Weekly Economic Commentary | November 14, 2025

Europe's Problem Children

France and Germany will set the direction for their region.

By Vaibhav Tandon

Growing up, my brother and I were branded the family’s “problem children.” We were loud, restless, and constantly testing our elders’ patience. Over time, we both wrestled with those traits in our own ways and found discipline. Ultimately, what defined us wasn’t the chaos we caused, but the resilience we showed in rising above it.

Europe’s economic family has its own “problem children.” The biggest siblings, Germany and France, are grappling with similar troubles: sluggish growth, structural rigidities, and political constraints. Like my brother and I, they bear a heavy weight of expectation. Their challenges may differ, but the struggle is familiar.

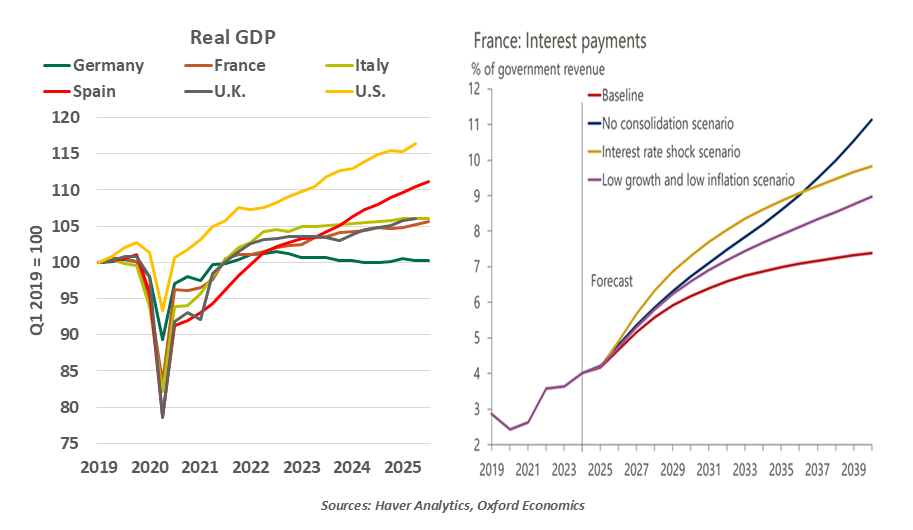

Since 2019, Germany has endured a prolonged period of stagnation. While the U.S. economy expanded by 13% over that interval and the eurozone overall has advanced by 5%, Germany’s output has remained virtually unchanged. Its industrial base, once the envy of the world, is faltering. The vital auto industry is losing its edge amid increasing global competition, particularly from China. Chinese automakers, backed by state subsidies, have boosted their presence in Europe with affordable, tech-driven models, eroding Germany’s engineering advantage.

Between 2017 and 2023, passenger car production in Germany declined by over 25%. High energy costs and bureaucratic hurdles have pushed some leading German companies to shift production abroad. Sluggish productivity and elevated labor costs, higher than peers like Spain, are undermining industrial competitiveness.

The eurozone faces headwinds as its two largest economies stumble.

Although Germany has loosened its fiscal brake, its frugal stance remains a problem. Public investment has been inadequate, accounting for 2.8% of gross domestic product (GDP), below the European Union (EU) average of 3.6%. Banks are still the primary sources of capital, and their conservativism has hindered risk-taking. Lower venture capital availability compared to countries like the U.S. has stifled innovation, making it harder for start-ups to scale or compete globally.

France, meanwhile, is muddling through its own low growth trap. Similar to Germany, structural factors like weak productivity gains and rigid labor laws have weighed on activity. But high deficits, political instability and frequent strikes are even bigger problems undermining the French economy.

France is among Europe’s biggest spenders relative to its economic output. It allocates nearly one-third of its GDP to social security, the second highest in the EU and far greater than the U.S. rate of a little over 20%. Persistent political turmoil has rattled investor confidence, driving up borrowing costs. Debt servicing is already among the largest items in the French budget, surpassing most departments except education and defense.

The recently-announced rollback of pension reforms has only worsened the fiscal outlook for France, pushing borrowing costs to historical highs. With weak potential growth, France's debt dynamics are set to deteriorate further.

Germany, with room to spend and still a robust export base, has levers to navigate the slowdown. France, by contrast, faces a tougher battle to restore fiscal health. If trends persist, France risks becoming the eurozone’s new weak link.

Together, Germany and France account for close to 40% of the eurozone’s GDP. They anchor regional stability, but their struggles raise a pressing question: where will growth come from? Investor confidence in the bloc often hinges on these two economies. Weakness in both could weigh on investment, push up risk premiums, and even pressure the euro’s exchange rate.

Just as my brother and I learned to leave chaos behind, Germany and France need to find their own balance. Letting go of old habits won’t just steady them but will help steer the broader eurozone forward. Their struggles won’t define them; how they respond will.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.