- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Weekly Investment Update: How U.S.-China Flare-Up Could Impact AI’s Advance

We examine the broader implications of China’s threat to expand restrictions on rare-earth exports.

KEY POINTS

What it is

We analyze, among other global political events last week, how China’s threat to further restrict exports of rare earths threatens the AI narrative.

Why It Matters

AI advancements and U.S. tariffs have driven stocks movement this year.

Where it's going

The flare-up creates more uncertainty for investors over the market outlook.

- Global equities fell more than 2% last week, with late-week drag from U.S.-China tensions.

- France and Japan continued to dominate political headlines outside the U.S.

- The U.S. government shutdown continues.

Despite gains in pockets of the market, including Japan and some U.S. technology stocks, broader global equity performance was negative last week. A late-week rise in U.S.-China trade tensions led to U.S. equities sliding more than 2% for the week, while non-U.S. equities were also in negative territory. Meanwhile, U.S. interest rates declined 5 to 10 basis points across the yield curve, with most of the move occurring Friday following a quieter stretch amid the U.S. government shutdown.

With the shutdown continuing, the U.S. economic calendar remained relatively quiet. Geopolitical-adjacent developments stepped in to help fill the void left by the lack of data. From a broader financial market lens, rising U.S.-China trade tensions overshadowed a substantial peace agreement between Israel and Hamas.

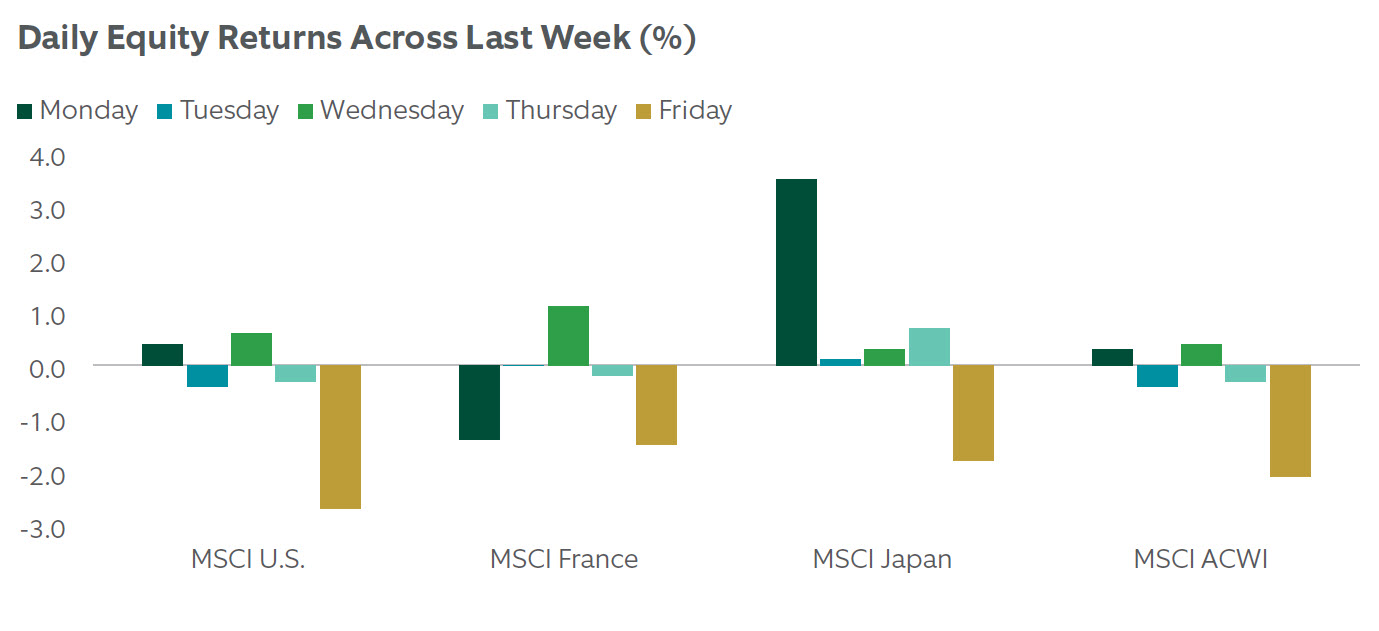

EXHIBIT 1: NOT A HAPPY FRIDAY FOR EQUITIES

U.S. equities led a Friday decline in global equities following a flareup in U.S.-China trade tensions.

Source: Northern Trust Asset Management, Bloomberg, MSCI. Data reflects week of 10/3/2025 through 10/10/2025. Country-level returns are in local currency; ACWI returns are in U.S. dollar terms. Note: ACWI represents All Country World Index.

After China threatened to materially widen the scope of rare-earth export restrictions, U.S. President Donald Trump responded with threats of additional large tariffs. U.S. equities dipped about 3% in response, marking the largest one-day decline for the S&P 500 since April.

Equity markets can often overreact to negative news, especially after a period of extended calm. These types of moves can have outsized short-term market impacts due to technical factors like crowded investor positioning. More broadly, the U.S. tariff threats highlight ongoing uncertainty around tariffs and U.S.-China relations, including broader economic impacts, ongoing legal challenges, and the potential for uneven sector-based impacts down the road. Financial markets are likely to remain attuned to U.S.-China headlines — even without material policy changes — as the issue spans both the broader macro backdrop and the artificial intelligence (AI) narrative. For instance, if China follows through on its rare-earth threats, it could materially restrict key components in semiconductor-related supply chains. This, in turn, could weigh on the AI adoption narrative and broader equity investor sentiment, given how central the AI-related theme has been to recent equity market gains. Overall, this remains more of a risk scenario in our view, but it’s something we are closely tracking. Outside the U.S., domestic political developments continued to draw attention throughout the week. Similar to early September, France and Japan once again shared the spotlight. Though different in many respects, both countries face political challenges in managing fiscal policy amid elevated debt levels and rising long-end government bond yields — without a strong governing majority for the parties in power.

With France on its fifth prime minister in two years, the political situation remains quite uncertain with the 2026 budget a near-term priority. The legislature remains divided across three major camps, with growing fiscal and debt-related concerns from the investor community. While French equities have performed well in 2025 alongside the rest of Europe, the political headwinds have been more impactful in the bond market. The spread of France’s 10-year government bond yield over Germany’s is near 10-year highs (roughly 80 basis points). Plus, the France 10-year yield is now roughly in line with Italy’s, despite typically trading more than 100 basis points lower over the last decade.

Meanwhile, Japan’s political uncertainty has declined but only modestly with possible re-acceleration on the horizon. Financial markets responded to Sanae Takaichi’s surprise win in the Oct. 4 leadership election of the Liberal Democratic Party (LDP), positioning her to become the country’s first female prime minister. The result led to initial equity gains, yen weakening, and steepening of the yield curve. Takaichi favors looser fiscal policy and targeted investment in key industries (defense, technology, etc.). However, enacting her policy priorities remains challenging, as the LDP lacks an outright majority in either house of parliament, meaning Takaichi will have to work with opposition parties to assume the prime minister role and pass legislation. This issue intensified after late-week news that Komeito, a smaller party and longtime LDP ally, announced it would leave the coalition with the LDP. Entering the prime minister seat will be even tougher for Takaichi in the near term, with heightened focus ahead of U.S. President Trump’s upcoming Japan visit in late October. By the end of the week, Japan equities were up more than 2% in local currency terms, the yen weakened about 2.5% against the U.S. dollar, and interest rates edged higher.

What to Watch for This Week

In response to China’s newly announced export controls, President Trump cast doubt about proceeding with a planned meeting with President Xi in the coming weeks and later announced a 100% additional China tariff on Friday night. Financial markets will assess the risk of a further rise in U.S.-China tensions in the near future, with a few key implementation-related deadlines set for early November.

The U.S. government shutdown continues, adding to the list of delayed economic data releases, such as September inflation and retail sales data. Third-quarter earnings season begins on Tuesday, with the usual cohort of large banks scheduled to release earnings, including JPMorgan (JPM), Citigroup (C), and Wells Fargo (WFC). Earnings expectations for the third quarter have been relatively stable over the past three months, with upward revisions in tech-related sectors and financials helping offset negative revisions in most other sectors. This differs from the traditional pattern of downward revisions (a few percentage points in the months leading into earnings season) followed by upside surprises when the companies actually report earnings. According to consensus expectations, aggregate earnings growth of about 8% year-over-year is expected for the S&P 500. Key earnings season watchpoints include AI-related demand and investment plans, as well as tariff-related impacts. Outside the U.S., the global economic data calendar is light, with inflation reports from Europe and China. France and Japan political-related developments will likely remain in the headlines.

Key Tactical Calls

Tilt to equities and real assets. We maintain a preference for equities and real assets over fixed income, expressed through tactical overweights to global equities and listed infrastructure. Within fixed income, we prefer high yield over more duration-sensitive segments of the market.

Earnings resilience. Easier monetary policy and fiscal stimulus help reduce downside economic risk, and global corporate earnings continue to grow.

Cautiously constructive. While our baseline is constructive, key downside risks we’re watching include a pronounced labor market downturn, sticky inflation, and a sustained breakout in yields.

Source: Bloomberg for data, news developments and schedule of economic releases. Data as of Oct. 10, 2025.

Meet Your Expert

Peter Wilke

Senior Vice President – Head of Tactical Asset Allocation

As the head of tactical asset allocation (TAA) at Northern Trust Asset Management, Peter is responsible for the research and development of innovative investment strategies for the firm’s TAA initiatives. Previously, Peter worked at Wellington Management, where he was the team leader of the multi-asset income investment boutique in Boston. His group was responsible for developing and managing multi-asset portfolios.

IMPORTANT INFORMATION

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited, issued in the European Economic Association (“EEA”) by Northern Trust Fund Managers (Ireland) Limited, issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. This information may not be edited, altered, revised, paraphrased, or otherwise modified without the prior written permission of NTAM. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For U.S. NTI prospects or clients, please refer to Part 2a of the Form ADV or consult an NTI representative for additional information on fees.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Not FDIC insured | May lose value | No bank guarantee