Sprint To Stroll

The sprint phase is giving way to a more measured pace.

After an extended period of surprisingly resilient economic activity, marked by buoyant consumer spending and robust labor market gains, the U.S. economy is shifting gears. The sprint phase, characterized by fiscal tailwinds and pent-up demand, is giving way to a more measured pace. The cumulative effects of restrictive monetary policy, a softening jobs market and trade disruptions are becoming more apparent.

The economy enters the final quarter of 2025 navigating a complex landscape. Renewed trade tensions with China and the ongoing government shutdown have compounded uncertainty at a time when momentum is already slowing.

The outlook calls for below-potential expansion, not contraction. Strolling may lack the adrenaline of the sprint, but it is more stable and sustainable.

Following are our thoughts on the U.S. economy.

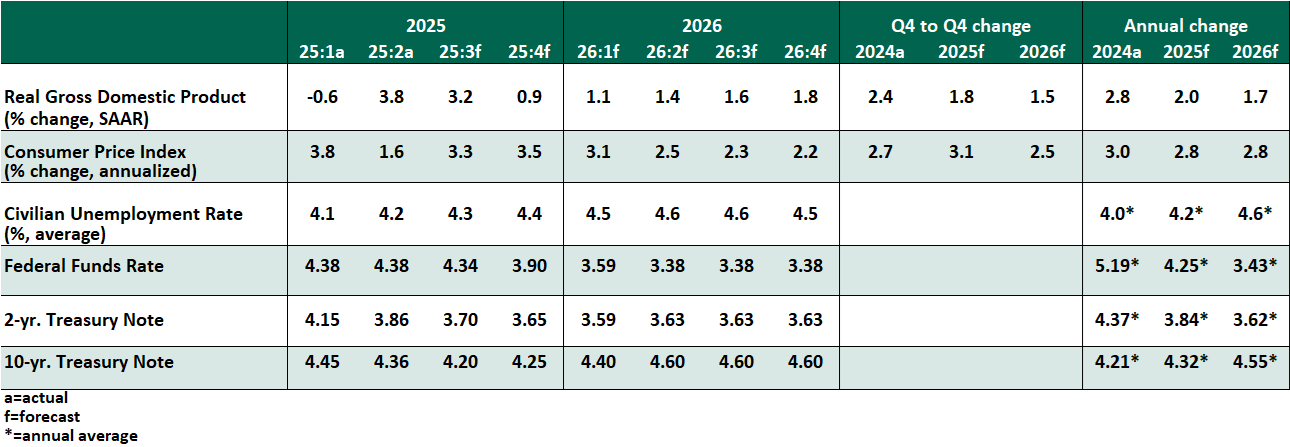

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- Real gross domestic product (GDP) growth has been volatile this year: a modest contraction in first quarter, followed by catch-up growth in the subsequent quarter and a likely strong performance in the third. This mid-year strength reflects payback after first quarter’s decline, which was driven by swings in imports and inventories. Robust consumer spending and an AI-led investment boom have also been drivers of activity.

But a step down lies ahead. The labor market is softening, and households’ real disposable incomes will be squeezed by rising prices. Discretionary spending has softened this year, with low job availability weighing on sentiment. A growing divergence in spending patterns is also set to dampen aggregate demand, amplifying the slowdown. While tax cuts and lower interest rates should help spending recover gradually into 2026, growth is expected to remain below potential.

- The U.S. government shutdown drags on, leaving federal agencies unfunded, key services disrupted and critical economic data releases suspended. Republicans and Democrats remain at odds over spending priorities and healthcare provisions, raising the risk that the impasse could stretch beyond October. The longer it lasts, the greater the macroeconomic toll. Prior shutdowns shaved up to 0.2 percentage points from annualized real GDP growth in that quarter.

- With official jobs data suspended, the ADP National Employment Report became the primary signal this month. It showed private-sector employment fell by 32,000 jobs in September, the largest decline since March 2023. The soft reading underscored slowing momentum. The labor market remains a key downside risk. Joblessness is gradually edging up while the trend of job growth is falling. That said, tighter immigration will restrain worker supply, limiting the rise in the headline unemployment rate.

- The September consumer price index (CPI) report has been delayed, but it is expected to release ahead of the Fed’s upcoming meeting. It will not alter the central bank’s stance. Tariff-driven inflation has been modest thus far, and the Federal Open Market Committee will look through a temporary rise in goods prices. Cooling employment conditions will cap domestic price pressures.

In a recent speech, Chair Powell signaled support for further cuts as the job market softens. Powell also indicated balance sheet runoff will stop “in the months ahead,” signaling that liquidity will not be a constraint to growth. We continue to expect two more cuts this year and one next year, with additional action only if the labor market weakens further.

- Trade tensions and tariffs are once again dominating headlines. In retaliation to China’s recent restrictions on rare earth exports, the U.S. has threatened additional tariffs of up to 100% on Chinese imports, which would push levies back to April levels of around 130%. This, coupled with sectoral tariffs, will distort price signals, disrupt supply chains and introduce uncertainty into investment planning all over again. With inflationary pressures potentially reignited by higher costs, the Fed may be forced to reconsider its current focus on labor market dynamics.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.