Goods Trade: Delayed Aggravation

Expect to see supply gaps in the months ahead.

By Ryan Boyle

Traveling last month, I connected through SEATAC Airport. On approach, the aircraft circled over the Port of Tacoma. The cargo-oriented facility is a sight to behold: massive cranes, artificial waterways and railroad tracks were all evidence of high-end logistics.

One sight was missing, though: I spotted no container ships in the harbor. My observation from 10,000 feet was consistent with facts on the ground. Imports from China are collapsing, and America is going to pay for that very soon.

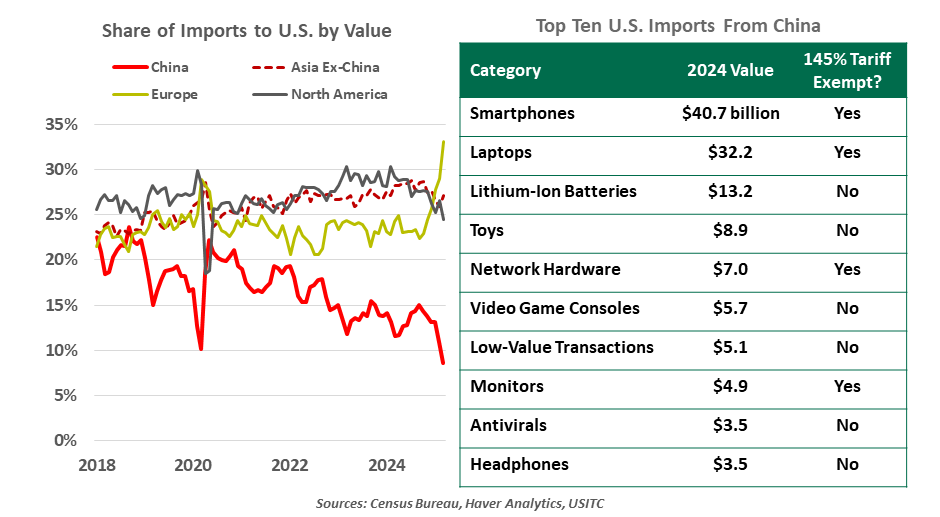

China has been a focal point of American trade policy for many years, but tensions were escalated early in the second Trump term. New 20% incremental tariffs were announced against China, Canada and Mexico in response to narcotic and immigration flows; only the latter two nations were then exempted. The rate then rose to a new 145% tariff on a range of Chinese products. Exceptions for certain high-value products were limited to only 22% of the nation’s exports to the U.S. by value.

Combined with existing restrictions held over from Trump’s first term, the new tariffs challenged the profitability of doing business with China. Volumes of cargo ships calling at U.S. ports are falling. The nation’s busiest port complex in southern California reports that traffic from China is down by 35% from a year ago, and poised to fall further. China dominates the U.S.’ supply of durable goods, and shortages are likely to appear in the months ahead.

The timing and composition of resulting product scarcity are difficult to predict, as inventories of specific items are not publicly disclosed. We know that import activity has been especially elevated in recent months as U.S. businesses rushed to accumulate inventory under the old tariff regime. The magnitude was sufficient to drag the estimate of U.S. economic growth negative in the first quarter.

Expect to see supply gaps in the months ahead.

Our outlook, which finds the U.S. avoiding a recession, is based on gradual reductions in tariffs and the striking of new trade agreements. News from the White House indicates movement toward more deals, which is welcome news. Discussions with China are scheduled to begin soon, but will likely take a long time to complete.

The possibility that tariffs may be reduced, however, will create incentives for import orders to be deferred. Importers will await lower tariff rates before resuming their activity, which will compound any shortages. They would also need better long-term clarity about trade policy before making investments to reorient or reshore their supply chains.

Our jobs would be easier if tariff consequences emerged immediately. But transit across oceans, transportation across the country, the depleting of inventories and renegotiation of trade terms are all processes measured in months, not days.

Supply lines are built around these lengthy timeframes. Orders from overseas must be placed months in advance of when they are needed. For instance, production of holiday gifts commences over the summer, with the final shipments leaving China in October. Delays today will be felt in shortages of Fourth of July fireworks and back-to-school supplies. A prolonged impasse could lead to fewer packages under Christmas trees. Even if all new trade barriers were lifted overnight, it would take time to catch up with the supply gaps that have been introduced.

Today’s bilateral U.S.-China trade conflict will not be a disruption on the scale of the global pandemic, but some of the lessons of 2020 can inform our view of what might be in store. Most pertinently, we learned that gaps in the supply chain can compound. Bloomberg dissected how the semiconductor shortage disrupted the supply of gummy bear candy. When supply chains work well, they are easy to forget; when they halt or break, the repercussions can linger.

Outcomes of tighter trade policy will be variable and unpredictable.

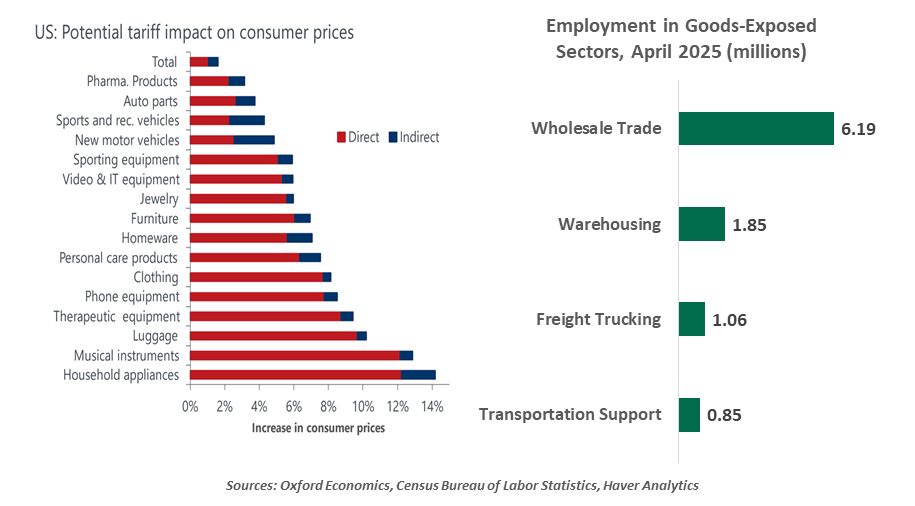

Scarce supplies will lead to higher prices, rekindling inflationary risks. Oxford Economics estimates that tariff effects will add 1% to the inflation rate. We are likely to see much larger cost increases in categories with low margins and a high reliance on China, like appliances, luggage and clothing.

Tariffs also put some jobs at risk. Already, longshoremen are losing shifts and truck drivers are reporting fewer loads to haul. Trade-exposed workers will feel uneasy about their financial security, cooling their spending.

These prospects have complicated the Federal Reserve’s work. This week’s Federal Open Market Committee statement plainly noted “the risks of higher unemployment and higher inflation have risen.” Chair Powell was peppered with questions about trade disruptions, though they are beyond the control of monetary policy. The Fed’s wait-and-see approach illustrates the difficulty of gauging the timing and extent of tariff costs, but their guidance suggests they are braced for bad news.

My bird’s-eye view of shipping infrastructure brought home American reliance on imports from the Far East. Disruptions to this flow of goods will create turbulence that could scuttle the soft landing.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.