Credit Markets Are Being Tested

Are loan defaults signaling a downturn?

By Carl Tannenbaum

People of my generation were expected to have a basic familiarity with automobile maintenance. At my peak, I was able to change spark plugs, filters, headlights, hoses and batteries.

Many of those components came from the Autolight line, which later became part of the First Brands Group. First Brands filed for bankruptcy late last month, training investor headlights on the credit markets.

Rumors surrounding the company had been swirling for months. As a private firm, First Brands was not subject to the same kind of reporting standards that public firms are. An auditor had certified its financial statements last spring, but apparently had not understood the layers of debt the company had taken on. At the end, there was a $2 billion hole in the firm’s balance sheet.

First Brands had tapped a wide range of financing sources. Its long-term borrowing has been packaged into securities that were sold to investors in the form of collateralized loan obligations (CLOs). It made liberal use of leveraged loans, secured by cash flows. The company used its accounts receivable as security for short-term cash needs. In the spring, it received a loan from a private credit fund.

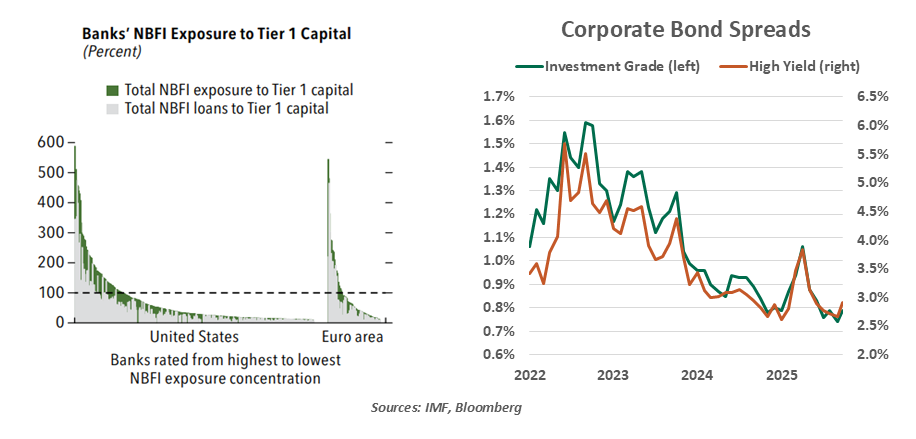

Concerns about private credit have resurfaced.

This diversity of debt is not at all unusual for private firms, but sustaining it relies on investors’ confidence in a company’s finances. While analysts have highlighted the idiosyncratic nature of the fall of First Brands, some investors have interpreted the event more broadly. Redemptions from funds containing the instruments employed by the company have accelerated in recent weeks.

We highlighted the issues surrounding private credit last year. The sector has grown rapidly over the past decade, thanks to attractive returns. Concerns center on light levels of regulation and reporting, which make it difficult to fully appreciate the risks involved. As often happens, questions are muted until adversity strikes. When it does, it provokes a powerful behavioral reaction, and contagion can ensue.

Credit extended directly by investors to corporations typically comes from funds or pools which are very well capitalized, and reasonably remote from the banking system. But in its October Financial Stability Report, the International Monetary Fund found that some banks have substantial exposure to non-bank financial institutions (NBFIs). It was these linkages that proved especially pernicious during the 2008 financial crisis, and which have been a focus of systemic concern ever since.

Global equity markets have surged this year, in spite of moderate economic growth and an accumulating series of risks. This has led some to worry that valuations have been stretched a little too far. The same can be said of credit markets, which have seen spreads fall to levels last seen in 2007. Credit spreads provide compensation for underlying risks; the First Brands debacle suggests that these may be underappreciated.

Losses related to First Brands have been widely felt. For now, contagion appears to be limited. But the system could certainly be tested again. JP Morgan Chase recently took a $170 million charge when a privately-held auto lender failed; the bank’s Chairman, Jamie Dimon, suggested that other problems might lie ahead. “When you see one cockroach there are probably more,” he observed. Bank earnings and call reports are under elevated scrutiny; at this time, loan defaults remain limited, not a hidden infestation.

Today, attempts to perform car maintenance are deterred by a cover that is fitted over the engine of many vehicles. The opacity of the lining makes it difficult to know what is going on under the hood. A similar sort of uncertainty is spreading through credit markets, and fixes may be difficult to apply.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.