- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

AI’s Long-Term Potential: More Upside Than Downside

AI’s long-term potential remains strong, but supply chain risks and uneven adoption may impact near-term gains.

KEY POINTS

What it is

A follow-up to the AI-Enabled Productivity theme from our 2025 Capital Market Assumptions report, exploring how AI’s promise is evolving amid demographic and geopolitical shifts.

Why it matters

Investors are watching how AI adoption could offset productivity headwinds, while supply chain risks and uneven global readiness may temper near-term impact.

Where it's going

AI’s long-term productivity potential remains asymmetrically skewed to the upside, but its impact will vary across regions and sectors depending on infrastructure, policy, and workforce dynamics.

As a follow-up to the AI-Enabled Productivity theme introduced in our February release of the 2025 Capital Market Assumptions (CMA), we’re taking a closer look at how this thesis is evolving.

Our original view suggested that the rapid advancement and adoption of AI could help offset productivity headwinds stemming from demographic shifts. While short-term implementation challenges persist, we remain confident in AI’s long-term potential to drive meaningful productivity gains. Recent market developments also warrant renewed attention.

Demographic challenges continue, exacerbated by changing immigration policies. At the same time, AI development is accelerating. For example, China’s announcement of DeepSeek R1 initially triggered a brief U.S. stock market dip, but the drawdown was short-lived, with competition viewed as a catalyst for innovation and faster AI progress.

AI is also being deployed in robotics (e.g., robotaxis, humanoid robotics)1 and agriculture, with China rolling out over 251,000 crop protection drones in 2024.2 These advancements could have a meaningful impact on food inflation and overall productivity.

We continue to view AI as having an asymmetrical profile — offering greater potential for upside than downside. However, concerns about job displacement remain. The timing and scale of AI’s productivity impact will vary across developed, emerging, and frontier economies, depending on each region’s technological readiness and workforce composition. Economies that embrace change may benefit from faster adoption and growth.

The Supply Chain Behind AI: Why Critical Minerals Matter

Trade tensions and concentrated mineral supply chains present strategic risks to AI scalability. China’s willingness to restrict critical mineral exports as a non-tariff trade barrier is increasing uncertainty in the global supply chain. For example, following tariffs imposed earlier this year, China’s exports of rare earth magnets dropped 74% in May compared to a year earlier — with exports to the U.S. falling 93%.3 These magnets are essential for graphic processing units (GPUs) used in AI model training and for small motors and actuators in robotics.

While the recently agreed U.S.-China trade framework aims to address these concerns,4 dependence on non-domestic sources means uncertainty will likely persist until supply diversification improves.

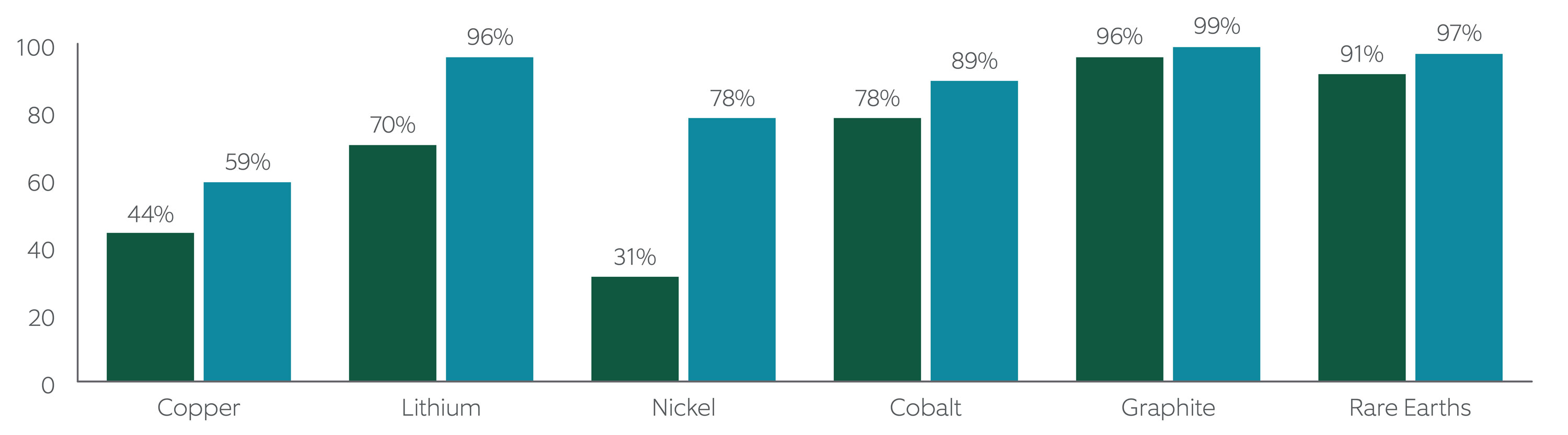

This issue was discussed at the latest G7 meeting in Kananaskis, Canada, where an action plan was agreed upon, though a near-term solution remains out of reach.5 China, Indonesia, and the Democratic Republic of the Congo, currently control 86% of the global refined critical minerals supply, up from 82% in 2020.6 About 90% of supply growth came from single-country sources — Indonesia for nickel, and China for cobalt, graphite, and rare earths.7 Exhibit 1 shows how China dominates in mineral refining.

Critical mineral supply also interacts with our other CMA themes: Navigating the Energy Transition relies on critical minerals for batteries and other technologies; and Globalization: Bent not Broken, explores trade, supply chains, and related risks and opportunities.

EXHIBIT 1: CHINA DOMINATES CRITICAL MINERAL REFINING

Percentage share of global refined material supply.

Source: Northern Trust Asset Management, Macrobond, U.S. Bureau of Economic Analysis (BEA). Q = quarter; GDP = Gross Domestic Product. Data as of 6/30/2025. Historical trends are not predictive of future results.

The Infrastructure Opportunity Behind AI’s Ascent

Infrastructure, both listed and private, remains a potential winner under our AI-enabled theme. Infrastructure has long been a favored option of global investors due to the sector’s high barriers to entry, inflation-linked cash flows, and equity-like returns with lower volatility. This theme, as well as Navigating the Energy Transition, further supports the case for infrastructure investment.

In the U.S., deregulation, the push for technological dominance (e.g., data centers, generative AI), and strong support for onshoring all act as tailwinds for the asset class. Today’s generative AI needs represent a game-changer for the utility and power-generation sectors. With many end-users seeking large-scale campuses, demand for power and data capacity is expected to remain robust. AI-driven data center power demand is projected to exceed 123 gigawatts by 2035 — a 30x increase from 2024.8 Utilities, midstream energy, and nuclear power are poised to benefit from growth in data centers, manufacturing, and electrification of the economy.

Outside the U.S., many countries are accelerating domestic infrastructure investments. For example, Germany announced the creation of a €500 billion infrastructure fund to support investments across energy, transport, and digital infrastructure. Globally, investments in AI-related data center capacity continue to grow, with one estimate putting it between US$3 trillion and US$8 trillion by 2030.9

AI’s Uneven Impact on Growth and Inflation

AI adoption has the potential to drive meaningful productivity and economic growth in countries able to capitalize on this theme. However, the magnitude of this impact remains difficult to project. Its potential is asymmetrical and skewed to the upside. For economies unable to leverage AI, economic growth may be more limited.

The effects on inflation are less clear. AI could lead to lower long-term inflation if it enables cheaper production and contributes to job displacement. More people competing for fewer jobs could lessen wage pressure, which may drive inflation lower.

AI, Energy, and Globalization: A Converging Investment Story

As AI drives up power demand, especially from data centers and generative AI, energy supply must keep pace. In the U.S., traditional sources like coal and petroleum are declining,10 while renewables face policy challenges. This growing demand is leading to the first major increase in the power load in a decade and prompting decisions to extend the lifespan of existing power plants.

A recent example is Meta’s 20-year deal with Constellation Energy to purchase energy from an Illinois nuclear power plant.11 Previously slated for decommissioning, the agreement extends the plant’s life by providing data centers more than 1100 megawatts of power.

As noted earlier, concerns about critical mineral availability and China’s use of critical minerals as potential non-tariff leverage in trade negotiations, also tie into Navigating the Energy Transition and Globalization: Bent not Broken CMA themes. These materials are essential for batteries and other energy infrastructure technology.

Special Considerations China’s Strategic Role in AI and Market Leadership

One of our “Special Considerations” in the 2025 CMA was China, specifically its economic size and trade influence. While that consideration focused on domestic consumption and internal stimulus, China remains relevant to the AI-Enabled Productivity theme through its role in trade, trade barriers, and competition for AI leadership. The U.S.’s ability to maintain AI innovation and leadership could also influence our Market Concentration topic in our CMA, particularly regarding continued U.S. stock dominance.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee