- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | May 15, 2026

Oil Prices Spill Over

All petroleum products may face disruption.

By Ryan Boyle

Nineteenth-century oil processing plants used simple, column distillation of crude oil to produce kerosene, which was in high demand for lighting lamps. The process also yielded a dangerously flammable byproduct called gasoline which had no obvious use. At best, it was thrown into furnaces for heat. Dumping petrol into waterways was common, until the internal combustion engine created a use for it.

Motor fuel is now the dominant petroleum product, and it has been the main source of inflation since the Iran War started. But not all of this is due to the price of oil. Further, a wide range of products derived from petroleum are under stress. An understanding of how oil goes from the well to consumers will help put recent developments into context.

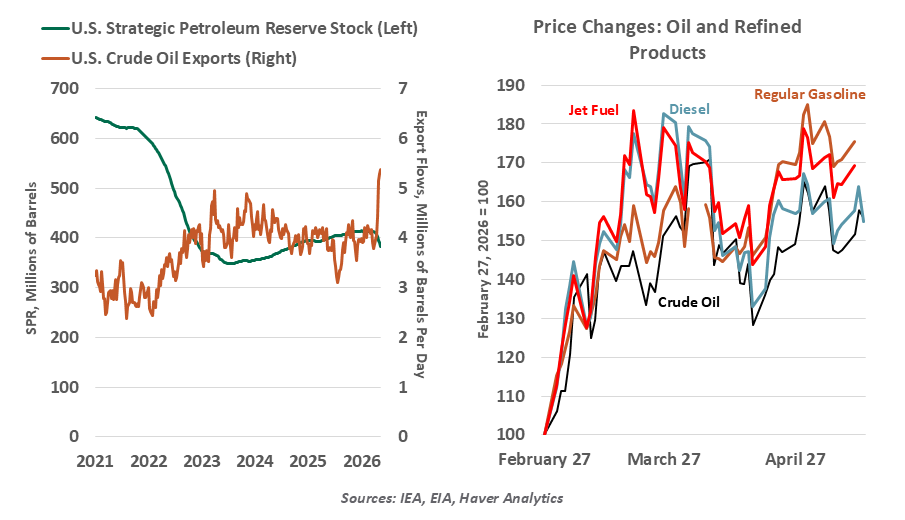

Given the extent and duration of the energy disruption, market observers have been surprised at the relatively limited change in oil prices during the Iran war. The shock has been tamed by two shifts: The U.S. has increased its exports of crude oil by about three million barrels per day, primarily from a drawdown in the strategic petroleum reserve. At the same time, China has reduced its volumes of oil imports by about five million barrels per day, also by relying on their domestic strategic reserves.

But reserves are finite and cannot temper prices indefinitely. As time goes on, nations may contemplate export controls. This will pinch countries which have no native supplies.

In its raw state, oil is virtually useless. It needs to be refined into fuel for various purposes. Refineries are massive chemical processing facilities. Building and tooling them is a significant, long-lived capital expenditure; some countries and communities are reluctant to host them. As a result, the global network of refineries is not ideally situated relative to sources of crude and demand for specific outputs.

Refineries are limited to processing certain types of oil into particular types of fuel. One illustration of this involves the U.S.: domestic refineries can process any type of crude, but they are optimized and thus more profitable refining heavier imported oil. Most crude oil extracted today in the U.S. is exported for refining elsewhere, and most oil refined in the U.S. is imported.

The Iran war has put the world’s fuel refining network under stress.

This could shift over time, but at a cost. While the U.S. is self-sufficient when it comes to oil, the same cannot be said for gasoline and other fuels. Domestic costs will depend on refining operations elsewhere.

Gasoline’s dominance means that it has the most robust supply networks and ample inventories. All other petroleum-based fuels have tighter inventories and are more susceptible to price fluctuations in a supply shock. As a result, the prices of diesel and jet fuel initially rose to greater extents than gasoline did as the war unfolded.

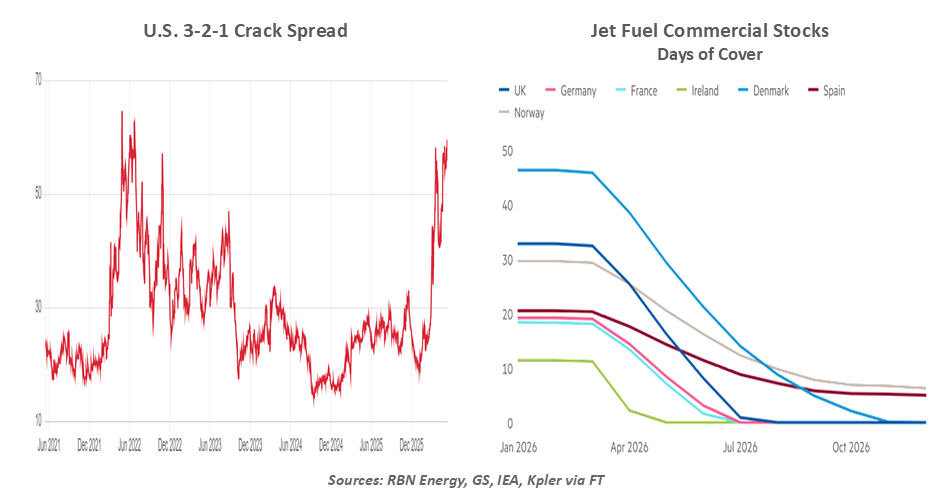

Oil refiners make their profit from the difference between the cost of their raw inputs and the price of their finished products, known as the crack spread. In rough proportions, three barrels of crude oil will yield about two barrels of gasoline, one barrel of distillates like diesel or jet fuel, and trace amounts of other chemicals (known as the 3-2-1 spread).

Since the Iran conflict began, the prices of final products have risen to a greater extent than crude oil has. The wider spread illustrates the extent of dislocations in the energy sector. We haven’t seen anything like this since the 2022 invasion of Ukraine.

Rising jet fuel prices, which have pressured air fares worldwide, offer a good case study. The geography of refining plays a critical role in this market. There is plenty of refining capacity in the United States, but much more limited capacity in Europe and Asia. Shortages and price pressures are much more severe in those locations.

For Europe, production of jet fuel has diminished considerably over time due to refinery closures and emissions regulations; the region had a structural shortfall of 500,000 barrels per day before the war began. Most of that gap was filled by imports from the Middle East, which has ample jet fuel refining capacity. But with the Strait of Hormuz still closed, Europe must seek other avenues.

The vulnerability of supply chains is once again on display.

The stress extends far beyond transportation fuels. Naphtha is a volatile byproduct of oil distillation that has found important uses. It is the primary feedstock used to produce ethylene, propylene and polyvinyl chloride, the chemical foundations of plastic products. Refineries that can create these polymers from raw naphtha are concentrated in the Middle East, led by Saudi Arabia, and are stuck due to the closure of the Strait of Hormuz.

Specialty petrochemicals are also used as inputs to some pharmaceuticals; delays in drug production and development are possible. Asphalt is a low-value residual byproduct that is easy to take for granted until it is scarce.

The pandemic disruptions taught us that global supply chains are delicate, and complications can compound. Fuel supply chains may be permanently altered by the current disruption. While they will take time to come online, additional capacity to refine and recycle petroleum derivatives will help. Investments in resilience will certainly not go to waste.

Related Articles

Meet Your Expert

Ryan Boyle

Chief U.S. Economist

Ryan James Boyle is the Chief U.S. Economist within the Global Risk Management division of Northern Trust. In this role, Ryan is responsible for briefing clients and partners on the economy and business conditions, supporting internal stress testing and capital allocation processes, and publishing economic commentaries.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.