- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Inflation’s Signal and Noise

Skepticism is warranted when inflation stories exclude bad news.

By Ryan Boyle

Economic reports have had a strong, but frustrating start to the year. Consistent spending has sapped the momentum of inflation’s decline, while elevated job creation shows no need for policy support. Traders and forecasters (like us) have had to reconsider our expectations for rate cuts.

Frustrated by this, some have started digging through the details of the inflation reports and suggesting that we dismiss segments whose prices are rising unnaturally. We would caution against this practice.

When outcomes do not live up to our expectations, it is natural to seek root causes. The cost of shelter has been a key culprit in the United States. In the March consumer price index (CPI) report, shelter grew 5.6% year over year, while the overall index accelerated by only 3.5%. Excluding shelter, headline CPI has hovered between 0.8% and 2.3% for the past year.

Does this mean we should exclude or limit the influence of some shelter components on inflation? Defense for this notion comes from the fact that most U.S. households own their homes. Indices of rents or owners’ equivalent rent (OER) do not reflect actual mortgage payments, which are steady for most homeowners. From this perspective, it can be argued that official inflation measures are overstated.

Other approaches to measuring inflation, like the Harmonized Index of Consumer Prices used in many European nations, do not include OER. But inflation is not a tailored measure. Anyone shopping for homes or major purchases like autos has felt the effect of higher interest rates. Those are real economic headwinds.

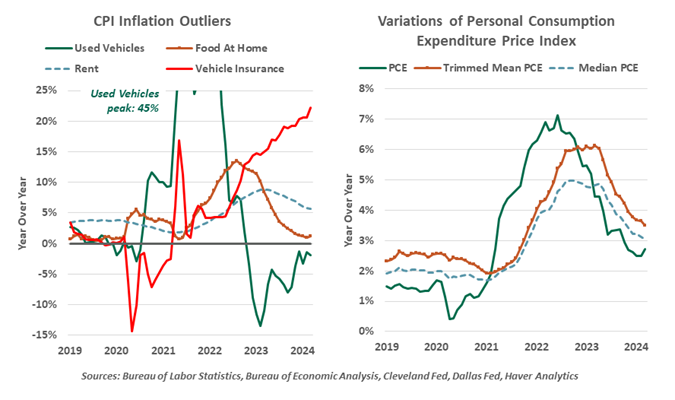

Readers may recognize the refrain of selective exclusion. As inflation took off in 2021, we could explain that the prices of used cars and trucks were skyrocketing due to automotive supply chain disruptions; excluding them, inflation was more tolerable. In 2022, commodity markets were skewed by the Ukraine war, and inflation was less problematic if categories like motor fuel were excluded. Today, we could get a calmer reading of prices if we ignore motor vehicle maintenance and insurance. There will always be categories of inflation that lead the pack. Inflation must be understood to include some hot and cold categories, not redefined to support a narrative.

Inflation measures are best understood as trends with a wide scope.

Established measures are available to handle the challenge of outliers. The Federal Reserve Bank of Cleveland publishes a median personal consumption expenditures (PCE) series, indexing to the price category that is the median of inflation rates each month. Their counterparts in Dallas publish a trimmed mean PCE, which excludes the categories with the highest and lowest inflation rates to present a more balanced picture. Both series did not surge like headline inflation rates did, but they also show more distance remaining for a full recovery.

Even the choice of measurement has drawn some scrutiny. CPI has an earlier publication schedule that garners more press coverage, but PCE is the subject of the Federal Reserve’s 2% year-over-year inflation target. The two measures are highly correlated in the long run, but when inflation rises, CPI tends to accelerate further and hold higher. Unlike CPI’s annual benchmark, PCE is re-weighted every month, making it more responsive to changes in consumer behavior due to inflation. As of March, the two core measures (excluding food and energy) are a full percentage point apart. They tell a consistent story of trending down, but not as quickly as we would like. Headline inflation of 2.7% for PCE in March sounds more palatable than 3.5% for CPI, but both are too high for comfort.

The Federal Open Market Committee (FOMC) will hold firm to its 2% PCE target. At the May FOMC press conference, Chair Powell made it clear: “Of course, we’re not satisfied with 3% inflation. ‘Three percent’ can’t be in a sentence with ‘satisfied.’” FOMC members have thus far done a good job rolling with the volatility of inflation, neither prematurely celebrating last year’s gains nor casting a more dour tone about this year’s shortfalls.

Media mogul Ted Turner once quipped, “If I only had more humility, I’d be perfect.” We can always find an attribute that’s lacking, or a point to exclude to improve our overall assessment. But the extremes still fit in the equation. With or without them, we see a trend of inflation coming down from an uncomfortable high, but with much more progress needed. The varying set of outliers remind us that inflation’s recovery will be uneven. After such a long stretch of stubborn inflation, we will maintain our own humility about forecasting it.

Related Articles

Read Past Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.