Hot And Sour

A period of slower growth and increased uncertainty lies ahead.

Hot and sour soup is a South Asian dish that delivers a distinctive blend of spiciness from chili peppers and acidic flavor from vinegar. U.S. officials have been dishing out a similar flavor profile, giving heartburn to many.

Constant threats are souring U.S. relations with its trading partners. Stop-gap deals of the kind agreed recently will not mark the end of the trade war, as the pacts leave high tariffs in place. Protectionism appears to be the U.S. administration’s preferred policy as it seeks to reshore industrial activity to the United States.

With trade in retreat, a period of slower growth and increased uncertainty lies ahead. America’s actions are a potential recipe for economic underperformance.

Following are our thoughts on how top markets are faring.

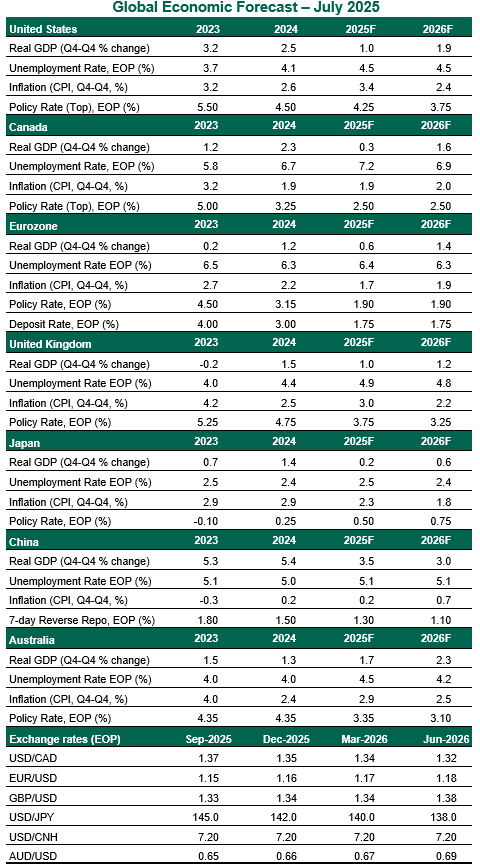

United States

- The U.S. economy is in an unsteady state: holding on to a soft landing, but also at risk of a downturn. Fundamental data is holding up well, as fears of policy-led inflation or job loss have not yet come to pass. The new fiscal bill averts the near-term prospect of a U.S. government default, but will compound long-term debt problems. As long as the worst uncertainty remains behind us, we believe the domestic economy will continue to grow.

- A balanced jobs market and sticky inflation justify the Federal Reserve’s patient posture. At its June meeting, the Fed left rates unchanged, but offered an outlook that reflected some differences of opinion. The median forecast called for two rate cuts before the end of the year, but a growing contingent expects no changes until 2026. Despite intense pressure from the White House, we believe that the Fed will reduce rates very slowly over the next year.

Canada

- President Trump has threatened to raise tariffs on Canadian goods to 35% on August 1. Reports suggest that the higher levy will only apply to goods not compliant with the United States-Mexico-Canada Agreement (USMCA), which are already tariffed at 25%. Therefore, the incremental duty will have only a limited additional impact on growth. With defense spending set to increase and a limited scope of tariffs, the Canadian economy may end up avoiding recession. But the risks are still very much tilted to the downside given Canada’s deep linkages with the U.S. economy.

- Firmer inflation and labor market data will prevent the Bank of Canada (BoC) from lowering interest rates at its July meeting. Canada’s retaliatory tariffs and the depreciation of the currency could keep inflation measures elevated in the near-term. Further on, the drag from reorientation of trade flows will force the BoC to prioritize supporting growth. We now expect one more cut of 25 basis points in October.

Eurozone

- The eurozone economy is on track for another quarter of positive but slower growth. While surveys and forward-looking indicators are turning more upbeat, hard data remain subdued. An expansionary German fiscal policy, increased defense spending by member states, and resilient labor markets will help boost the outlook; on the other hand, uncertainty around trade with the U.S. is suppressing spending by households and corporations. The U.S. and the European Union (EU) have reached a trade agreement, which imposes a 15% import duty on most EU goods. Though a full-blown transatlantic trade war has been averted, tariffs will remain much higher than they have been historically, impacting European exports.

- Inflation in the eurozone has slowed markedly in recent months and is on track to hold near 2%. Disinflation will continue, with sluggish growth, lower commodity prices and a stronger euro exerting downward pressure on consumer prices. This allowed the European Central Bank (ECB) to hold rates steady this month. With the risk of low inflation starting to surface again, coupled with spillovers from escalating trade tensions, we expect the ECB to cut in September and leave the door open to further easing.

United Kingdom

- The first quarter boost from stamp duty changes and front-loaded exports proved to be short-lived, as real GDP has declined for two months in a row. U.S. tariffs are not the sole culprit, as a raft of tax increases (such as the hike in employers’ National Insurance contributions) are weighing on spending. The government is being pressured to provide more stimulus, but fiscal headroom has tightened, with borrowing higher than was forecast. Tax increases are looking increasingly likely in the Autumn budget, which would further muddy the growth picture.

- The latest economic reports have not made the Bank of England’s (BoE) job any easier. A broad-based increase in both headline and core inflation in June makes a case to hold rates higher. On the other hand, labor market data supports the view that slack is emerging, and wage growth is cooling. The BoE is unlikely to pivot to a faster pace of easing this year.

Japan

- After months of negotiations, Japan and the U.S. struck a trade deal calling for 15% tariffs on all imports, including autos. While this represents a concession from the U.S., it will impair the competitiveness of Japanese exports. The nation’s fiscal health will remain a concern amid the ruling party’s loss of a majority in Japan’s Upper House. Economic growth is expected to slow to a crawl this year.

- The Bank of Japan (BoJ) is in wait-and-see mode. The central bank kept its policy rate unchanged at 0.5% at its June meeting, but announced a plan to slow down its reduction of Japanese government bond purchases in fiscal year 2026. Amid heightened uncertainty, weakening economic momentum will ease some price pressures. We expect the BoJ to remain on hold for the balance of this year.

China

- Economic data was firm in the first half of the year, led by accelerated export orders and the continued boost from a consumer goods trade-in program. Industrial production growth edged down in May, as the boost from front-loading faded. Exports rebounded in June, led by the reciprocal tariff pause in May. But amid external headwinds, the momentum is about to wane. The U.S. focus on curbing transshipments will spell trouble for China’s primary economic engine. While recent agreements have focused on de-escalation in areas like rare earth minerals and semiconductor chips, differing strategic interests will continue to hinder progress towards a comprehensive trade pact.

Excess production capacity will add to deflationary pressures. Signs of slack are evident in the intensifying price competition in the Chinese auto industry and deepening producer price declines. Drag from the property market will persist; house prices declined 0.3% month-on-month in June, the most in eight months.

- Policies to stimulate consumption and stabilize the labor market have gained traction. These have taken the form of subsidies for durable goods purchases, expansion of social safety nets and pension reforms. The urgency to pursue large-scale stimulus has waned, given the rollback of sky-high U.S. tariffs. But further measures will be needed to beat deflation.

Australia

- Australia’s economy has been in the slow lane since the start of the year. Government spending, the main engine of activity in 2024, has been flat in the year to date. Consumers remain frugal, with the labor market starting to show signs of softening. Sluggish productivity is impairing both income per capita and living standards. Australia is less susceptible to U.S. trade policy than many of its peers, facing only the 10% across-the-board levy. But for a trade-reliant nation like Australia, softer global growth will filter through to the domestic economy via weaker exports and stalled business investment.

- The Reserve Bank of Australia (RBA) held its policy rate steady at its July meeting. The pause was more “about timing rather than direction” as the central bank decided to “wait for a little more information.” With monetary policy still in restrictive territory and progress on disinflation on track, we expect the RBA to gradually lower its policy rate to 3.10%.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.