- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

The Fed And The Ballot Box

The FOMC has enough factors to consider without adding politics to the mix.

By Ryan Boyle

Try as we might, we cannot ignore politics in election years. Campaigns creep into our lives through advertisements, yard signs, bumper stickers and casual conversation. The contagion has spread to our discussions of monetary policy: we are often asked whether the Fed will be influenced by the election. We believe not, based on a reading of history and the structure of the organization.

The Federal Open Market Committee (FOMC) is chartered to be apolitical. Seven of its 12 members are Governors of the Federal Reserve System, who serve staggered 14-year terms. While they are nominated by the President and approved by the Senate, their backgrounds are typically well outside the political sphere. The other five voting members are the presidents of the New York Fed and four other regional Federal Reserve Banks. Regional leaders are chosen by the boards of their local Reserve Banks, not through any electoral process.

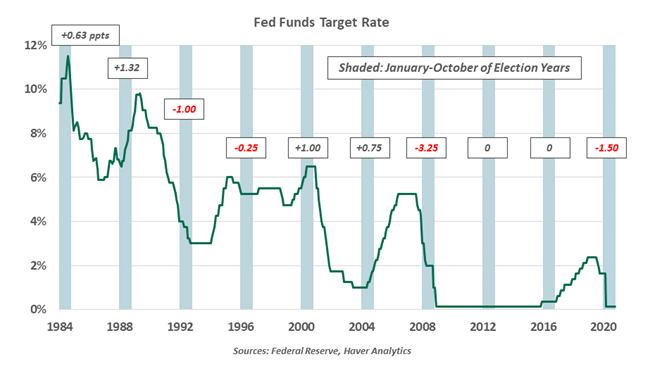

The Fed’s leaders do not live in isolation. A political lens could be applied to all decisions. But a review of the FOMC’s actions in the January-October interval of past election years reveals a pattern of decisions based on prevailing economic circumstances, no different from non-election years. The Fed’s practice of publishing a specific target rate only began in the 1980s, allowing a review of ten presidential election cycles.

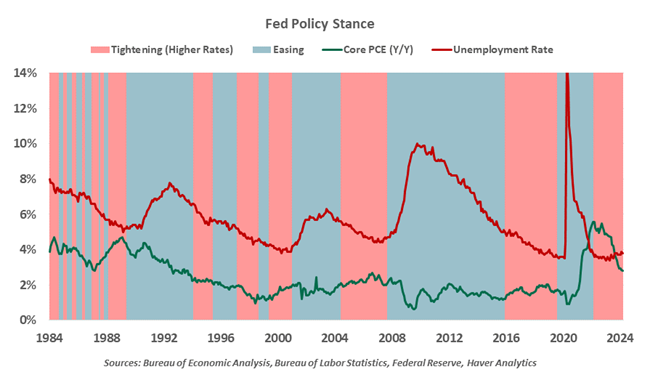

The Fed reacts to economic data, not polling data.

1980s: Finishing the Inflation Fight

The two elections of the 1980s came in the wake of the persistent inflation of the prior decade. The overnight rate stood at 10% as voters went to the polls in 1984, and 8.125% in 1988. Amid volatile rate movements, both years saw rates higher in October than where they started the year.

But higher interest rates were the norm at the time. The Fed did not arrest the growth cycle of the 1980s by hiking, nor did they do any harm to the incumbent. Ronald Reagan won reelection in 1984, and his party held power as his Vice President George H.W. Bush ascended in 1988.

1990s: Steady Growth, Steady Rates

Election-year rate adjustments in 1992, 1996 and 2000 were too minor in magnitude to be of electoral consequence. Leading up to the 1992 election, the Fed Funds Rate was cut from 4.0% to 3.0%, but that small stimulus did not secure Bush’s reelection. 1996 brought just one quarter-point hike early in the year, consistent with the stable economy that helped Bill Clinton win a second term. The leadup to the 2000 election included 100 basis points of hikes in February, March and May, as the Fed worked to cool the hot, tech-led economy. Core inflation had leaped from 1.4% in December 1999 to 1.9% in March 2000, meriting a policy response. Republicans narrowly returned to power in 2000 with the election of George W. Bush.

After 2000: Crisis Interventions and the Zero Lower Bound

The dot-com bubble was bursting as Bush took office. A cyclical recession in 2001 was unavoidable; the terrorist attack later that year cemented a difficult interval. The Fed eased in response, from 6.5% to a then-record low of 1.0%. The 2004 election year saw some movement toward normalizing, including a total of 75 basis points of hikes in June, August and September. Inflation was on the rise in the first half of the year as spending picked up. The tightening was consistent with an upturn in economic activity, working in Bush’s favor for reelection.

After hiking steadily back to 5.25% in summer 2006, the Fed enjoyed little respite before the housing market correction sparked a financial sector crisis. The FOMC started cutting in September 2007 and continued throughout the following year. The overnight rate stood at 1.0% as of the 2008 election, on its way to the zero lower bound. Deep recessions bode poorly for incumbent parties, with Democrat Barack Obama taking office.

The recovery was too sluggish to justify any tightening through Obama’s first term, with the unemployment rate stuck above 7%. The Fed attempted new interventions like quantitative easing, an afterthought in the 2012 election. The recovery strengthened in Obama’s second term, justifying one cautious hike in 2015, and then not again until the end of 2016.

The Fed’s long pause before the 2016 election had a whiff of political motivation, with Democrat Janet Yellen at the helm. However, the year was marked by fear of a recession stemming from a hard landing in China and persistently low inflation. As in 2000, a close election ended two-term Democratic control, with Republican Donald Trump taking charge. After modest hikes and cuts, the FOMC fell back to the zero lower bound in response to COVID. Monetary policy was the furthest thing from most voters’ minds in 2020.

Counter to popular perception, the Fed has often changed rates in election years.

The past ten cycles reveal two years of both hikes and cuts, four examples with cuts, two with holds and two with hikes. Rate decisions in election years have twice come as late as September, plus an emergency intervention in October 2008. The FOMC’s mandate revolves around inflation and employment, not elected leadership.

We understand the suspicion. The foregoing analysis starts after President Nixon inveighed on rates, contributing to the inflation of the 1970s. Subsequent presidents have mostly respected the Fed’s autonomy, and today’s Fed governors have steered well clear of political matters. Asked at this week’s press conference if the election raises the bar for a rate action, Chair Powell reiterated that “we’ll do what we think is the right thing, when we think it’s the right thing….If you go down that road, where do you stop?”

We must also challenge the premise that interest rate movements will sway the election. No cut before November would be a sign of economic strength, but also persistent inflation risk. A marginal reduction, while consistent with an optimal soft landing, would still leave rates much higher than they were at the start of Biden’s term. Rapid cuts would only accompany a crisis.

We will have more to say about key policy issues as the election draws nearer, but we do not expect the Fed’s independence to be one of them.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.