China Tries To Curb Competition

Excess capacity leads to excessive competition.

By Carl Tannenbaum

I learned a new English word this week. What made the experience more interesting is that the Chinese taught it to me.

The Oxford dictionary defines “involution” as the process of complicating things. China has extended this term (“neijuan,” or 内卷 in Mandarin) to describe needless competition within its economy. The Central Committee has vowed to root out involution and eliminate it wherever possible, but the effort misses the forest for the trees.

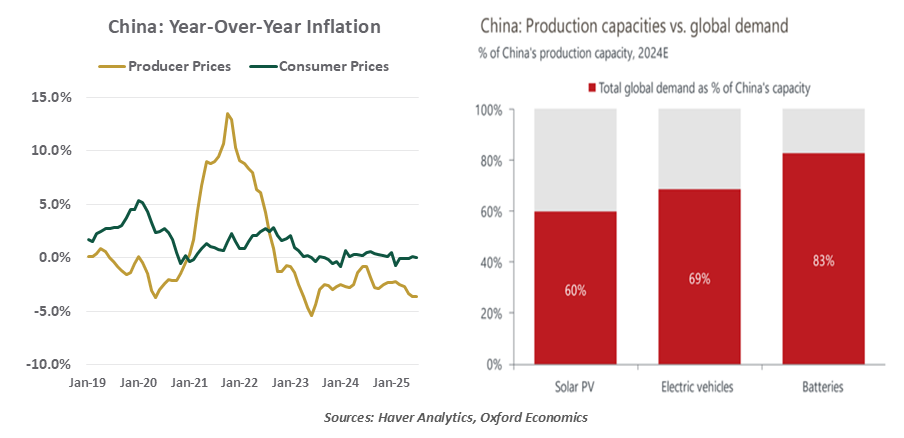

China continues to struggle with deflation. Producer prices have been falling for more than two years, and consumer prices have been essentially flat over that time. The stability of the consumer price index raises questions of potential steering of the data; posting declines in that series might contribute to a deflationary mindset that would be difficult to dislodge.

One of the main drivers pushing China towards deflation is an excess of supply. In a range of industries, China has capacity to produce much more than global demand. With trade restrictions rising and trading partners taking a dim view of product dumping (selling below cost), avenues to absorb output are narrowing.

Reducing internal competition will still leave China with considerable overcapacity.

China’s problem with overcapacity isn’t just in the aggregate. In many industries, there are quite a few domestic competitors who are fighting for market share. This drives prices down even further, raising the issue of involution. To remedy the situation, Chinese authorities are encouraging consolidation within sectors, and offering capital to help with the transition.

A basic example of involution centers on food delivery. Visitors to China inevitably come across armies of scooters clustered around eateries, vying to ferry dinner to hungry households. Online and on the streets, the major players are very aggressive, driving down prices and profits. The government has moved to curb the cutthroat competition.

On a larger scale, China produces an oversupply of the equipment that is utilized in generating clean energy. China has a dominant position in the production of solar panels, components for wind turbines, and the batteries needed to store power generated by both of them. Over the past two years, however, the momentum behind “green tech” has been diminished by policy shifts in the United States and elsewhere. Analysts estimate that 30% of Chinese companies in this sector are “zombies,” meaning that their interest payments exceed their revenue.

Ultimately, however, putting a floor under prices will require reducing overall capacity. This will be an exceptionally difficult thing to do. Shutting down factories or reducing their running hours will reduce revenue and could create credit issues for a wider community of firms. It would also risk a rise in unemployment, which would further diminish demand. Chinese provinces are reliant on local producers for employment and tax revenue, and may be reluctant to see them closed in the national interest.

One other way to deal with excess capacity in green tech would be for China to accelerate the modernization of its own energy infrastructure with a government-sponsored effort. That would have the ancillary benefit of improving China’s environmental reputation, but it might replace one glut with another: demand for power in China has diminished, as factories have slowed.

Ultimately, winning the battle against deflation will require boosting demand. Household spending in China represents less than 40% of gross domestic product (GDP), as compared to more than 50% for the eurozone and more than 65% for the United States. This gap has grown recently, as Chinese households seek to rebuild savings in the wake of the real estate crash. Eurasia Group, a geopolitical consulting firm, estimates that housing accounted for 75% of household wealth prior to the pandemic; home prices have fallen by more than 10% since then, and will likely decline further.

China will hold its next major economic policy meeting in October. If it is serious about arresting deflation, leaders will have to come up with a new word to describe stimulus.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.