EU Agrees To Reform Its Fiscal Architecture

EU nations have compromised on paths toward fiscal balance.

By Vaibhav Tandon

Maastricht is the birthplace of the European Union (EU). The treaty forming the Union was negotiated and signed there, following years of debate on increasing economic cooperation across the continent. In the more than three decades of the treaty’s existence, the bloc has grown in size and scope. However, the treaty’s fiscal limits—deficits of no more than 3% of gross domestic product (GDP) and government debt not exceeding 60% of GDP—had remained unchanged.

Government debts and deficits in Europe have soared in the aftermath of the pandemic and the Ukraine war. Members are facing rising borrowing costs due to higher interest rates and increased spending needs in areas like defense, digitalization, the green transition and old age support.

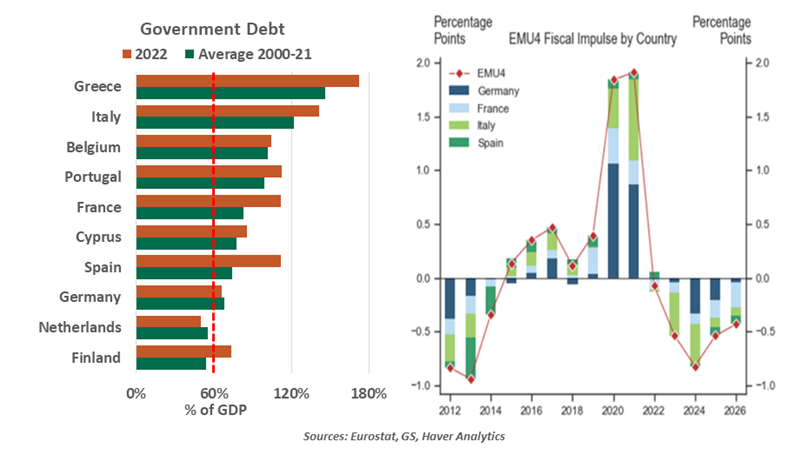

Debt in the common currency region remains elevated at around 90% of GDP, and in excess of 100% in Greece, Italy, France, Spain, Portugal and Belgium. Only nine of the 20 eurozone states have consistently had debt levels below 60% of GDP since the year 2000.

Reconsidering the bloc’s fiscal rules has been on the agenda for several years. But the persistent North-South divide within Europe hindered progress.

Late last year, however, European finance ministers finalized the long-awaited reform of the fiscal framework. Formal backing by national governments and EU lawmakers is likely to happen later this year. The new outline aims to give member states greater independence on agreeing to debt and deficit plans with EU authorities in Brussels. The main elements of the reform include:

- The two fiscal targets remain untouched: a 3% deficit limit and a 60% public debt to GDP ratio.

- Countries with debt ratios over 90% of GDP will be required to trim them by one percentage point per year over the duration of their national spending plan. That target is halved for states with debt ratios above 60% but below 90% of GDP.

- Member states breaching deficit rules will have to set a course of reducing their deficits by 0.5% of GDP each year. However, increased interest payments will be excluded from the calculation until 2027.

- The deal requires countries to keep deficits to around 1.5% of GDP, below the mandatory 3% deficit limit, to create room to increase spending during unexpected crises without breaching the original deficit threshold. Nations with deficits above 1.5% but below 3% will have to meet schedules for reducing them.

- States will be able to extend their fiscal adjustment period from four to seven years by following through on reforms that improve growth and support debt and deficit sustainability.

The new EU fiscal rules are complicated and may be difficult to enforce.

The flexibility offered by the new rules will limit the return of austerity, especially during tough economic times. The old rules prevented countercyclical growth-augmenting investments in areas like infrastructure, one of the key factors behind the economic under-performance of several EU members over the past decade. However, the reform falls short of the objective of simplification. Several exemptions and extensions to the pace of adjustment will make it difficult to enforce.

While the focus on budget restraint will comfort markets, it is also likely to weigh on growth at a time when the continent is fighting hard to avoid a recession. With the unwinding of energy-related support and the normalization of post-pandemic economic measures, the fiscal impulse in Europe is set to turn negative in the coming years.

The new fiscal framework agreed by the EU finance ministers is far from perfect, but still an important step forward. Pushing for the perfect might have been the enemy of the good.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.