China: Reluctance To Pivot

China needs to look beyond investment and trade for drivers of growth.

By Vaibhav Tandon

Every innovation follows a lifecycle, from breakthrough to ubiquity to obsolescence. The Edison bulb once lit up the world, transforming how we lived and worked. But it was ultimately replaced by more efficient and sustainable alternatives.

Similarly, China’s growth model was a marvel of its time. It illuminated global trade routes, powered industrial expansion and brightened up its urban skylines. But the glow of this economic engine is waning, and Chinese policymakers remain hesitant to switch to a more efficient source of light.

This reluctance to pivot was clear at the recently concluded Fourth Plenary Session of the 20th Central Committee. The leadership reaffirmed its confidence in the current growth strategy, signaling continuity over change, as their goal of “around 5%” full-year growth appears within reach.

Robust growth in the first half, propelled by trade distortions and consumer support, reduced the urgency to recalibrate the strategy. A 10% reduction in U.S. tariffs on Chinese goods, agreed upon this week, could provide further support to exports and headline growth in the short run. But it will not be enough to counter the drag from a host of domestic economic challenges.

A lasting de-escalation in trade tensions and barriers remains out of reach, with several critical issues still unresolved. U.S. restrictions on chip sales remain in place, as do China’s April controls on rare earths. The reciprocal tariff pause has only been extended by one year. In return, China has agreed to resume U.S. soybean imports. Both sides have also committed to postponing imposition of higher docking fees on each other’s shipping fleets.

Without a comprehensive trade deal and amid inconsistent policy from Washington, global corporations may continue reassessing their China exposure. This risks triggering a reconfiguration of supply chains that could jeopardize China’s role in global production networks.

While major targets under the 14th Five-Year Plan (2021-25) are on track, policymakers also flagged rising uncertainties heading into the 15th Plan, seen as an acknowledgement of structural headwinds facing China’s supply-driven economy.

China’s old growth model is losing steam.

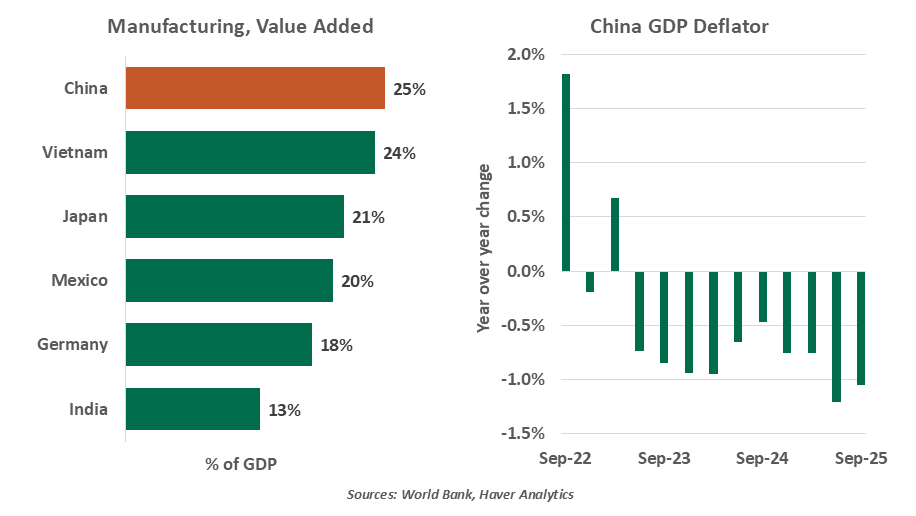

Deflation looms as the most immediate and consequential risk for the Chinese economy. Since 2023, consumer price inflation has lingered around zero, and the gross domestic product (GDP) deflator has been in an outright decline. Pipeline price pressures continue to point toward deflation, with the producer price index floating in negative territory for over 30 months.

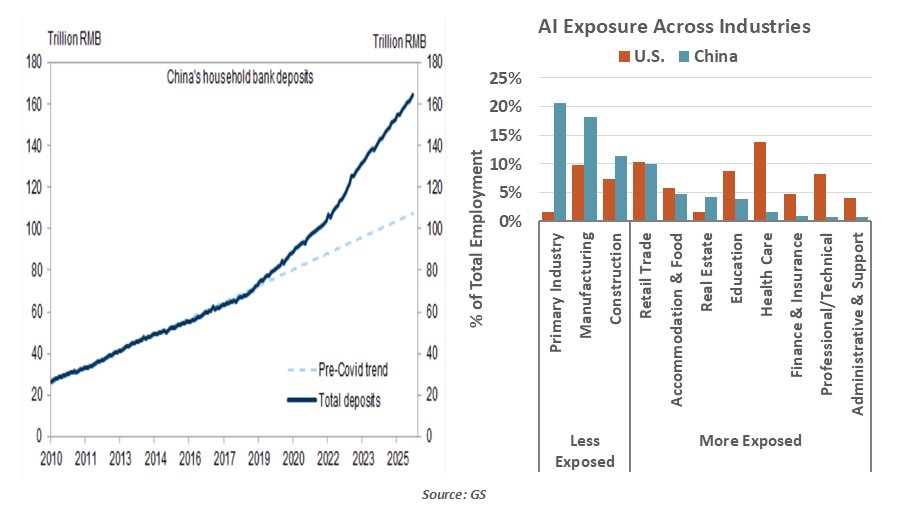

Deflation appears to be much more than a cyclical slowdown. Weak domestic demand, persistent overcapacity in key sectors and subdued confidence are the key forces behind depressed prices. Consumers have remained risk averse, reflected in elevated savings and a surge in household bank deposits since 2020. Consumer credit growth remains weak, reflecting reluctance to take on new debt. These patterns point to deeper structural and behavioral shifts.

China’s long-standing goal of transitioning from manufacturing and investment-led growth to a consumption-driven economy continues to face significant hurdles. Household spending remains subdued as a share of GDP, compared to major advanced economies. Government efforts to stimulate consumption, including measures like boosting the nationwide childbirth subsidy, have yielded limited results so far. Sustained deflation could entrench expectations of falling prices, discouraging spending and investment. A cycle of stagnation could get underway.

Demographics are also becoming unfavorable. For the first time in decades, China’s population is shrinking. The fertility rate remains well below replacement, with little immigration. The working-age population is contracting. As society ages, resources will be increasingly diverted toward healthcare and pensions, potentially crowding out investment in productivity-enhancing sectors.

China has made strides in artificial intelligence (AI). But it may not be a panacea for its looming productivity challenges. A higher share of China’s output is physically intensive and less exposed to automation, limiting the potential productivity gains from AI advancements. Agriculture, manufacturing and construction account for roughly half of employment in China, compared to less than one-fifth in America. Sectors more exposed to AI, such as financial and professional services, constitute less than 3% of all jobs in China.

China cannot count on AI alone to cure its economic malaise.

The real estate market, once a reliable pillar of growth and local government revenue, is mired in debt and oversupply. Defaults and restructurings among major developers, along with unfinished projects, have left homeowners in limbo. Despite targeted policy support, including rate cuts and relaxation of purchase restrictions, the real estate market is yet to show any clear signs of recovery. The property market downturn has dealt a significant blow to local governments. With land revenues drying up and deflation amplifying the real cost of debt, these governments are grappling with strained finances.

Despite a host of challenges, the broader financial system seems stable. Banks face rising asset quality risks from a weak property sector and indebted local governments, while profitability is squeezed by tighter margins and provisioning needs. At the same time, fiscal support is waning, reflected in slowing public spending. High total debt across government, corporates and households, which exceeds 300% of GDP, is limiting room for further stimulus.

Taken together, these challenges are complicating China’s efforts to sustain growth and transition to a more advanced, services-driven economy. A decisive reflationary shift will require deeper structural changes, that prioritize household confidence and income security. Just as Edison’s inventions sparked new industries, China will need to reinvent its growth model to power the next wave of economic prosperity, before it burns out.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.