Hot Seat

APAC economies are at great risk from the U.S. reciprocal tariff plan.

Trade-dependent Asia-Pacific (APAC) economies are at great risk from the U.S. reciprocal tariff plan. After a three-month deferral, a new series of letters from the White House suggests that the levies will go into force on August 1. This will have a significant impact on the region’s economic fortunes.

Fourteen Asian nations are now facing similar tariff rates to those announced on “Liberation Day.” Asia’s trade links with China are also under the microscope as transshipments will be subject to additional penalties. The recently concluded trade deal with Vietnam and the threat to Japan suggest that the U.S. is not seeking complete free trade agreements; import duties are set to move up from their current levels.

Asian economies are starting to feel the pain from higher tariffs. Exports have pulled back, following strong front-loading to start the year. Unpredictable U.S. trade policy and heightened geopolitical tensions could end up rewriting Asia’s established export-driven growth model. Looser fiscal and monetary policies are the best bets for the region’s leaders to provide a floor to growth.

Following are our views on how major APAC markets are poised to perform.

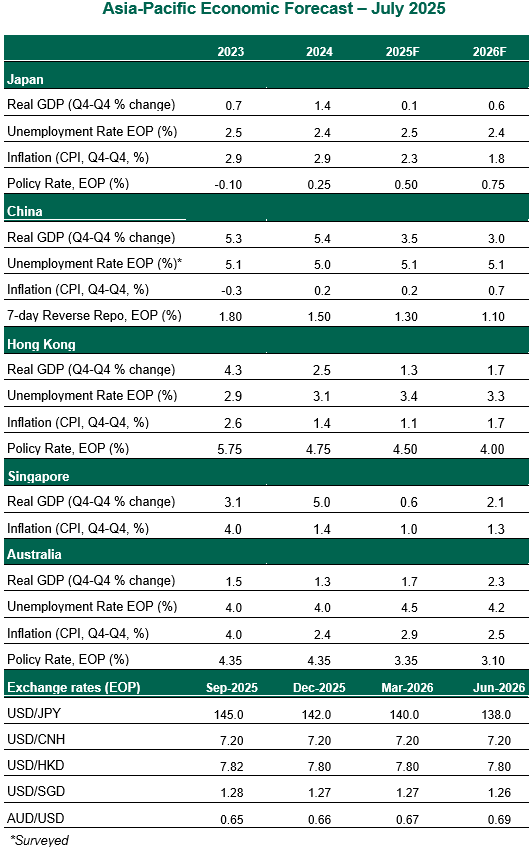

Japan

- Despite being a close U.S. ally, Japan is among the nations that are set to see a tariff rate increase on August 1. Trade negotiations have reached an impasse; Japan is seeking concessions for its important auto industry, and it is disinclined to open its politically-sensitive rice market to more American imports. Japanese exports are experiencing a decline, led by a drop in vehicle shipments to the U.S. The loss of a majority of the ruling coalition in the Upper House election could add to concerns about Japan's fiscal health and hamper the outcome of trade negotiations with the U.S.

- The Bank of Japan (BoJ) is in wait-and-see mode. The central bank kept its policy rate unchanged at 0.5% at its June meeting but announced its plan to slow down its reduction of Japanese government bond purchases in fiscal year 2026. Amid heightened uncertainty, weakening economic momentum will exert downward pressure on price increases, though wage increases will provide some support to domestic demand. We expect the BoJ to remain on the sidelines this year.

China

- Economic data was firm in the first half of the year, led by accelerated export orders and the continued boost from the consumer goods trade-in program. Amid external headwinds, the momentum is about to wane. Industrial production growth edged down in May, as the boost from front-loading faded. Exports rebounded in June, led by the reciprocal tariff pause in May. But continued decoupling and U.S. efforts to curb transshipments will spell trouble for China’s primary economic engine.

- Excess production capacity will add to deflationary pressures. Signs of slack are evident in the intensifying price competition in the Chinese auto industry and deepening producer price declines. Drag from the property market will persist, with recent data showing renewed weakness in the housing market. Home prices declined 0.3% month-on-month in June, the most in eight months.

- Policies to stimulate consumption and stabilize the labor market have gained traction. These have taken form of subsidies for durable goods, expansion of social safety nets and pension reforms. The urgency to pursue major reforms or large-scale stimulus has waned, given the rollback of sky-high U.S. tariffs. But further easing will be needed to beat deflation.

Singapore

- Economic momentum was fairly resilient in the first half of the year. The new U.S. import duties were silent on Singapore, raising optimism that the tariff rate will not exceed 10%. But for Singapore’s export-driven economy, even minor increases in global tariffs will have a significant bearing on its growth. The American focus on transshipment activities will deliver a big blow to Singapore’s vital re-exporting sector, which accounts for about two-thirds of total trade.

- Disinflation has continued, with the core measure decelerating to 0.6% year over year in May, well below the Monetary Authority of Singapore’s (MAS) soft target of “around 2%.” Most signs are pointing towards further disinflationary pressures, which would allow the MAS to loosen its policy settings again later this year. Higher reciprocal global tariffs, however, could prompt the central bank to ease as early as July.

Hong Kong

- Economic activity was robust in the first quarter. Growth was driven by notable upsurges in exports, as Hong Kong is a hub for rerouting goods between China and America. Improving inbound tourism also underpinned growth. That said, the outlook is bleak. Domestic demand is weak. Retail sales saw its first positive turn in May after 14 consecutive months of decline. The housing market is undergoing a severe correction, with home prices hovering at their lowest in nine years. Hong Kong is also paying the price for its ties to the Mainland economy. The Asian financial hub is subject to the same high tariff rate that the U.S. has applied to Beijing.

- Financial conditions have tightened recently, after the Hong Kong Monetary Authority's intervention to prop up the Hong Kong dollar, which had hit the weaker end of its trading band. Coupled with a patient U.S. Federal Reserve, this will hinder the recovery in domestic demand. Hong Kong’s growth prospects will be heavily influenced by aggressive U.S. trade tactics and cautious monetary policy.

Australia

- Australia’s economy has been in the slow lane since the start of the year. Government spending, the main engine of activity in 2024, was flat. Consumers remain frugal, with the labor market starting to show signs of softening. Sluggish productivity is impairing both income per capita and living standards. Australia is less susceptible to U.S. trade policy than many of its peers, facing only the 10% across-the-board levy. But the economy is far from untouched. For a trade-reliant economy like Australia, weaker global growth will filter through to the domestic economy via weaker exports and stalled business investment.

- The Reserve Bank of Australia (RBA) held its policy rate steady at its July meeting. The pause was more “about timing rather than direction” as the central bank decided to "wait for a little more information". With monetary policy still in restrictive territory and progress on disinflation on track, we expect the RBA to gradually lower its policy rate to 3.10%.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Related Content

Weekly Economic Commentary

Discover our latest insights on all economic news, from breaking headlines to long-term trends.

Learn More

The View From Here

Watch Carl explain the latest economic news in his own words.

Learn More

US Economic Outlook

Review our forecasts for selected economic indicators and interest rates and explore how they could affect future U.S. economic conditions.

Learn More

Global Economic Outlook

Explore the trends that will shape growth, employment, inflation and interest rates for major markets around the world.

Learn More

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.