Treasury Tax Tension

Section 899 would raise the stakes of international tax disputes.

By Carl Tannenbaum

The draft of the One Big Beautiful Bill Act (OBBBA) runs more than 1,000 pages. Analysis of the legislation has focused primarily on its impact on the U.S. federal deficit: the Congressional Budget Office estimates that passage would add almost $3 trillion to the national debt over the coming decade. We’ll have a fulsome look on the economic consequences of the OBBBA later this month.

Specific measures within the bill are often narrowly focused, and have little impact on aggregate outcomes. We are usually content to leave analysis of those codicils to tax experts. But one component of the OBBBA has generated a great deal of international anxiety.

Section 899 of the legislation would authorize the White House to enact special taxes against individuals and corporations in countries that impose “unfair foreign taxes” on American firms. The U.S. Administration has vowed to reduce or eliminate overseas levies that it views as hindering domestic companies; section 899 would provide a weapon to use in this endeavor.

Countries raise revenue in very different ways. All use some combination of income, sales, and excise taxes, but the mix can vary considerably. Tax systems aren’t just for raising revenue; they can also be used to promote or discourage certain types of activity. And they have periodically been used to protect domestic providers from foreign competition.

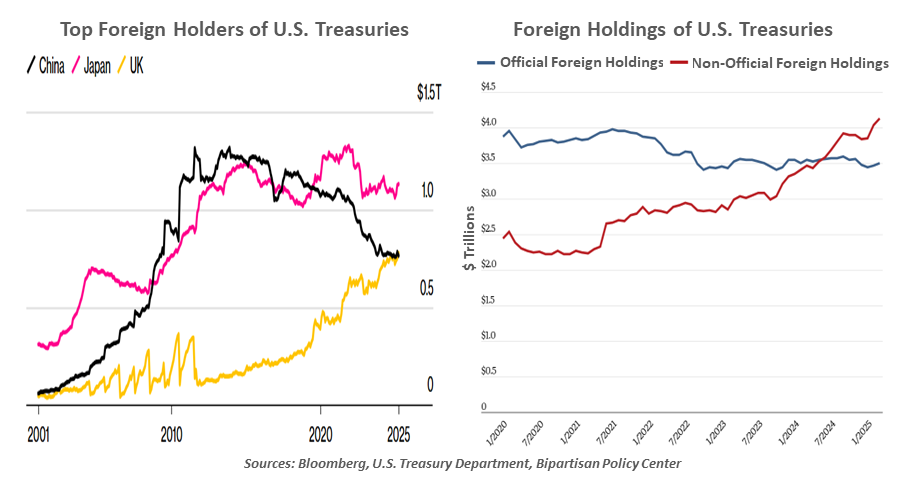

Placing additional taxes on foreign investors would be counterproductive.

One of the assessments that has drawn America’s ire is the digital services tax (DST) charged by the European Union and other countries. While the locus of a factory makes it is easy to determine the genesis of output, the origins of technology services are more difficult to pinpoint. In an effort to collect corporate taxes from digital firms, some countries apply a rate to revenues earned from users with local internet addresses.

The past several U.S. Administrations have found DSTs to be anti-competitive. U.S. firms are the predominant providers of digital services; local purveyors are typically exempt from the tax. Using revenue as a basis (as opposed to profit) is also seen as unfairly targeting offshore providers.

The DST is among the issues that the U.S. will want to address as part of trade negotiations with the European Union. If section 899 passes, it will almost be certainly be used as leverage in those discussions. The language allows the U.S. to raise taxes on income earned in the U.S. by companies operating in the relevant jurisdictions. The assessments start at 5%, but can escalate to 20% if the offending levies remain in place.

If this were merely a source of leverage in trade policy, it might have gone relatively unnoticed in high-level analysis of the OBBBA. But as written, it appears that the new tax could be applied to interest earned on U.S. securities owned by the targeted foreign entities. This would diminish the returns earned by overseas investors. Given the substantial role that foreigners play in financing the U.S. national debt, and the prospect that the debt will continue to increase, section 899 has been an unwelcome source of uncertainty.

Experts who have read the text generally agree that the intent is not to increase taxes on U.S. investments. But the language is ambiguous. As the U.S. Senate continues its discussion of the OBBBA, a clarification on this front would be very welcome.

As I wrote in the summary of my recent trip to Asia, international investors have increasing concerns about their exposure to U.S. assets. Few are making wholesale changes to their portfolios, but even incremental shifts could have important impacts on market performance. American policymakers should be doing everything they can to bolster confidence; the ambiguity surrounding section 899 is not helping to achieve this goal.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.