- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

OPTIONS QUARTERLY COMMENTARY Q4 2024

U.S. equities maintained their positive momentum in Q4, rounding out a year of solid performance. Gains were driven by strong economic and earnings growth, interest rate cuts, and Trump’s victory in the U.S. presidential election. Investor optimism faded somewhat in December, due to inflationary concerns over Trump’s proposed tariff policies, whilst hawkish remarks at the December FOMC meeting triggered an equity selloff. The (SPX) ultimately closed at 5881.63 (+ 2.06% vs Q3 24) and (+23.3% vs 2024) and the CBOE Volatility Index (VIX) closed at 17.35 (+3.71% vs Q3 24).

Source: Bloomberg

An increased demand for hedging heading into the U.S. election meant SPX implied volatility was trading at a significant premium to realized volatility. During this time, the put- call ratio on the VIX index was at its highest level since 2020, and volatility skew reached a 99th percentile high. While NTSI saw a large amount of outright put and put spread buying for hedging purposes, some clients chose to take advantage of the elevated risk premium by selling volatility into the election. Following the fast and decisive election result, the S&P rallied due to investor optimism over the future growth of the U.S. economy under the Trump administration, with expected de-regulation and tax cuts.

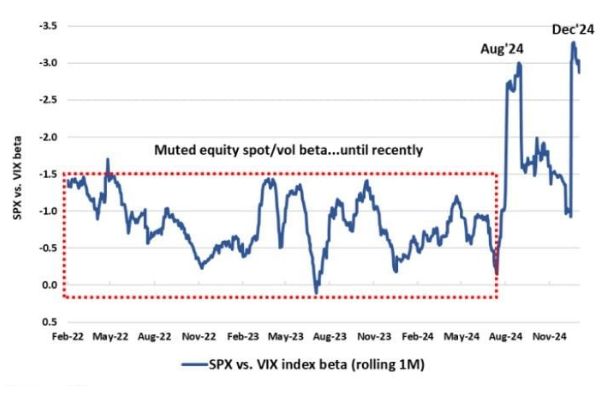

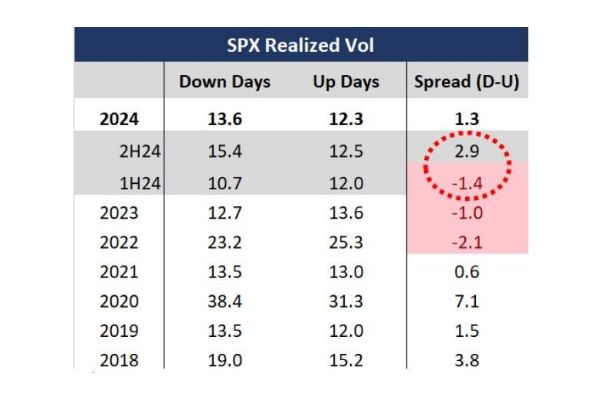

As a response to the Fed indicating they would dial back rate cuts in 2025 during the December 18th meeting, the VIX spiked by 74%, the second biggest percentage in history, closing at 27.6. According to CBOE, this spike was notable due to how much it outperformed the sell-off in the SPX index with equity spot/vol beta (the difference between realized and implied volatility) surging to a high of 3.3 as shown below, even higher than during the August 5th volatility shock. Following these notable volatility events, the CBOE has thus highlighted a potential shift in the equity volatility landscape. SPX skew has steepened because of options pricing in more downside risk as a result of higher realized volatility during market sell offs versus rallies. This marks a return to ‘normalcy’ from the unusual pattern we have seen the last 3 years, where on average higher realized volatility is seen on up days, the inverse of what has been true historically. We saw this pattern normalize in the second half of 2024, the first time since 2021.

Source: CBOE

Source: CBOE

Options Trends in 2024

We are continuing to see growth across the U.S. options market with an 8.6% increase in total option average daily volume (ADV) and a 34.4% increase in ADV of notional value of notional value (CBOE). Growth in options-based ETF strategies has also been notable, and according to JP Morgan they now amount to $140bn AUM, with call overwriting funds selling short dated calls contributing to around 60% of this total. Zero Day to Expiry options (0DTE) also continued to grow in popularity in 2024. For the first time, 0DTE SPX options surpassed all other expirations combined in Q4 averaging more than 1.5 million contracts, making up 51% of total SPX options volume (Bloomberg). Mandy Xu, CBOE’s head of derivatives market intelligence has attributed this growth to higher intraday volatility, an increase in macro catalysts, as well as an increase in retail investors trading index options.

Looking ahead to 2025

As we head into 2025, we can expect to see continued periods of volatility, particularly around the inauguration of Trump and further down the line, with uncertainty around proposed tariff policies. As noted by Bloomberg, the S&P 500 has only on two occasions returned between 5 -10% the year after an election since 1953, with extreme gains or losses more common. They also note that in the last 60+ years the S&P has only risen once when a Republican took over from a Democrat, which interestingly was during Trump’s first term.

Analysts at JP Morgan have predicted the VIX will trade on average in the teens expecting fundamental and technical factors to outweigh macro-economic risk. They note that U.S. volatility will be supply driven due to the prevalence of option selling ETFs and 0DTE strategies, further keeping volatility muted. That said, they expect vol of vol to be elevated, indicating we can perhaps expect to see an increased number of intraday vol spikes similar to the ones we witnessed in 2024.

Options involve risk and are not suitable for all investors. Call for a copy of the Options Clearing Corporation (“OCC”) Disclosure Document entitled "Characteristics and Risks of Standardized Options." Please read it carefully before investing.

Confidentiality Notice: This communication is confidential, may be privileged, and is meant only for the intended recipient. If you are not the intended recipient, please notify the sender as soon as possible. All materials contained in this presentation, including the description of Northern Trust, its systems, processes and pricing methodology, are proprietary information of Northern Trust. In consideration of acceptance of these materials, the recipient agrees that it will keep all such materials strictly confidential and that it will not, without the prior written consent of Northern Trust, distribute such materials or any part thereof to any person outside the recipient’s organization or to any individual within the recipient’s organization who is not directly involved in reviewing this presentation, unless required to do so by applicable law. If the recipient is a consultant acting on behalf of a third party client, the recipient may share such materials with its client if it includes a copy of these restrictions with such materials. In such event, the client agrees to comply with these restrictions in consideration of its accepting such materials.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 6th & 7th floor, Claude Debussylaan 16A-18A, 1082 MD Amsterdam, the Netherlands. Subject to regulation in the Netherlands by De Nederlandsche Bank and Autoriteit Financiële Markten. Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE NUF, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.