- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Is There Value in the Value Premium? (Revisited)

By Steven Germani, CFA, CFP, Senior Investment Research Analyst, Wealth Management

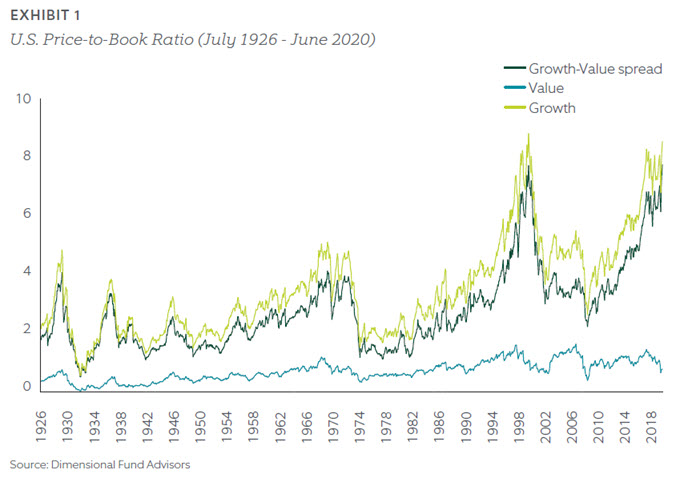

In January 2016 we published the research article "Is There Value in the Value Premium."At the time, value stocks (Russell 3000 Value index) had underperformed growth stocks (Russell 3000 Growth index) by 4.1% annualized since 2009, and investors were questioning whether a value tilt was beneficial to their portfolio. Fast forward to July of 2020 and the underperformance has fallen to 7.2%. The main academic research on the value premium uses the price-to-book ratio to sort value and growth stocks, though other value measures produce similar results. The value premium is the return of value stocks over the return of growth stocks, so an intuitive measure of potential “value” in the value premium is the spread in price-to-book ratios between growth and value stocks. Exhibit 1 shows the price-to-book ratio for both growth and value stocks, as well as the spread from July 1926 through June 2020.

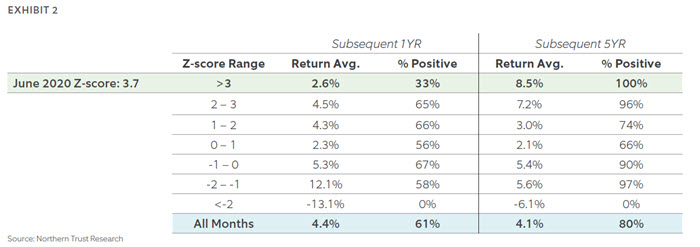

The spread hovers around levels not seen since the technology bubble of the late 1990s. The increased spread is fueled by a run-up in the valuation of growth stocks and to a lesser degree by the devaluation of value stocks. Market timing is unreliable, and we can’t know for sure when the value premium will turn positive or even if it will persist going forward. But we can put this in the context of history, which may be informative to forward-looking investors. We calculate a Z-score1 for the price-to-book ratio spread (number of standard deviations above the average spread) for every month back to July 1926. In Exhibit 2, for a range of Z-scores we display the average value premium and percentage of time the value premium was positive over subsequent one-year and five-year periods.

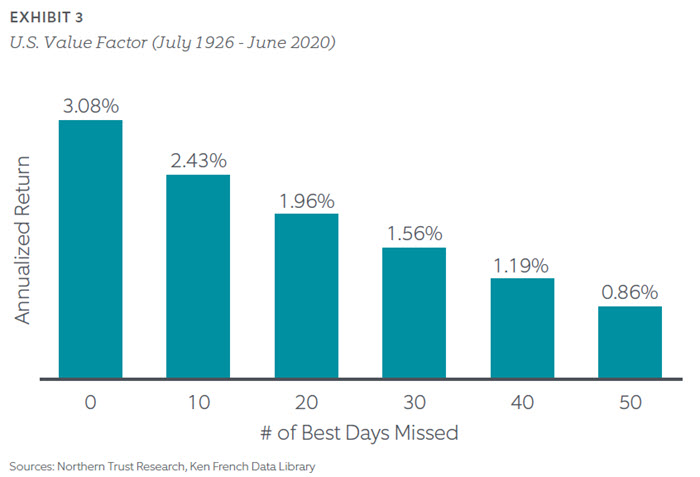

At the one-year horizon there is not much of a discernable pattern across the Z-score ranges. This reinforces the fact that short-term returns are noisy, valuations can stay extreme for a long time, and attempting to time the value factor is probably a useless endeavor. At the five-year horizon there is also not much of a pattern for the middle Z-score ranges, but we see stronger evidence at the extremes of the distribution. The Z-scores associated with the most extreme spreads have historically been associated with both the highest average 5-year subsequent value premium and the highest likelihood of a positive value premium. The current spread is in the extreme Z-score range. While history is no guarantee of future performance, this observation may inform confidence levels for long-term investors who seek additional return from a value tilt in their portfolio. Finally, Exhibit 3 displays the cost of trying to time the value premium historically.Missing just the best 30 days cuts the value premium in half over its 94-year history.

Factor-based investing requires a long-term view and the value premium is earned on average, but not every year. For investors already invested in a value-tilted equity strategy, it may be wise to stay the course. For investors who are considering implementing a value-tilted equity strategy, now is as good of a time as any to start.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S.

This document is a general communication being provided for informational and educational purposes only. The opinions and conclusions expressed herein are those of the authors and are not meant to be taken as investment advice or a recommendation for any specific investment product or strategy and does not take your financial situation, investment objective or risk tolerance into consideration. Performance examples are hypothetical and for illustration purposes only and actual results may be lower or higher than a portfolio that may be more or less diversified and/or managed in a different manner. In performing its services, Northern Trust will take into account other relevant facts and circumstances such that positions and transactions for any particular client account may differ with the investments described herein. Northern Trust provides fiduciary and investment management services to various types of accounts, including but not limited to, separately managed accounts, registered and unregistered funds. The investment advice given to one client account may differ from the investment advice given to another client account. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel.

All investments involve risk and can lose value. The market value and income from investments may fluctuate in amounts greater than the market. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.