Given what we observe as of August 2025, we believe inflation risk, fiscal risk, geopolitical risk and credit market fragility map like this ↓

So what?

Levels of uncertainty that have not been seen for many years and signs of slowing economic growth in major markets like the U.S., is supportive of global fixed income; indeed, demand for fixed income remains elevated and resilient. Investors appear to have decided the bond market is a ‘safe place to be’, for the moment anyway.

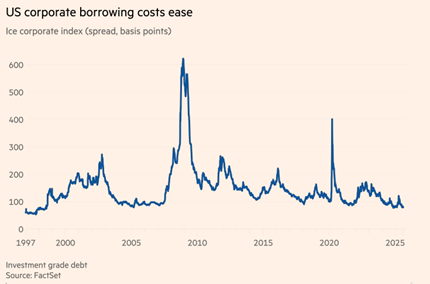

Investment-grade corporate bonds continue to attract strong inflows, with U.S. ETFs and mutual funds pulling in $11.6 billion between July 30 and August 6—marking the fifth-largest weekly inflow on record and the highest since late 2020 (JPMorgan).

Spreads over Treasuries have narrowed to just 0.80%, nearing levels last seen in the late 1990s.

In Europe, demand for investment-grade paper is equally strong, while junk bond issuance hit a record €23 billion in June, surpassing the previous high by €5 billion (JPMorgan). Japan is also seeing renewed interest in long-dated government bonds, with PIMCO—led by CIO Andrew Balls—turning constructive on the asset class amid a dislocated yield curve and 30-year yields trading above 3% as of May 2025.

Closer to home in Australia, APRA’s decision to phase out A$43 billion in hybrid Tier 1 capital instruments by 2032 is prompting investors to seek alternatives. These range from investment-grade bonds and private credit funds to listed investment companies (LICs) and bond ETFs. It’s a similar story in the AUD market—lower supply means that any new issues are quickly absorbed, reflecting strong demand across the credit spectrum.

In addition, central bank IR cut forecasts such as that of the RBA last week are fixed income positive.

In short, investors are engaged, active and buying any available bond liquidity.

Sources

https://www.ft.com/content/51ecaa00-c674-48d6-b2ce-eb6211e8cdd5

https://www.ft.com/content/7c6fa795-6e6e-457c-bc0e-54fbd2c5a65a

[1] https://budgetlab.yale.edu/research/state-us-tariffs-august-7-2025#

[2] Bloomberg data – Northern Trust analysis

Meet Your Expert

Gerard Walsh

Gerard leads Northern Trust’s Global Banking & Markets Client Solutions group, covering Equities, Fixed Income, FX and Securities Finance.

Meet Your Expert

Joanne Gadd

Based in Australia, Joanne Gadd currently leads as Head of Fixed Income, APAC at Northern Trust, where she oversees strategy and execution across the region.

IMPORTANT INFORMATION AND DISCLOSURES

Northern Trust Banking & Markets is comprised of a number of Northern Trust entities that provide trading and execution services on behalf of institutional clients, including foreign exchange, institutional brokerage, securities finance and transition management services. Foreign exchange, securities finance and transition management services are provided by The Northern Trust Company (TNTC) globally, and Northern Trust Global Services SE (NTGS SE) in the European Economic Area (EEA). Institutional Brokerage services including ITS are provided by NTGS SE in the EEA, Northern Trust Securities LLP (NTS LLP) in the rest of EMEA, Northern Trust Securities Australia Pty Ltd (NTSA) in APAC and Northern Trust Securities, Inc. (NTSI) in the United States. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures.

This marketing communication is issued and approved for distribution in the United Kingdom by The Northern Trust Company, London Branch (TNTC). TNTC is authorised and regulated by the Federal Reserve Board; authorised by the Prudential Regulation Authority; subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. This communication is provided for the sole benefit of clients and prospective clients of TNTC and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of TNTC. Any unauthorised use is strictly prohibited. This communication is directed to clients and prospective clients that are categorised as eligible counterparties or professional clients within the meaning of Directive 2014/65/EU on markets in financial instruments (‘MiFID II’). TNTC does not provide investment services to retail clients. This communication is a marketing communication prepared by a member of the TNTC sales & trading departments and is not investment research. The content of this communication has not been prepared by a financial analyst or similar; it has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. This communication is not an offer to engage in transactions in specific financial instruments; does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of individual investors.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.