Housing Reforms On The Horizon?

Housing markets do not change quickly.

By Ryan Boyle

Some of the most useful financial advice has a homespun tone, like to make hay while the sun is shining or save up for a rainy day. I recently encountered another helpful idea in that vein: Think of your house like a family member who is always sick. The owner will take care of its needs but never really be done worrying and managing its problems.

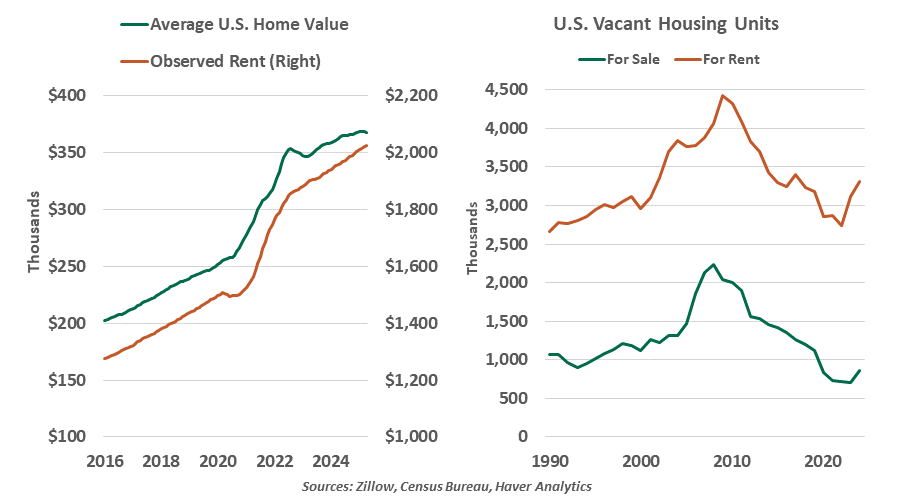

Viewed broadly, the U.S. housing sector can’t seem to find its way back to perfect health. Its maladies have evolved: twenty years ago, house prices swelled, then corrected in a manner so severe that it brought the global economy into recession. It took years to work through bad debt and find a new equilibrium. After a gradual recovery, the pandemic rapidly altered market dynamics, with a surge of buyers snapping up every available property across the country. Now, the market is expensive and under-supplied.

The current paucity of properties was long in the making. Following the 2008 crisis, market appetite to invest in residential real estate development was limited. When demand returned, inventory was not available to react. And then the pandemic hit, and prices nationwide rose 40% from 2020 to 2022.

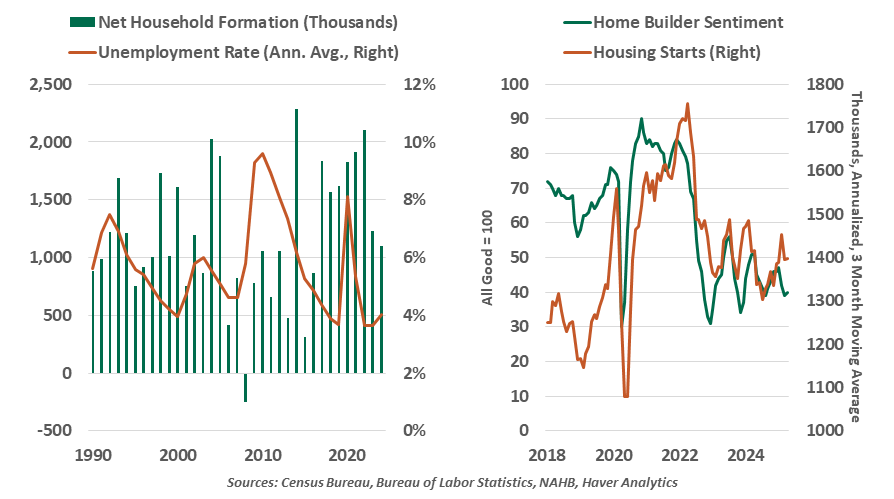

In a free and efficient market, a lack of supply should be met with investment to meet the rising need. Instead, housing starts have held steady. Builders face a series of frictions such as land use regulations, permitting and carrying costs during construction.

Home builders have remained cautious, despite high demand for housing.

As well, homebuilders must have confidence that they can sell completed homes at a profit. The cost basis of a home started today is less predictable: tariffs may raise the cost of materials, while tighter immigration policy could impact the supply of labor. And rising recession odds raise the risk that selling prices could fall. Homebuilder sentiment is hovering near a 10 year low.

Multifamily developments have also been slow to break ground amid tighter credit conditions. These projects take more time to complete. Very few apartments are on track to be delivered in the next two years, which will keep rents firm in many markets.

Demand for housing has retreated, but not stalled. Household formation has continued apace, and immigration flows have added to the population seeking housing. Resilient employment markets have equipped more workers to step into home ownership. Shoppers are no longer shocked by prices or interest rates. A smaller number of buyers are making purchases from a more limited inventory.

Homeownership is not within everyone’s reach. Those who cannot yet afford a home are keeping demand for rental housing strong.

The U.S. system of home financing may also not be in its best state of health. Homeowners are able to take mortgages with rates fixed for 30 years, made possible by insurance provided by the government-sponsored entities (GSEs) Fannie Mae and Freddie Mac. The GSEs facilitate a secondary market for mortgage debt, adding to liquidity. Their government backing removes much credit risk for investors, keeping mortgage rates low.

Could Fannie and Freddie finally come out of conservatorship?

The GSEs were not designed to be wholly-owned governmental bodies; they operated independently when they were chartered. However, an emergency federal intervention during the financial crisis put the GSEs into federal receivership, a condition that persists to this day. In exchange for getting recapitalized in a crisis, the GSEs pay their income to the Treasury.

In the weeks before President Trump’s inauguration, a path toward returning the GSEs to private hands was proposed. Similar work had started in the first Trump term, and continued through the waning days of the Biden administration. Analysts began to anticipate that the deal would get done.

But spinning off the GSEs would be expensive. The Congressional Budget Office estimates the GSEs would need to raise $370 billion to build adequate capital. That value is attainable if they are allowed to retain earnings rather than forfeit their income, but it would take three years.

And the timing of this plan is not optimal. The next federal budget is shaping up to widen the deficit, leading to the recent downgrade of U.S. sovereign debt. The Federal government needs all the revenue it can get, and the roughly $30 billion of the GSEs’ annual net income would be missed. However, the U.S. Treasury holds preferred shares and warrants for up to 80% of the GSEs’ value; unwinding this position to private investors could generate a windfall.

Valuing the GSEs, though, would not be straightforward. They function with the backing of the U.S. government. Mortgage-backed securities (MBS) are viewed as close to risk-free. If that assurance is removed, how will the risk within MBS be priced? Absent clear government support for the GSEs, mortgage rates will rise, and MBS demand will change.

We are also cautious about our hopes for other deregulation in the housing sector. Easier permitting for new construction is not a federal matter, as most land use regulations are local. The 2024 Republican platform included plans to make more federal land available for development, though most of these protected lands are in remote areas, far from commercial centers. And preparing newly-released land for construction is not a fast or simple process.

Well-being comes from a series of healthy choices, which aren’t always easy. The maladies of the housing market have been difficult, and the treatment will require creativity and adaptation. But ignoring the symptoms will not make the problems go away.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.