Brighter Picture

Clearer policy and lower rates are favorable for growth.

Volatile policy has overshadowed the outlook for the U.S. in the year to date. Now, as we enter the final stretch of 2025, some of the clouds are parting. Tariffs rates have reached a steady state. Risk assets have been buoyant, and financial conditions are easy. The summer fiscal bill created incentives for business investment which may soon bear fruit. The resumption of the rate-cutting cycle will support the growth outlook.

However, the array of risks remains wide and significant. Tariffs act as a significant tax increase that will weigh on margins, lift prices and diminish spending. Tariff-driven inflation is poised to be a chronic malady rather than a passing shock. A weakening dollar will further erode purchasing power, though it could add to the momentum supporting domestic production.

We believe resiliency and adaptability are core competencies of the U.S. economy. We have the resources to grow through uncertainty, whatever form it may take.

Following are our thoughts on the U.S. economy.

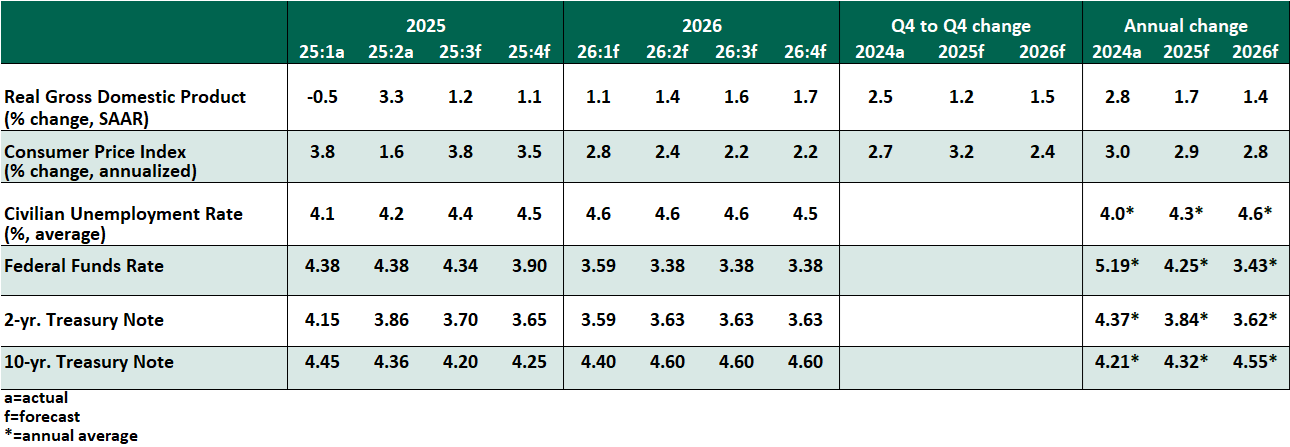

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- The labor market has taken the spotlight, with two consecutive reports of disappointing job gains. The August establishment survey found only 22,000 jobs were added, with most sectors showing losses on the month. The unemployment rate remains well-behaved at 4.3%, but job prospects for young and minority workers are showing greater strain. A preview of the annual benchmark revision, to be finalized next January, showed even weaker growth than had been estimated in the year through March 2025.

Tighter immigration means the break-even rate of job growth is likely lower this year than in recent cycles. Subdued gains may be the new norm.

- The soft labor market offered sufficient justification for the Federal Open Market Committee (FOMC) to reduce the overnight rate by 25 basis points after a nine-month pause. The statement emphasized the slower employment outlook and shifting balance of risks. The quarterly Summary of Economic Projections showed the median FOMC member expects two more cuts this year, with moderate easing to follow in 2026.

We expect cuts at the next two meetings, and one more next year; any additional action would require a weaker labor market than we anticipate..

In his press conference, Chair Powell declined to address many questions related to political pressure on the Federal Reserve. We do not view ideological influence as a near-term risk; the data support a return to a more accommodative stance. The downsides of a less independent central bank will be higher inflation in the long run and difficulty responding to future crises.

- Inflation remains stuck. The August measure of the consumer price index (CPI) showed prices grew 2.9% on the year, or 3.1% on a core basis (excluding food and energy). The price index on personal consumption expenditures was similarly elevated at 2.6% headline and 2.9% core, holding above the Fed’s 2.0% target. Inflationary effects of tariffs on imported goods have been limited thus far, tempered by large inventory accumulation at the start of the year and sellers absorbing some tariff costs into their margins. Services are also showing firm inflation, which cannot be tidily explained as a tariff effect.

Stable import price indices suggest that exporters have not made price concessions, while some reheating of producer price indices shows that tariff costs are stuck in the supply chain. We expect the costs to be passed on to final prices gradually in the quarters to come.

- Fears of the end of American exceptionalism were overstated. Demand for U.S. Treasuries remains strong; on days with mixed economic data, they are bid up as a safe haven, keeping yields in check. We believe the yield curve will steepen as markets price in the high and rising level of U.S. debt, but not immediately.

- The housing market is cooling. Though U.S. house prices do continue to appreciate in aggregate, the S&P CoreLogic Case-Schiller Index found that seven regional markets were in contraction in June, led by Tampa, San Francisco and Dallas. Lower interest rates may help to bring more buyers into the market to halt these declines.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.