- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Should We Party Like It's 1999?

Comparing and contrasting two tech-led cycles.

By Ryan Boyle

To be human is to fall into moments of nostalgia. The bias is natural: we look back favorably on the time that we gained new experiences, developed deep relationships and managed fewer responsibilities. Uncertainties that were of concern in the moment do not trouble our recollections. Those memories disregard the macro perspective of material gains made between then and now; the present is almost always better than the past.

My own struggle with nostalgia is that I came of age in the U.S. in the late 1990s. By many objective measures, it was a great time to be alive, not only for my carefree adolescence. Investors are now harking back to the fervor of the late 1990s. I will now set aside my fond memories and compare the economy today with that boom.

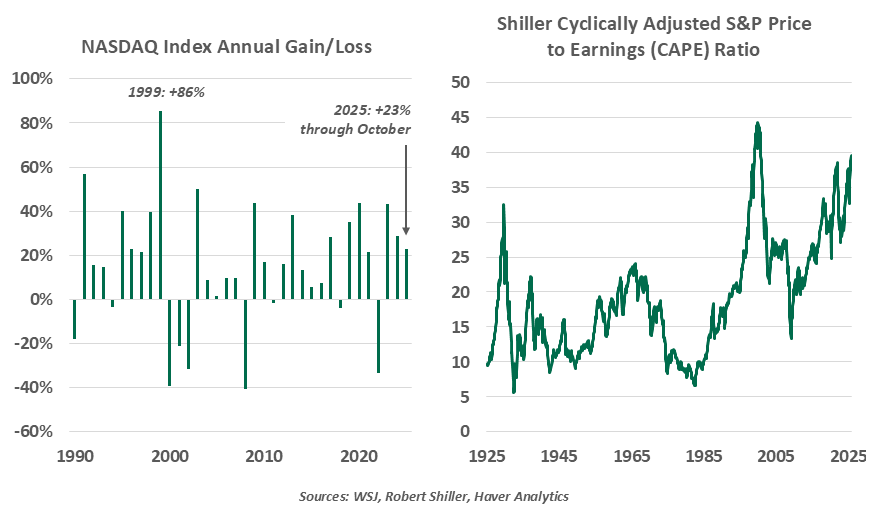

The obvious analogue between 2025 and 1999 is the technology-led equity rally. The Dot-Com bubble reflected optimism about the internet. This led to fervent investment, memorably characterized in a 1996 speech by former Fed Chair Alan Greenspan as “irrational exuberance.” Internet companies saw their stock prices skyrocket, regardless of their actual prospects or profits. While markets have been buoyant this year, the tech-heavy NASDAQ has not matched its massive gain seen in the year 1999. In hindsight, that was a bubble; what about today?

The current tech boom has both similarities and differences from the last one.

Valuing a stock requires subjective judgment about its future returns. There is no line beyond which an asset is empirically overpriced. Measures like the ratio of a stock’s prices to earnings (P/E) can suggest when valuations are stretched; lofty P/E values have preceded past corrections. Aggregated P/E ratios like the Shiller Cyclically Adjusted P/E (CAPE) are now approaching the highs seen as markets peaked in 2000.

The 1990s rally wasn’t only speculation. Businesses were investing in on-premise data centers and redeveloping older systems to survive the Y2K logic fault. Households and schools were buying PCs and getting online. Telecommunications firms were building networks to provide capacity for all of this growing demand. A true shift was underway in how jobs were done and how people communicated.

Today’s rally is led by artificial intelligence (AI), both the firms developing AI models and those providing the computing and power infrastructure to run them. Rapid AI advancements are fueling speculation of how much they may transform our lives, and thus speculation in this sector.

We are not equity analysts, but we collaborate with some good ones. Looking back on the Dot-Com bubble, our Northern Trust Asset Management colleague Gary Paulin observes better earnings quality this time around. Today’s tech firms are funding their growth with stable cash flows, offering higher margins that help justify their valuations.

Today’s zeitgeist may also be fueled by broader investor participation. Equities have never been more accessible. Whole movies have been made about irrational meme stock investments. More people today are watching prices rise and have a vested interest in averting a downturn.

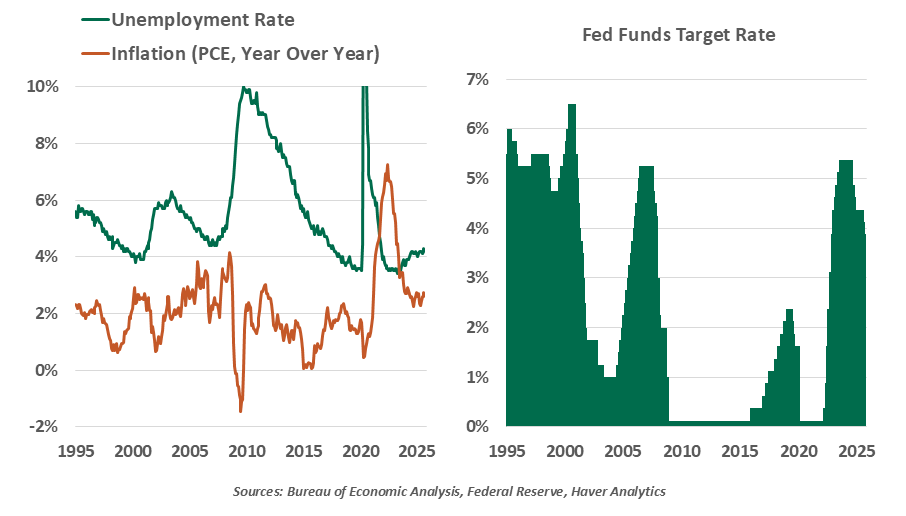

Both today and the late 1990s were characterized by tight labor markets. The Dot-Com boom continued a protracted recovery: the unemployment rate fell to 3.8% in March 2000, a 30-year low at the time. The prime-age labor force participation rate of 84.6% in January 1999 is still a record high. But the pace of hiring distinguishes the two eras. In the 1990s, anyone with marginal tech skills could readily find work. Information sector employment grew over 27% from 1995 to 2000, while total nonfarm employment gained 12%. Today, technology sector job prospects are challenged, with AI more likely to replace new jobs than create them.

Fiscal policy neither helped nor hindered either cycle. Both rallies grew from monetizing research that started with public subsidies. High incomes, higher tax rates and lower spending balanced the federal budget in fiscal years 1998-2001, an outcome that seems well beyond reach today.

Returns to technology investment may take longer than markets can tolerate.

The macroeconomic outlook has always offered reasons for worry. Global investors reckoned with the Asian financial crisis and the fallout of the failure of Long-Term Capital Management in 1998. Today’s worries around trade frictions, credit tremors and a slower China bring familiar unease.

Both eras saw the Federal Reserve trying to manage inflation against a persistently strong demand environment. In 1998, the Fed cut by 75 basis points to support the economy through macro shocks; after a seven month pause, the Fed then hiked 175 bps in a year to try to cool inflation, which accelerated through the end of the decade. The recent return to Fed cuts reflects a cooling labor market, but it may add fuel to the ongoing rally.

Looking back to the 1990s need not be just a matter of nostalgia. Those too young to have lived it envy the fortunes made as technology firms grew. Seasoned investors who worked through the cycle can warn us of the pain of a correction. Along the way, the cycle taught useful lessons.

Technology transformations are gradual and persistent. At the height of the Dot-Com boom, we still talked on landline phones, read newspapers and paid bills by mailing paper checks. Innovation and adoption did not end when markets turned; ongoing advancements built upon the investments made in the bubble. The story of AI transformation will run longer than this initial AI equity cycle.

Markets can stay irrational longer than we can stay solvent. Conventional pricing models could not defend the valuations of 1990s tech firms. An end was inevitable. Those who sat out missed strong returns, but those who shorted stocks were in peril. Investors should stay prepared for a potential downturn, but not try to predict its timing.

The first movers aren’t always winners. The hardware and telecom darlings of the 1990s faced reckonings of mergers and bankruptcies. Two of the “Magnificent Seven” firms that have underpinned today’s tech thesis were not formed until the 2000s, while the rest have undergone substantial changes. Future AI market leaders might not yet exist.

My favorite aspect of my age is that I was among the last to see the world before digital technology became commonplace. Many of the promised productivity gains of the 1990s came true, but not in the short timeframe that markets had priced. I was too young to invest and earn easy money, but I also didn’t lose in the correction that proved to be inevitable but survivable. Keeping the current era in historical context will help us to keep a cool head. I guess this is growing up.

Related Articles

Read Past Articles

Meet Our Team

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)

Carl R. Tannenbaum

Chief Economist

Ryan James Boyle

Chief U.S. Economist

Vaibhav Tandon

Chief International Economist

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.