Tax Policy: A New Course Is Required

Tax cuts are popular but not affordable for most nations.

By Vaibhav Tandon

Frustrated voters sometimes ask how governments can run up debt so freely, when ordinary people need to live within their means. A key difference is that governments can tax their citizens when they need money, and borrow freely in public markets. While we caution against making analogies between household and government finances, the public sector needs to prioritize more revenue over more debt.

Nations in continental Europe learned this lesson the hard way during the sovereign debt crisis a decade ago, and the United Kingdom’s bond markets had quite a scare in 2022. American politicians haven’t faced this kind of stress, but they would do well to heed the lessons that these episodes offer as they consider tax policy.

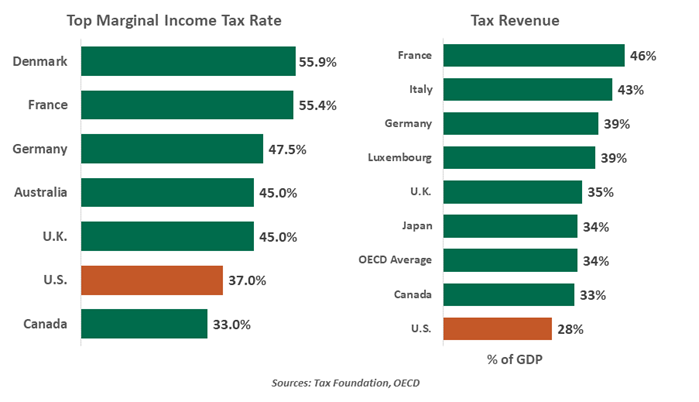

Corporate and personal taxes are key sources of revenues for governments of developed nations. There are large differences in tax levels and structures across countries, which reflect a range of political choices and administrative capabilities. On average, around half of the revenues in high-income nations comes from income and payroll taxes, one-fourth from value added taxes (VAT), 10% each from corporate income and other consumption taxes and the remainder from property taxes. The U.S. is the only major economy without VAT. Instead, it levies a sales tax, collected by state and local governments.

U.S. taxes are low relative to other advanced economies. The U.S. corporate income tax rate of 21% is below the global average of about 24%. The top personal income tax rate of 37% is also one of the lowest in the developed world. By contrast, the average statutory top personal income tax rate in major European countries is about 43%. The ratio of tax revenues to gross domestic product in the U.S. is 26%, the lowest among high-income economies.

There is no room for large-scale tax cuts in the U.S., nor in Europe.

In recent years, European governments have implemented a host of tax reforms. But given the already impoverished state of public finances across most of Europe, the policies were aimed at maintaining tax revenue levels while protecting consumers and firms from the post-pandemic cost of living crisis. These measures included temporary reductions in value-added taxes and excise duties, indexing the income tax to inflation and cutting tax rates for low-income families.

These programs were paid for by increasing taxes for higher-income groups through assessments on wealth and windfall profits. Similar measures have been contemplated by American Democrats during the current election campaign.

Proposed wealth taxes on financial assets are hard to implement, requiring global cooperation to prevent capital flight. We would need broad implementation of the proposed global minimum corporate tax deal to avoid losing revenue from that source to other jurisdictions. However, the future of the agreement still hangs in the balance.

Given the discontent surrounding tax increases, many governments have been content to accumulate mountains of debt. The costs of that strategy are burdening public finances and reducing the wealth of nations. Against this backdrop, the risk of potential revenue losses should be taken very seriously as tax policy is being contemplated.

A household in excessive debt can sell assets or, in the extreme, declare bankruptcy to find relief. Remedies for overindebted nations are not so straightforward, and default would burden societies in the extreme. No one likes taxes, but keeping them at a reasonable level will be essential to long-term fiscal health.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.