- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Economic Commentary | May 8, 2026

Japan Steps In On The Yen

The Bank of Japan keeps its currency value contained.

By Vaibhav Tandon

The Japanese yen has traditionally been viewed as a safe-haven currency, one that appreciates when global uncertainty rises. In recent years, however, that relationship has frayed. The currency has increasingly traded like a risk asset, weakening during episodes of stress rather than strengthening. The latest bout of volatility linked to the Middle East conflict underscores that shift.

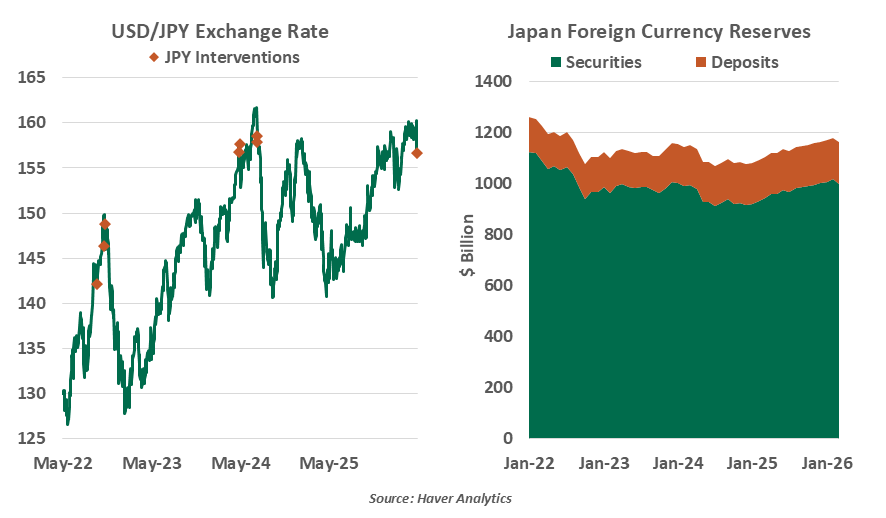

The yen has been under persistent downward pressure since March. Last week, it slid past ¥160 against the U.S. dollar, a threshold that has historically prompted official intervention.

Since then, the yen has rebounded sharply. The move was likely aided by intervention estimated at around ¥5.5 trillion ($35 billion) based on Bank of Japan data, just shy of the $37 billion deployed in July 2024. Yet, the broader downward bias may persist.

Policymakers will defend a floor, not target a rebound in the yen.

A weaker currency is typically supportive for Japan’s export-oriented economy. But the current episode has become a source of concern for policymakers, as the costs are increasingly visible. Japan’s heavy reliance on imported energy leaves it acutely exposed to external shocks. Higher oil prices raise the country’s import bill, increasing demand for dollars and putting further pressure on the yen. In this context, the currency’s slide reflects geopolitical dislocations more than traditional rate differentials, with Japanese bond yields already near three-decade highs.

Intervention remains a tool, but not an infinite one. Japan’s foreign currency reserves total about $1.2 trillion, of which roughly $162 billion is held in liquid deposits that can be deployed quickly. Policymakers can supplement this by offloading foreign securities, as seen a couple of years ago. That said, the scale and timing of any further intervention will depend on the pace of depreciation and market volatility. The objective is likely to center on preventing a disorderly move beyond ¥160 per dollar, rather than driving the yen toward a stronger target level.

Buying yen and selling dollars can only offer temporary relief unless the underlying economic drivers are addressed. Until those fundamentals shift, the currency may continue behaving less like a traditional safe haven and more like the risk asset it was once expected to hedge.

Related Articles

Meet Your Expert

Vaibhav Tandon

Chief International Economist

Vaibhav Tandon is the Chief International Economist within the Global Risk Management division of Northern Trust. In this role, Vaibhav briefs clients and colleagues on the economy and business conditions, supports internal stress testing and capital allocation processes, and publishes the bank’s formal economic viewpoint. He publishes weekly economic commentaries and monthly global outlooks.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.