- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Big Bill Promises Big Bills

OBBBA sets a path for more borrowing ahead.

By Ryan Boyle

The United States has a proud culture of going big. We take pride in our open spaces, large vehicles and bold ambitions. This year’s fiscal legislation follows the same mold, with the “One Big Beautiful Bill Act” (OBBBA) setting a trajectory of very big deficits.

Beauty is in the eye of the beholder, but the bill is certainly big, by necessity. The OBBBA is progressing through a reconciliation process, which allows passage with a simple majority in the Senate. The upside is that budget legislation can move more quickly, but the challenge is that the bill has to include a lot of legislative priorities. Among them are:

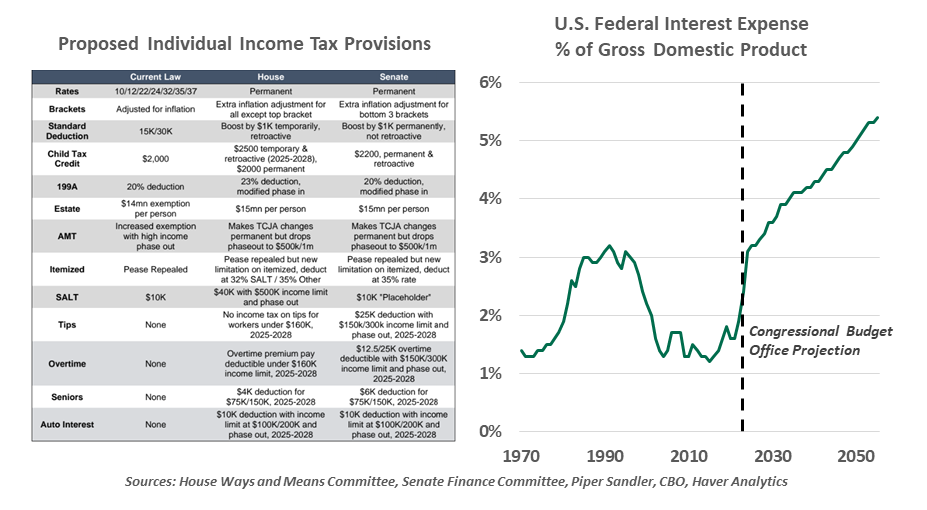

- Tax rates: The Tax Cuts and Jobs Act (TCJA) of 2017 was set to expire at the end of this year. For most taxpayers, especially businesses, that would have represented a tax hike in 2026. The OBBBA renews most provisions of the TCJA.

- Debt ceiling: As we mentioned in our money market discussion, the debt ceiling must be raised to keep the U.S. out of technical default in the coming months. The OBBBA would lift it by at least $4 trillion, sufficient to cover required borrowing.

- Other priorities: the OBBBA includes a series of Republican priorities like ending taxes on tips and overtime. Social Security income will still be taxed, but recipients will gain a higher standard deduction. Funding for border security will rise, while social supports and green initiatives will lose out.

The OBBBA passed the House of Representatives by a margin of a single vote. This week, the Senate debuted their vision of the bill. The two bills are functionally similar, with differences centering on the size of state and local tax deductions, the permanence of some business deductions and caps on Medicaid spending. Once the Senate finishes work, its version will have to be harmonized with the House edition.

The OBBBA is a missed opportunity to work on the deficit.

While the Republican party is aligned behind the direction of the bill, its details have brought about some mixed opinions. Those in the party who advocate for fiscal discipline have expressed disappointment in the borrowing that the budget will require. Some are advancing a case that the bill will unlock new growth and pay for itself, but those pledges are often too good to be true.

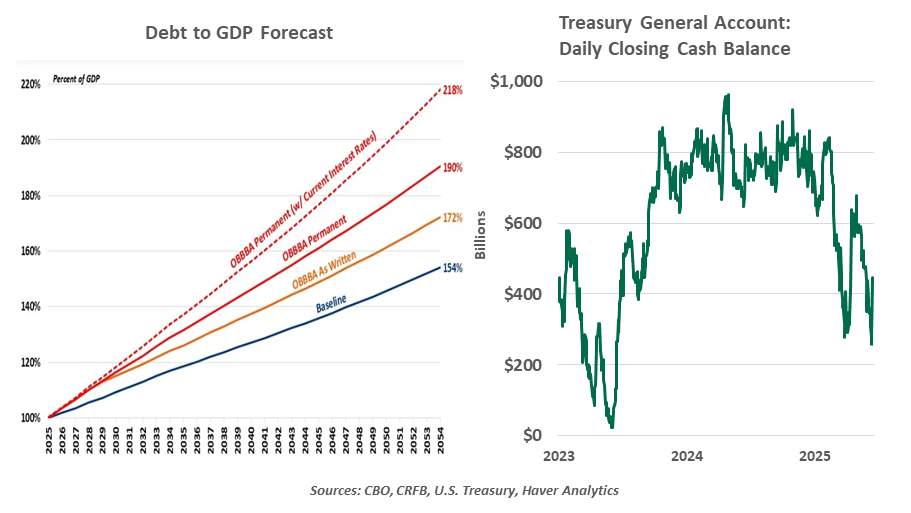

Fiscal concerns are legitimate. The United States runs a structural deficit. Congress routinely authorizes spending that substantially exceeds government revenue, with new debt issued to bridge the gap. Relentless borrowing is an easy point of criticism in election campaigns, but actually reducing the deficit was not a priority in the OBBBA. The Congressional Budget Office (CBO) estimated that, including additional interest, the House bill would increase deficits by $2.8 trillion over the next ten years.

The CBO analysis looks only at the parameters of the OBBBA, a view the bill’s supporters argue is incomplete. The second Trump administration led with tariff pronouncements, many of which have now gone into effect. Already, customs receipts are on the rise. Forecasting future receipts from tariffs will be difficult, but they will act as a partial offset to reductions in tax revenues. Nonetheless, those projected totals will still leave wider deficits ahead.

The OBBBA does propose a handful of tax increases. University endowments may face a tax of up to 21% (depending on their size) on their investment income, while private foundations may pay up to 10%, building on the 1.4% tax introduced in the TCJA. Business charitable contributions would only be deductible to the extent they exceed 1% of the corporation’s taxable income. Remittances (money transferred abroad, usually among family) would be newly taxed. And Section 899 would grant new taxation authority to address differences in international tax regimes.

Some tax credits are set to expire to meet deficit requirements.

A wider deficit can be worthwhile if it helps to unlock new economic activity that broadens the tax base. The OBBBA renews business investment tax credits and resumes immediate expensing of business investment in equipment and research. These business-friendly measures were the most economically impactful components of TCJA, and they can play an important role toward an agenda of reshoring and domestic production. In aggregate and accounting for the higher debt burden, the Yale Budget Lab estimates that the OBBBA would add only 0.2 percentage points to total economic growth for three years, and then become a long-term drag.

Some of the elements of the bill will come with an expiration date. The reconciliation process requires that the projected deficit in ten years is at the same level as it is currently. Annual deficits can widen in the intervening years, as long as they return to the starting point. The House version of the OBBBA sets expirations of many beneficial tax policies as soon as 2029. If these are ultimately extended, as past sunsets have been, projected deficits will rise even further.

We are tracking the risk of a bond market reaction to the national fiscal imbalance. The possibility is not theoretical: “bond vigilantes” sold their holdings in 1994 when U.S. government spending was viewed as too expansive and inflationary. More recently, an imbalanced budget in the U.K. in 2022 brought about a bond market rout and change in leadership. However, the bill that passed the House did not spark a selloff. The U.S. has gotten away with decades of fiscal imbalance; why should this time be different?

When struggling to take action, friends may encourage each other to “go big or go home.” Members of Congress appear to have taken this guidance, designing a budget that preserves big government and will require big borrowing. Passage may not be feasible before the July 4 target, but Congress will almost certainly go big before they go home for the summer.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.