Fed Balance Sheet: Leveling Off

The flood of liquidity has receded.

By Ryan Boyle

We were gripped by last week’s news of an old-fashioned heist at the Louvre. Despite world-class security, thieves dressed as museum workers made off with eight priceless historical artifacts. Detectives are searching frantically to determine where the goods have gone.

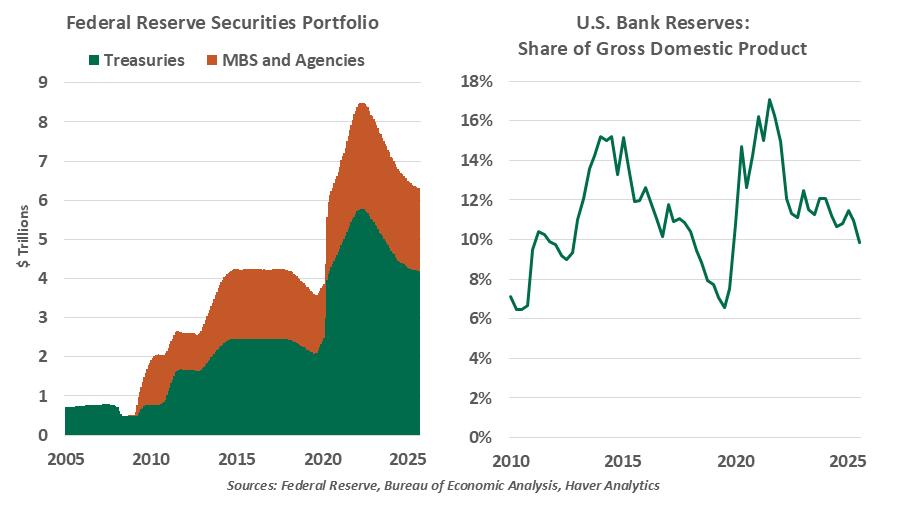

A different sort of disappearing act has played out in plain sight for the past three years. Over $2.2 trillion dollars have gone missing from the Federal Reserve’s balance sheet. Though the rundown has been quiet, it was no heist: the pace was well communicated. Now, an end is in sight, with the Fed’s balance sheet approaching a steady state.

Central bank purchases of securities in a crisis, or quantitative easing (QE), are still a relatively new tactic. They were first widely deployed in the Global Financial Crisis, then again in the pandemic. The first recourse in a crisis is to cut interest rates, but when rates hit zero, asset purchases offer an alternative form of support. When investors are reeling, the purchases can be a powerful intervention to backstop fixed income markets. QE maintains liquidity and encourages investors to stay in the markets for riskier assets.

Crises eventually subside, and then the central bank is left holding a large quantity of assets. Once conditions are stable, they begin depleting those assets through quantitative tightening (QT). Under QT, when a bond held by the central bank reaches maturity, its principal is not reinvested. The balance sheet entry is deleted, and the total portfolio value declines. Money is not physically destroyed, but the overall liquidity in the financial system is reduced.

Whereas the emergency intervention of QE is stimulative, the impact of QT is hard to observe. Amid a crisis, policymakers may err on the side of doing too much, creating more liquidity than the system needs. While those excess funds are evaporating, financial conditions show little change. And thus, two trillion dollars can disappear without consequence.

Asset purchases allow the Fed to support markets when interest rates can’t go any lower.

Last week, Fed Chair Jerome Powell gave a speech on the balance sheet. While not offering a specific plan for ending QT, the content of the speech made it clear that the Board is working on an approach to be announced soon. Powell recapped the pandemic-era QE and did not back down from addressing its critics. Perhaps QE could have ended sooner, but the Fed did not want to spark volatility in a vulnerable economy. Perhaps the Fed did not need to purchase over $1.3 trillion of mortgage-backed securities (MBS), but those were allowable assets to acquire as the Fed sought to keep financial conditions easy.

Powell’s key takeaway from the pandemic QE and QT was that the Fed “can be more nimble in our use of the balance sheet.” Bond markets are now familiar with this tool and can adapt quickly to the Fed’s strategies.

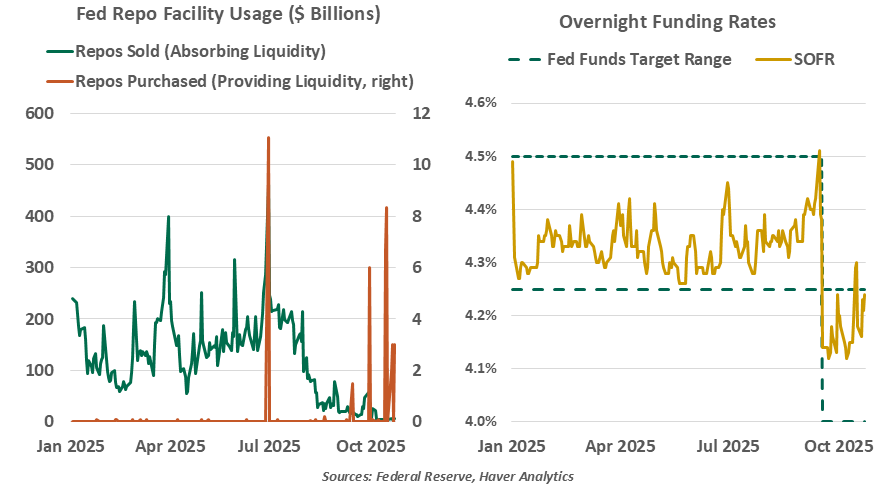

The Fed has remained cautious about the timing and announcements of its QT decisions: first, when to start as to not upset markets, and later, when to cease runoff. The Fed has only one prior interval to QT to study, and that episode went too far. On September 17, 2019, as GFC-era assets were in gradual runoff, interbank lending reached an unexpected shortfall. The Secured Overnight Funding Rate (SOFR), reflecting market pricing for overnight lending, spiked by nearly three percentage points. The Fed rapidly switched from QT to QE, and SOFR calmed.

To prevent recurrence, the Fed launched the standing repurchase facility (SRF) to allow quick borrowing. If funding markets are tight and overnight rates are rising, the SRF allows banks to pledge their U.S. Treasury assets to borrow directly from the Fed, at the top end of the Fed Funds target range.

The timing of Powell’s speech was driven by daily market observations. Strain is evident, suggesting the time is right to stop draining liquidity.

The Fed’s overnight reverse repurchase (ONRRP) facility was a pandemic workhorse. As savings rose, excess cash flowed into money market funds, who could earn a safe return placing these monies with the Fed each day. ONRRP utilization thus provided a ready measure of excess liquidity, exceeding $2.3 trillion in September 2022. Now, the ONRRP is holding near zero.

Draws on the SRF have increased, suggesting some overnight funding gaps have emerged. Similarly, banks can draw upon the Fed’s discount window to borrow directly; its usage has come back to life from zero in recent weeks.

Reserves in the U.S. banking system have gone from abundant to ample.

These shifts are not signs of stress; shortfalls have been minor, and relief systems are working as intended. However, we can be certain the era of excess liquidity has ended. Fed speakers have characterized the pandemic-stimulated economy as one of “abundant reserves,” with bank reserves elevated beyond their natural level. The Fed is targeting an environment of “ample reserves.” The boundary between “abundant” and “ample” has never been defined. However, the 2019 shock is illustrative. Bank reserves as a share of nominal gross domestic product had trended down from 15% to a low of 6.5% when markets seized. The Fed is unlikely to go that low again. The decline to roughly below 10% today is likely consistent with “ample” reserves.

And while he left this point unstated, Chair Powell may view the balance sheet as the last piece of unfinished business from the pandemic crisis, to be resolved before his term ends next May. Leaving the balance sheet in a steady state will make it more difficult for any successor to change its use, until another crisis opens this path again.

In an upcoming meeting, we expect the Federal Open Market Committee to announce a new strategy that will set a steady state for the balance sheet. And with that, the years-long case of the missing trillions will close.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.