Getting To Know Money Markets

Money markets are one place to see policy and economics in action.

By Ryan Boyle

Editor’s Note: The Northern Trust Economics team collaborates regularly with subject matter experts throughout the bank. We think you will appreciate hearing from them, too. This week, in the second installment of the series, we sit down with Dan LaRocco, Head of Liquidity within Northern Trust Asset Management (NTAM).

What is your role within NTAM?

I’m responsible for the team that manages our cash management vehicles, like money market mutual funds (MMMFs) and short term investment funds. Our assets under management currently exceed $300 billion.

Have you seen any signs that investors are changing their allocations to cash assets like MMMFs?

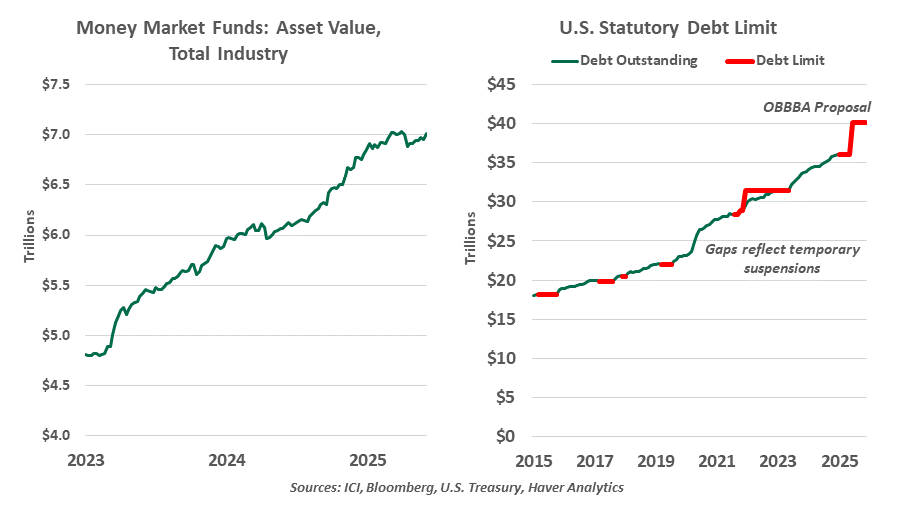

At the industry level, money market fund assets have been growing this year, but at a slower pace than the strong run up seen during the two years prior. Demand for cash has been steady, even during volatile intervals like the trade uncertainty in April of this year. Industry assets under management are holding near all-time high levels.

How do you approach the potential risk of the U.S. Treasury breaching the debt ceiling this summer? What could the consequences be, and what are the latest developments?

We’ve been through many debt ceiling episodes before, and we treat each as a risk management exercise. In addition to closely monitoring the news and the political environment, we deploy tools like position-size management, and we consider repositioning our portfolios. We monitor markets for disruptions in trading conditions.

Clients use cash management products with the expectation of safe, readily-available liquidity. We would not want to encounter the extreme tail-risk scenario of delayed repayment of principal and interest on certain US Treasury securities, or “technical default.” While the knock-on effects of such a scenario can’t be completely known, many market participants have taken measures to mitigate these potential tail risks after several recent debt ceiling incidents.

The debt ceiling is back in force, and we are again tracking technical default risks. The current episode differs from previous ones that have gone down to the wire, in that past incidents took place under divided government. Nonetheless, we’re monitoring the progress of the budget bill making its way through Congress, which includes an increase in the debt ceiling. The current projected “X-date,” when the Treasury would lack sufficient funds to make payments, is in August. Party leaders have set a goal of passing the budget by July 4th. We will welcome a resolution.

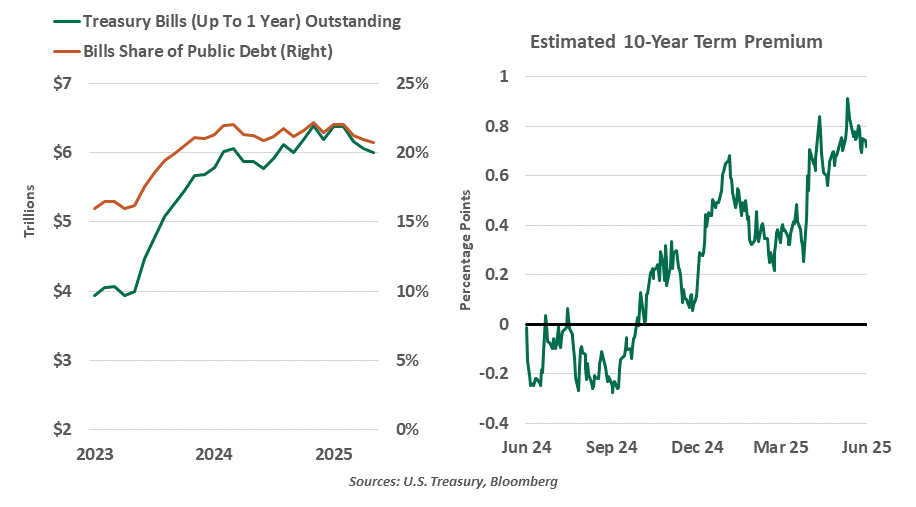

Treasury auctions results do not suggest a withdrawal of foreign buyers.

How have auction results been? Any sign of investor fatigue or shifting demand from foreign buyers?

We often participate in Treasury auctions and always watch the results closely. In April, a handful of Treasury auction results drew attention for their rumored lower participation by foreign buyers; however, we haven’t seen a widespread shift in demand across the curve in recent auctions. T-Bills (with durations less than one year), in particular, have seen solid demand as net supply is currently negative: short-duration bills are reaching maturity at a pace that exceeds issuance. Precisely determining foreign demand in real time is difficult, but on the whole, investor demand doesn’t appear to have shifted as definitively as some press reports suggest.

Have you seen any evidence U.S. debt expansion affecting term premia?

A term premium is the additional yield paid for locking in capital for longer durations. It’s not an explicit price, but can be derived by comparing the yields on longer and shorter tenors of the same instrument. By many measures, term premia have increased over the past nine months or so. We can only infer the cause. This could include concerns over fiscal expansion and related increased issuance of US Treasuries, but it’s difficult to separate that from general uncertainty about a number of policy changes that could impact U.S. Treasury yields and term premia.

Demand for safe, liquid assets is steady.

What do you expect will be the steady state of the Fed’s balance sheet? How have balance sheet expansion and contraction affected markets?

We don’t have a specific target size for the Fed’s balance sheet in mind, but we believe we’re closer to the end of balance sheet paydown (quantitative tightening, or QT) than the beginning. Indicators like usage of the Fed’s Reverse Repo Program have come down considerably. Other money market rates, like the Secured Overnight Funding Rate (SOFR), have drifted higher within the Fed Funds target range. As the Fed calibrates different assets and liabilities on its balance sheet, their primary objective is to implement monetary policy within orderly money markets. They would not want QT to be a cause of disorder.

Are there potential policy changes on the horizon that you’re watching?

U.S. sovereign debt trades in the world’s largest and deepest securities market, so we are tracking any policy tweaks around central clearing of US Treasuries. The Fed may change the design of the Standing Repo Facility, which could be important in the event of a liquidity shock. Potential changes to the Supplementary Leverage Ratio could improve demand for banks to hold Treasuries. And of course, we are watching the Fed very closely…just like many others!

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.